Source: Free Pik

Australia’s near-term climate ambition has been redefined as a range between two hard numbers: a 62 to 70% emissions cut by 2035.

What we don’t have is a range, or any number, for valuing the cost of carbon in our largest domestic pool of available capital to help achieve that ambition. This is a glaring anomaly that must be fixed.

That pool of available capital is called superannuation, or compulsory ‘super’ to most of us. The fact that it’s compulsory is not irrelevant to this discussion, but more of that later.

Australia now has a $4.3 trillion pool of super, a bit over $3 trillion of which sits in large APRA-regulated funds.

Together, these big super funds are the nation’s most potentially powerful investors, holding assets worth more than our annual GDP. Those funds have an astounding degree of latitude to move assets around as they see fit.

During the global financial crisis in late 2008, for example, Australia raised more equity capital than any other country in the OECD.

Super came to the party and recapitalised our banks and then major corporates in a time of need. Yet, in 2025 in a different time of need, less than 1% of big super’s capital is currently invested in targeted, climate-related investments.

What can be done to get super funds to allocate more capital to decarbonisation, while protecting the long-term financial interests of their millions of members?

A new proposal from The Conexus Institute suggests one simple, system-wide intervention: a mandatory Value of Emissions Reduction (VER) framework for all those big super funds. The idea is elegant in its simplicity — to make the cost of carbon visible in every investment decision (ie hold, buy or sell).

Although a small number of leading super funds use their own internal carbon prices, most investment analysis in super currently treats emissions as externalities — important but not priced. A VER framework would change that by assigning a notional value to avoided or reduced carbon to all big super funds.

In simple terms, a VER applies a notional cost per tonne of CO₂e to investment opportunities and existing holdings. It’s not a tax, fee, or transfer of money, but a shadow price — a disciplined, system-wide tool for pricing in the financial impact of emissions.

