Image: Neoen

Corporate Power Purchase Agreements (PPAs) signed between renewables projects and electricity buyers (directly or indirectly via a retailer) have been an integral part of Australia’s growing renewable energy sector.

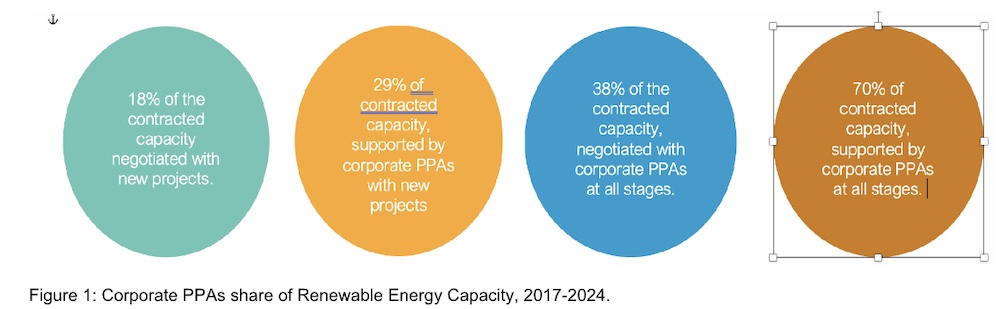

Since 2017, Corporate PPAs have directly contracted for almost one-fifth of the capacity of new renewable energy projects. As many PPAs are contracted for only some project capacity, they have supported new projects accounting for just under one-third of the capacity.

Once you also consider Corporate PPAs that have been signed with projects that are financially committed or operational, their involvement extends to the majority of projects.

Corporate PPAs have directly contracted for almost 40 per cent of capacity and supported projects that account for 70 per cent of capacity installed. In other words, only 30 per cent of the renewable energy capacity installed since 2017 has not been supported at some stage by a Corporate PPA.

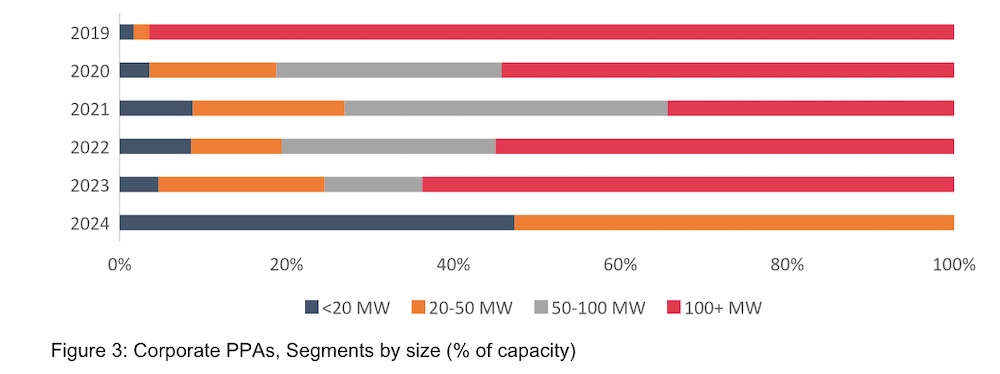

In 2024, the deal volume hit a new record for the third year running – almost 3400 MW.

There were two mega-deals signed by Rio Tinto at the beginning of 2023 (1120MW, Bungaban Wind Farm; 1100MW, Upper Calliope Solar Farm). In what may be a sign of things to come, the resource sector was the biggest player in the Corporate PPA market last year.

Many market participants described the Australian corporate renewables PPA sector in 2023 as a ‘sellers market’ with a slowdown in supply (due to a multitude of factors e.g. transmission constraints) and strong buyer demand ahead of 2025 targets.

Many of the same dynamics were at play in 2024, but there was an element of stasis. On the demand-side, there were less buyers in acute need to contract and some appear to have been waiting for new supply. On the supply-side, the volume of renewable energy projects reaching financial close did not accelerate until the second half of 2024.

The Australian Energy Regulator is forecasting 5GW of renewable energy will be connected to the grid during 2025 and much more capacity is on the way as the Capacity Investment Scheme and Renewable Energy Zones gather pace.

