Satellite image of damage after a drone attack to an oil refinery in Saudi Arabia. (Satellite image ©2026 Vantor via AP)

My conclusion is that a rise in gas prices domestically – as international prices feed through – will lead to an increase in NSW spot electricity prices compared to pre-war expectations. But the extent will likely be minor if NSW coal continues to perform. Last year, Mt Piper had a poor autumn.

There is a bit more wind and solar around, but then demand is also up. Gas prices have so far been quiet even though gas demand is up.

There is already a meaningful amount of new batteries, both utility-scale and behind-the-meter, and there are 2 gigawatts (GW) of utility batteries commissioning, of which 1 GW is in NSW. Batteries usually commission quite quickly.

In the end, big rises in fossil fuel prices signal their own doom. The impact is to accelerate the move to lower-risk, fixed-cost renewables. That applies to transport, to electricity and to process heat. The high prices probably won’t last that long, but the induced substitution will be permanent.

Based on some comments on WattClarity, LinkedIn and an article by Angela Macdonald Smith over at the AFR, it seemed like a good time to put on the price forecaster hat, invoke the dashboard tools and develop a feel for the variables.

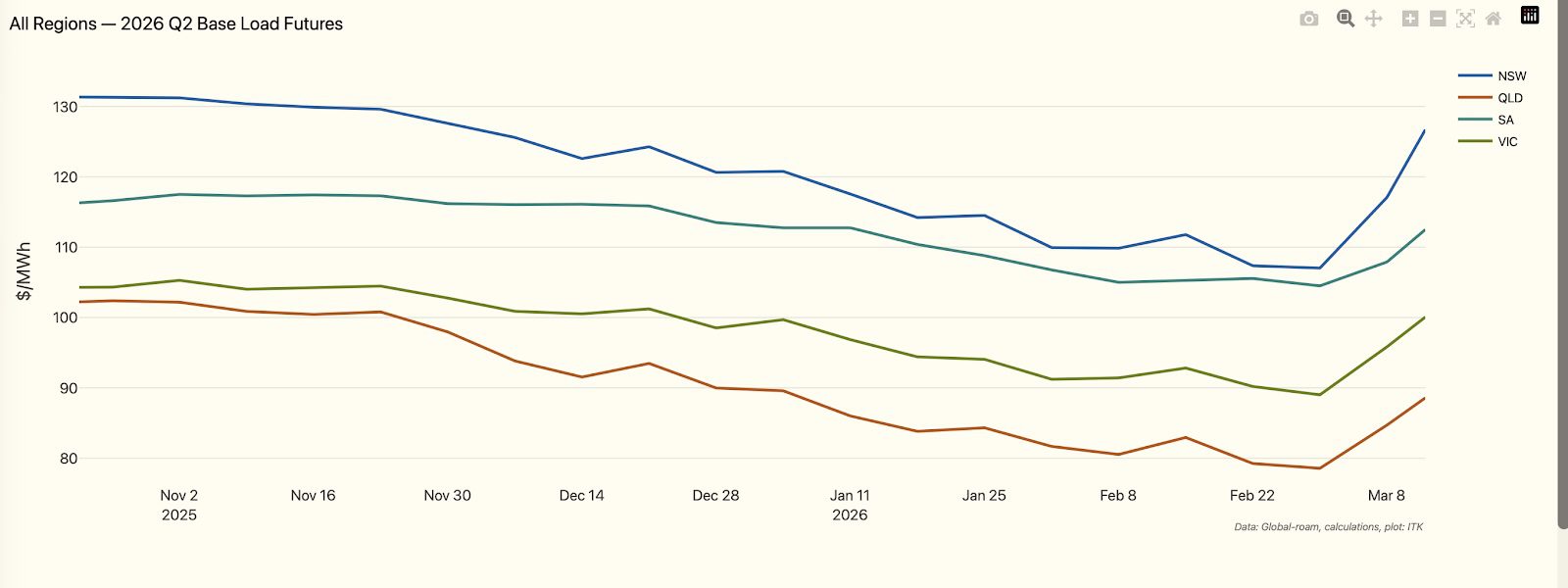

Figure 1: Futures jump

The jump since Trump declared war on Iran is most noticeable in NSW and comes against a trend of softening prices.

Longer term it’s nothing unusual, but it’s the sudden change in direction that catches the eye.

The following plot shows that price expectations have softened compared to a year ago, despite the June spike. The plot also shows that June is generally the quarter where NSW electricity prices are expected to peak.

