A lot has been written about the so called ‘sun tax’ with the finalisation of two way tariffs that start on 1 July 2024 in NSW. Much of the reporting is primarily concerned with the fairness of charging a distribution fee on exports during the middle of the day.

However, the mainstream media misses what I believe is the bigger issue – the size and degree of symmetry of the distribution reward being paid for exports during peak periods of demand.

Accelerated deployment of solar PV and home batteries can help address the challenges and delays being experienced with large scale renewable and transmission build out.

Homes and small businesses that electrify in this manner radically reduce their demands on bulk generation, distribution and network services. And in this context the initial trials of two way tariffs were an encouraging development.

Take the Ausgrid two-way tariff trial which ends on 30 June 2024. It includes a modest export charge of 2 c/kWh for exports above 6kWh between 10am and 2pm, but also includes a reward of 26.6 c/kWh for exports between 2pm and 8pm.

Significantly, this reward is very close to symmetrical with respect to the charge for importing electricity during this peak period (27.3 c/kWh) and in fact when the trial was originally introduced in 2022 the reward and charge were exactly equal.

This trial created a sizeable incentive to install and operate a home battery exposed to this tariff. In Ausgrid’s words the trial pricing structure “made our trial tariff lucrative for customers investing in batteries.”

The symmetric pricing feels fair – if a user is charged $x for taking a unit of energy from the distribution network during a peak demand period surely they should be rewarded by $x for feeding back the same unit of energy into the distribution network in the same window.

Indeed, from a physical system perspective there is no difference between one user reducing their peak demand by 1 unit of energy and another user on the same feeder pushing in a unit of energy over the same time period.

Essential Energy appreciates this logic, in their 2024-2029 revised tariff structure statement they say they have “ … sought to align the LV tariff export rebate with the equivalent peak consumption charge in the same time window to provide a symmetrical reward to customers and encourage reductions in peak demand”

And here is how Endeavour Energy describes the need to encourage exports during peak demand in their tariff structure statement for 2024-2029:

“First, when customer demand peaks in the evening and our network becomes constrained, we are required to make additional investments in network capacity to ensure that we can continue to provide safe and reliable import services to customers.

“However, additional exports by customers during these periods of peak demand can help to avoid those network investments, thereby reducing the costs we need to recover from customers.

“By signalling to customers the future costs that can be avoided by exporting in the evenings – using export rewards – we can signal to customers the network benefit associated with exports in the evening.”

Unfortunately, the transition from trial two way tariffs to production two way tariffs has not maintained this desirable symmetry in any of the NSW DNSP plans.

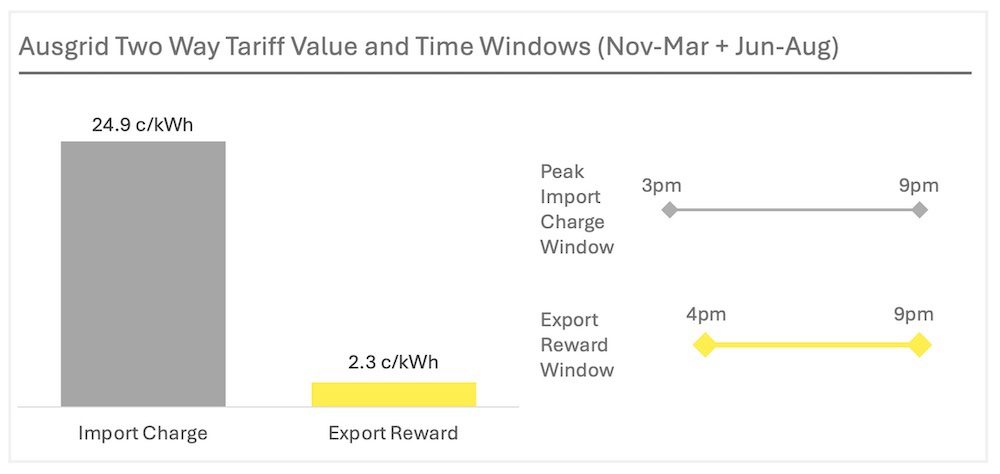

The production Ausgrid two way tariff for 2024-2025 has an export reward of only 2.3 c/kWh (now for exports between 4pm and 9pm). This is in comparison to their peak import charge (3pm – 9pm) of 24.9 c/kWh for 8 months of the year*.

So the symmetry and simplicity of matching timeframes and charge / reward for peak usage and export are both gone.

