Macarthur wind farm. Credit: Vestas

Wind manufacturer Vestas, with a market capitalisation of about $41 billion, and a global market share of about 35%, held its investor day overnight.

And, as we interviewed the CEO of Vestas Australasia, Peter Cowling, on the latest episode of the Energy Insiders podcast published today, I thought a few extracts of slides from the investor day presentations might be interesting.

Vestas has about 3.5GW of turbines installed in Australia and is installing about another 600MW and, interestingly, the PowAR Rye Park wind farm will be one of the first in the world to use the new 6.2MW turbines, although they will be down-rated to just 6MW.

As briefly alluded to in the podcast, and more fully developed in the presentation, Vestas is indicating that we are moving away from the ever larger onshore turbine model towards a more modular approach.

There is far more to be said and, in looking at the presentation, it’s a reminder of how much work it is for a research analyst to project a P&L, balance sheet, cash flow statement, free cash flow valuation model and then write it up into an industry analysis to be marketed against the efforts of 10 others mostly smarter than yours truly. Rinse and repeat for another few companies. Instead it’s just a matter of copy and pasting a few charts and letting readers draw their own conclusions.

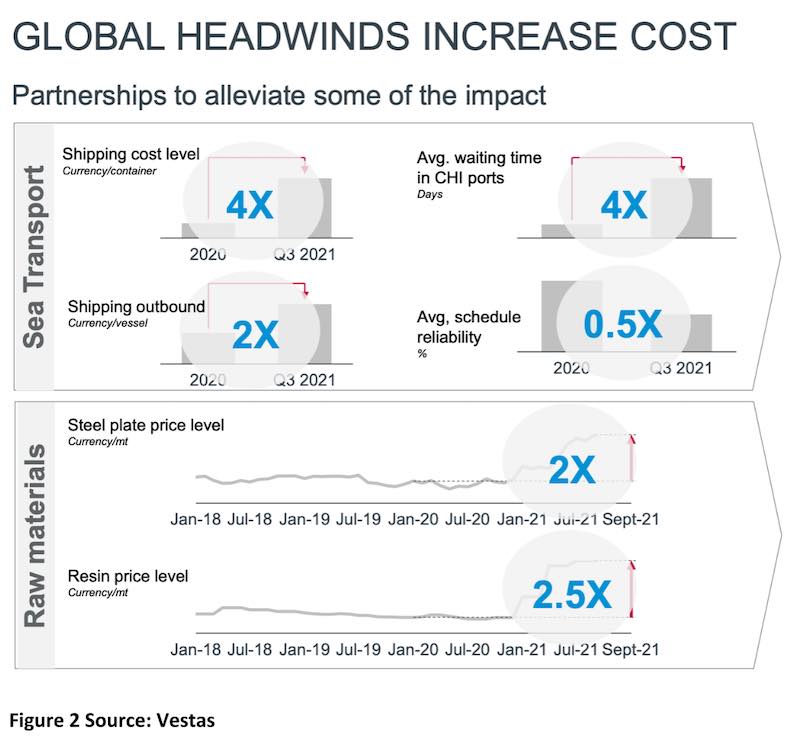

Having said that, if I was an analyst I’d be marking Vestas management down for leaving numbers off the graphs. Here in Australia we demand a pretty high level of disclosure, essentially on the basis of the theory originally articulated by Jensen & Meckling (Agency theory).

I exaggerate the message of Jensen & Meckling to state that the market rewards disclosure. If you take shareholders along with you on the journey they are more likely to appreciate the issues. Anyhow.

I’m not sure if the Danes have a sense of humour, but to me there is plenty of low-level irony in a wind company talking about “cost headwinds”.

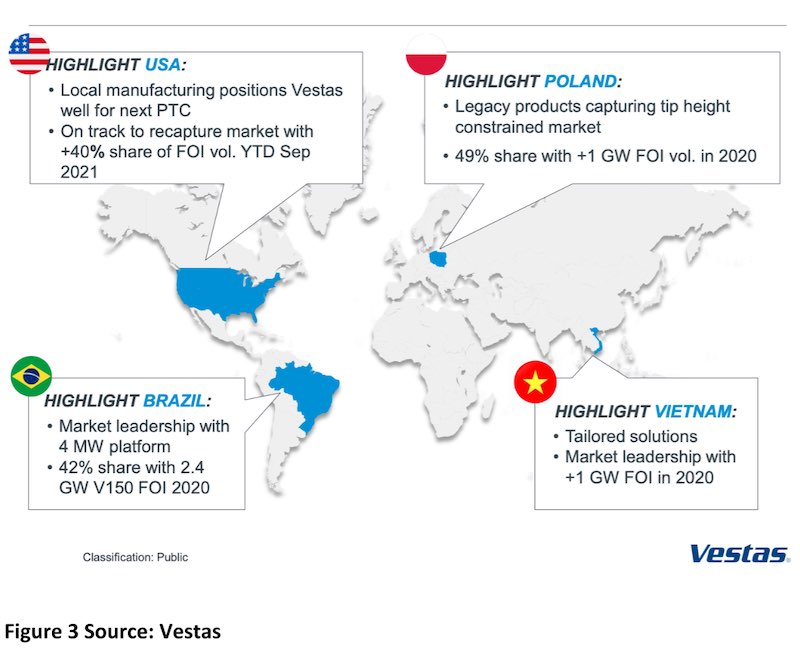

I include this next one because of the Vietnam mention:

To me, 50% growth over the next 10 years is fairly disappointing.

And you can see the Asian offshore wind market potential significance here:

And this shows the relative position of offshore wind to onshore, in terms of cost. However, as Vestas and everyone else is coming to understand, cost is not the same as value.

Wind, in my opinion, has diversity value, capacity factor value (relative to solar it needs less firming, GW for GW) and in some cases is more correlated with demand than solar; and offshore wind may be more correlated with demand than onshore, although to my knowledge there isn’t much public data on that. (Hmm, maybe time to ask the ANU team.)

To listen to our interview Energy Insiders podcast interview with Peter Cowling, please click here: Energy Insiders Podcast: Vestas head winds up on transition.

State government has already ploughed more than $300 million into embattled coal generator, and has…

Less than three years after launching its home battery product, Sigenergy has dominated the Australian…

The next-generation of solar technology could be cheaper, more efficient and a step closer to…

Kaluza CEO Melissa Gander on the change in technologies, and energy thinking, that will deliver…

As Australia's biggest utility stalls on the closure of the biggest coal plant, Andrew Forrest…

Energy retailers should be required to act in their customers’ best interests, rather than forcing…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}