Whilst there is a big increase in supply on the way, the supply-demand balance is hard to predict in coming years as there will also be parties with PPAs expiring in 2030 entering the market as well as parties seeking to negotiate new PPAs ahead of 2030 target commitments.

One of the features of the Australian market has been the diversity in buyer and deal sizes – unlike some overseas markets which are dominated by large buyers. Where small and mid-sized deals represented a significant portion of the market in past years, large deals accounted for over 95 per cent of capacity announced in 2024.

The polarisation of deal size may be a product of the supply slowdown and therefore temporary, or there could be a structural shift towards a larger-buyer market. The cohort of public sector buyers (governments, universities, councils etc) that signed the small-to-medium sized PPAs in earlier years who are yet to sign a PPA is certainly diminishing.

In their first phase (2016-20), Corporate PPAs were primarily developed by large corporates to leverage greater value and impact from their renewable energy procurement through wholesale PPAs negotiated directly with new projects. In the second phase (2020-23), Corporate PPAs (partly) filled the void after the achievement of the RET and the market expanded to a wider diversity of buyers via de-risked PPAs with operational projects brokered by retailers.

Corporate PPAs may be entering a third-phase as the post-RET policy architecture is established through the Capacity Investment Scheme, Renewable Energy Zones and a new green certificate regime (Renewable Energy Guarantee of Origin, or REGOs) from 2030.

Under this scenario, Corporate PPAs are crowded out as retailers and project developers focus on bidding for contracts under the CIS. The scale of the CIS means this will undoubtedly occur with some parties, but it is unlikely that Corporate PPAs will fade out. Demand for Corporate PPAs is underpinned by emissions reduction targets and reputational drivers, so there will continue to buyers seeking PPAs.

The large PPAs signed by buyers such as Rio Tinto and BHP also demonstrates that large buyers are likely to see value in negotiating directly with projects outside the CIS.

There are reasons why both projects and buyers could decide to incorporate Corporate PPAs into bids for contracts under the Capacity Investment Scheme. For project developers, tender criteria encourage and reward bidders with alternative contracts such as Corporate PPAs because the aim is not to displace conventional market contracting. Brad Hopkins (AEMO Services) noted after the announcement of the second round of NSW LTESAs (November 2023) that Corporate PPAs were being incorporated into bids and enabling them to reduce the tenor and price terms being sought.

For buyers that are seeking higher standards of additionality – or seeking recognition under voluntary schemes that require contracting before financial closure – negotiating a PPA with a project before being awarded a contract is desirable or even essential. A senior lawyer from one of the major firms observed they have seen some buyers concluding agreements before CIS tenders for these reasons.

Corporate PPAs may be negotiated with new projects by large users outside the CIS and sometimes as part of bids through the CIS but this may be the minority as in recent years – and increasingly the role centres on revenue certainty through commissioning and operational phases.

In Queensland, state-owned utilities have on-sold retail PPAs with solar and wind farms after signing a PPA to underwrite construction. A similar dynamic could emerge as the CIS scales up.

Some market participants have already observed projects offering shorter tenor PPAs to attract buyers after securing CIS contracts, and this could be the approach of big retailers that will need to contract with renewable energy in coming years.

Most renewable energy projects since 2017 have involved a Corporate PPA at some part of their lifecycle and this will probably continue.

————

Dr Chris Briggs, Business Renewables Centre – Australia

The annual State of the Market report produced by the BRC-A on Corporate PPAs is being launched at a webinar on Wednesday. Register here.

The BRC-A is also conducting ‘buyer bootcamps’ for organisations seeking to learn how to contract renewable energy PPAs in the Hunter Valley (March 2025) and Brisbane (May 2025). For more information on the BRC-A, visit here or businessrenewables.org.au.

Labor's offshore wind plans are under fire from all corners of the conservative political and…

It's common to see a group of blokes working away on a rooftop solar installation,…

The first stage of what will be Australia's biggest battery has entered the grid management…

Australia's main grid boasted a record share of renewables over summer, and experienced record demand…

Draft strategy says batteries of all sizes - and deep storage - are critical to…

NT confirms plans to extend the life of a nearly 40-year old gas plant as…

{kind=link}

{kind=link}

{kind=link}