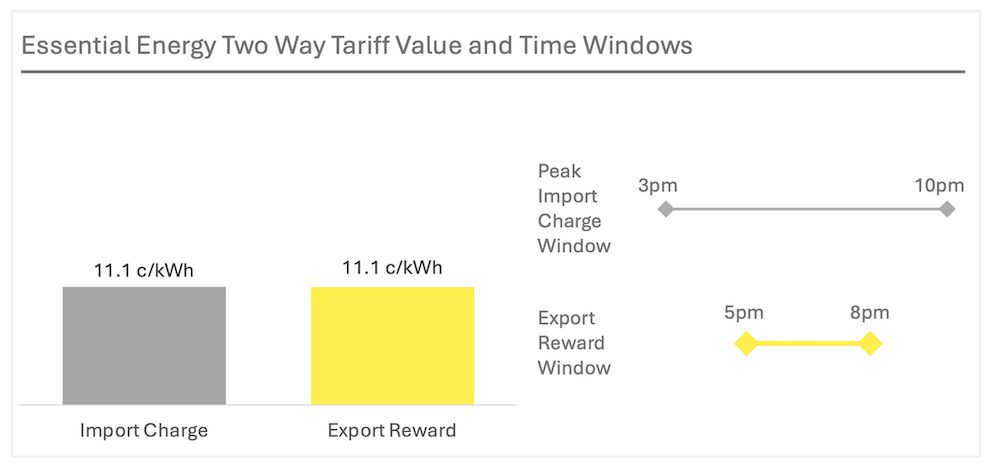

Essential Energy still seems committed to a component of symmetry for its two way tariff, which only comes into effect in 2025, with the export reward and charge being set at 11.1 c/kWh (but the reward only kicks in from 5pm to 8pm, while the peak charge is applicable from 3pm to 10pm).

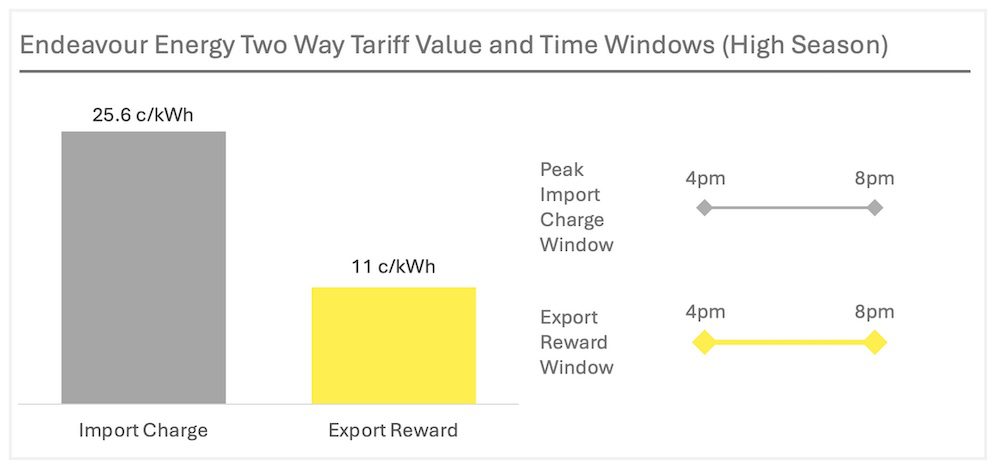

And conversely Endeavour is keeping symmetry on the timeframe (4pm – 8pm for export reward and peak charges) but giving an 11 c/kWh reward against a 25.6 c/kWh high season peak energy charge.

Each DNSP has a rationale for the AER to justify their two-way tariffs in terms of their long run marginal cost (LRMC) and ‘residual costs’. The long run marginal costs are the forward looking costs to scale the network for increased imports and exports.

In Essential Energy’s words, the residual costs are “the difference between LRMC-driven costs and our AER- allowed revenues”. For example, Ausgrid say they made a mistake by including the residual costs in the trail tariff export reward, here is how they describe it in their revised TSS explanatory statement for 2024-2029:

“Residual costs in export tariffs distort customer decisions – the trial tariff artificially increased the peak usage charge and the export reward, by recovering additional residual costs from consumption and refunding those residual costs in the export reward.

“This approach has made our trial tariff lucrative for customers investing in batteries and driven additional cycling of batteries in response to our tariff. This has informed our decision to base export charges and rewards on the LRMC of exports on our network.”

So, what do you think? Should the DNSPs be pressured to offer symmetric (both value & timeframe) two way tariffs and thereby accelerate deployment of behind the meter batteries and west facing solar panels?

Or would the unavoidable increase in other elements of the distribution network charges (to ensure the DNSP recovers all its residual costs and makes the full AER allowed revenue) outweigh the symmetric benefits?

* For apples to apples comparison the numbers quoted are from Ausgrid’s energy based time of use plan(EA025), rather the default demand plan (EA116) which has a lower peak energy usage rate (2.1 c/kWh) but a hefty peak demand fee of 30 c/kW/day with no symmetric export benefit.