Gas demand is generally much higher in winter than in summer, which is why the June quarter matters.

Despite marginally higher demand and the wild take-off of LNG (20% of global supply, from Qatar, goes through Hormuz), spot gas prices have so far really only risen a bit more than you would seasonally expect.

Spot prices were soft through spring and into the start of autumn. Notice also that the NSW price is more volatile despite having more demand.

NSW is at more risk of a price spike because it is structurally undersupplied, partly by design of the NEM back in earlier times and partly because NSW transmission South of Sydney is ridiculously constrained and should have been increased a decade ago, as should the NSW-QLD interconnector.

NSW’s issues today will be Queensland’s in another decade, but that’s another story. You can see how prices are higher in virtually every half hour but particularly at the peak.

Here at ITK we have long, long expected that batteries would reduce the influence of gas on peak prices. It’s not just the batteries themselves, although they certainly matter; it’s the willingness to compete that comes when there are more suppliers.

It’s no secret that thermal energy is a very oligopolistic business in Australia. As hard as it may be to build a utility battery, it’s infinitely easier than building a gas plant and getting the gas supply.

When Russia invaded Ukraine not only did global gas prices spike but so did coal prices. The coal price spike was partly a result of wet weather, at least in Australia.

However, I would contend that things might indeed be a bit different this time. China has increased domestic coal consumption, even if the grade has fallen. It’s built amazing quantities of wind and solar which do make a difference to its demand for coal-fuelled electricity.

Here in Australia there are still floods but they are not as widespread as during the Ukraine crisis. There is no real sense, yet, of coal prices going through the roof.

However NSW remains vulnerable because we haven’t built the replacement capacity for Eraring or Vales Point. It’s frustrating to keep talking about the big new wind farms that could do the job.

Not one of them has yet got to FID let alone be available to help right now. I am as big a fan of Penny Sharpe as I am of Matt Kean and Chris Bowen but, by gosh, the team needs to show some visible progress before the lights do go out.

In any case, if we look at the last 30 days in NSW we can see that, for whatever reason, prices in NSW in the evening peak are massively below last year, despite some marginal increase in total supply.

I think you have to give some credit to batteries as making a difference to peak prices across the NEM but everyone will have their own view.

Equally though, in that evening peak it’s coal providing the bulk of energy – even though gas and hydro (Snowy) have traditionally set the marginal price.

In the plot below I compare the June quarter peak price supply in NSW with what’s happened in the last 30 days. This is a bit of an apples and oranges comparison.

The most interesting point is that, on average, coal generation in NSW has been higher in the last 30 days than it was in the previous June quarter. Imports also become more important and there is naturally less solar.

This once again emphasises that the spot price outcome will very likely depend on how well coal performs. And the truth is:

– The coal generation is old, not being maintained, and there is less incentive to invest in long-term maintenance.

– There are only four coal generators and, generally speaking, if either Bayswater or Eraring lose a unit then the resulting price increase probably outweighs the volume loss. That wouldn’t be true for the 2-unit Mt Piper and Vales Point stations.

If I look back to the last year’s June quarter, Mt Piper, particularly unit 1, and arguably even Bayswater, underdelivered. In my view underperformance by Mt Piper is somewhat structural as it just doesn’t have enough access to coal.

Home batteries can be expected to help. There is no data for measuring the impact other than seeing what happens to spot prices. Neither charging nor discharging of home batteries is measured unless I am missing something, and I often do.

There is some increase in utility solar and a bit of new wind as projects in Victoria and Queensland continue to ramp up.

In regards to utility batteries as measured by Renewmap there are 3 GW in commissioning including the Waratah Super BESS of 850 MW. The replacement transformer at Waratah won’t be available until towards the end of the year so won’t help in the June quarter.

There are currently around 1 GW of batteries commissioning in NSW, and I expect them to have some impact in the June quarter.

The bottom line: NSW futures have jumped but the fundamentals – steady coal performance, growing battery capacity, and so far modest gas price rises – suggest that price rises will be less than when Russia invaded Ukraine.

David Hochschild, the head of the California Energy Commission, on how the world's fourth biggest…

Fifty years of cheap gas and electricity and intensive marketing have distorted perceptions. Every element…

Australian Energy Market Operator says its system and market operation functions should not be separated…

The Clean Energy Council has approved a new PV module with around 25 per cent…

An in-depth webinar exploring the next phase of residential battery storage in Australia, brought to…

Huge wind project that survived LNP's perilous project call-in process kicks off full federal environmental…

{kind=link}