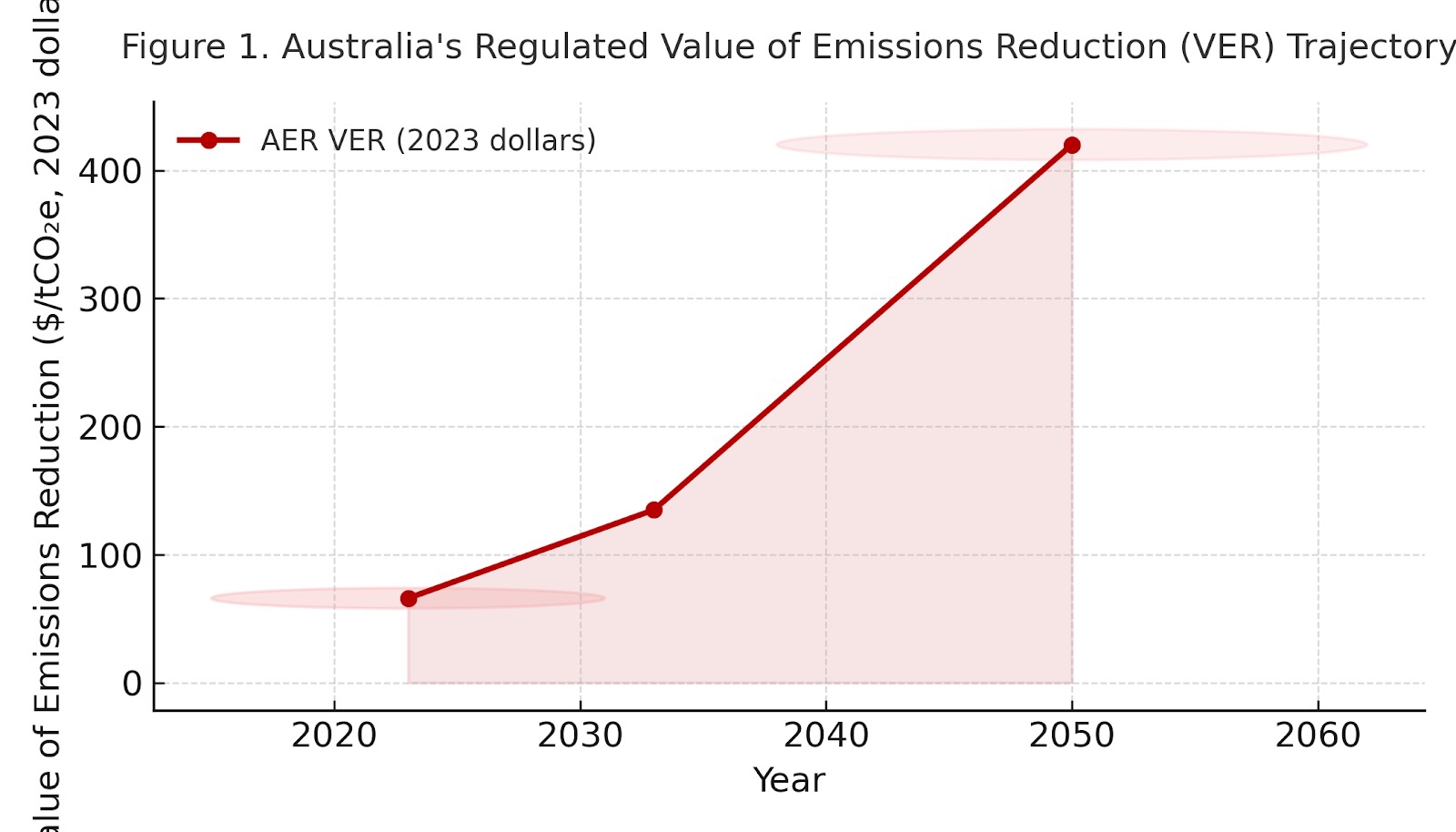

The Australian Energy Regulator (AER) already publishes an official VER for use across the energy sector: $66 per tonne of CO₂e in 2023, rising to $135 by 2033 and $420 by 2050.

These figures are based on carbon credit and abatement cost projections and are now embedded in the National Electricity Objective. Extending this methodology to super would bring coherence between the financial and energy systems.

Critics might quibble about whether using the AER price is exactly right for super, but expert policymakers can have a look at that issue.

The advantages behind using the AER price are that it already exists and was created independently of the super system. A good start, but if it can be improved it should be. The point is that it needs to be done quickly.

By embedding a VER, every investment decision would carry an implicit climate score. The mechanism translates emissions into currency — the one language all investors speak.

A uniform VER, anchored to the AER methodology, could offer the predictability markets crave. It would link energy regulation, financial (including sustainability) reporting, and climate policy into one coherent signal. Over time, it would become as routine as interest-rate assumptions in discounted cash flow models.

Set out below is the ‘cost curve’ of the AER’s VER.

Consider a renewable energy project versus a gas-fired power plant. Under conventional analysis, the two might appear similar in risk-adjusted return.

Add a VER, and the gas project carries a multi-million-dollar notional emissions cost over its lifetime. The renewable project, by contrast, carries little or none. Suddenly, the return gap widens — not because of ideology, but because of risk-adjusted economics.

A mandatory VER would also dovetail with the new Australian Sustainability Reporting Standard (AASB S2), which requires entities using an internal carbon price to disclose how they apply that price.

Making carbon more visible in super helps all the system’s 17 million or so members in ways that extend beyond merely meeting Australia’s climate targets. Younger Australians will now typically contribute to super over 40-year horizons (a typical work career) and then might expect spending money from their super for another 25 or more years (during retirement).

This means that members in their 20s today might still be reliant on their super in the 2080s and 2090s. Seen this way, decarbonisation is also a ‘retirement income’ problem.

A dignified retirement is now inextricably linked with decarbonisation. What’s the point of having a pile of super savings in retirement if the climate has effectively already spent them for you?

Climate risk is equally important to older members. A person retiring today will still typically spend 25+ years on the planet and be at least partly dependent on their super for their financial wellbeing during that period.

We also need to remember that super is heavily subsidised by tax concessions. This gives the government a bit more ‘social licence’ to ask the system to do more on decarbonisation. At the same time, members will be protected by the existing obligations on funds to act in members’ best financial interests.

Pricing carbon within the super system is not a moral or ethical gesture; it’s financial risk management. Markets will eventually reprice emissions — the only question is whether it is done proactively or reactively.

A mandatory VER would ensure that the world’s fourth-largest retirement savings system reflects the economic truth of the transition: carbon has a cost, and the sooner it’s accounted for, the smoother the path to net zero will be.

For decades, super has managed the nation’s savings. With a VER, it could also help manage the nation’s climate risk — by making the invisible cost of carbon visible where it matters most: the capital markets.

Jeremy Cooper is a strategic adviser on ESG and financial services issues in a range of capacities. He is a former Deputy Chair of ASIC; and chaired the Cooper Review into Australia’s super system.

Claims and promises of carbon offset schemes are falling deep into the category of being…

Australia has just experienced its worst heatwave in six years but it's set to become…

There will be daily cap on the federal government's Shared Solar free power offer, to…

Developer of what was once hailed as the biggest solar hybrid project cuts PV component…

Fortescue wind technology company says its turbines will be the "tallest, mightiest and the widest,"…

Rooftop solar reaches remarkable 117 pct of state demand in Australia's most advanced renewable state,…

{kind=link}