(An aerial view of our Tennessee data center under construction (photo credit: Aerial Innovations).

Opposition to data centres in the USA has increased, spreading out from specific community-level concerns to a broader argument about the impact on electricity prices. These concerns could harden into a widespread movement opposing AI and data centres, matched by a counter-movement insisting “AI and data centres are wonderful.”

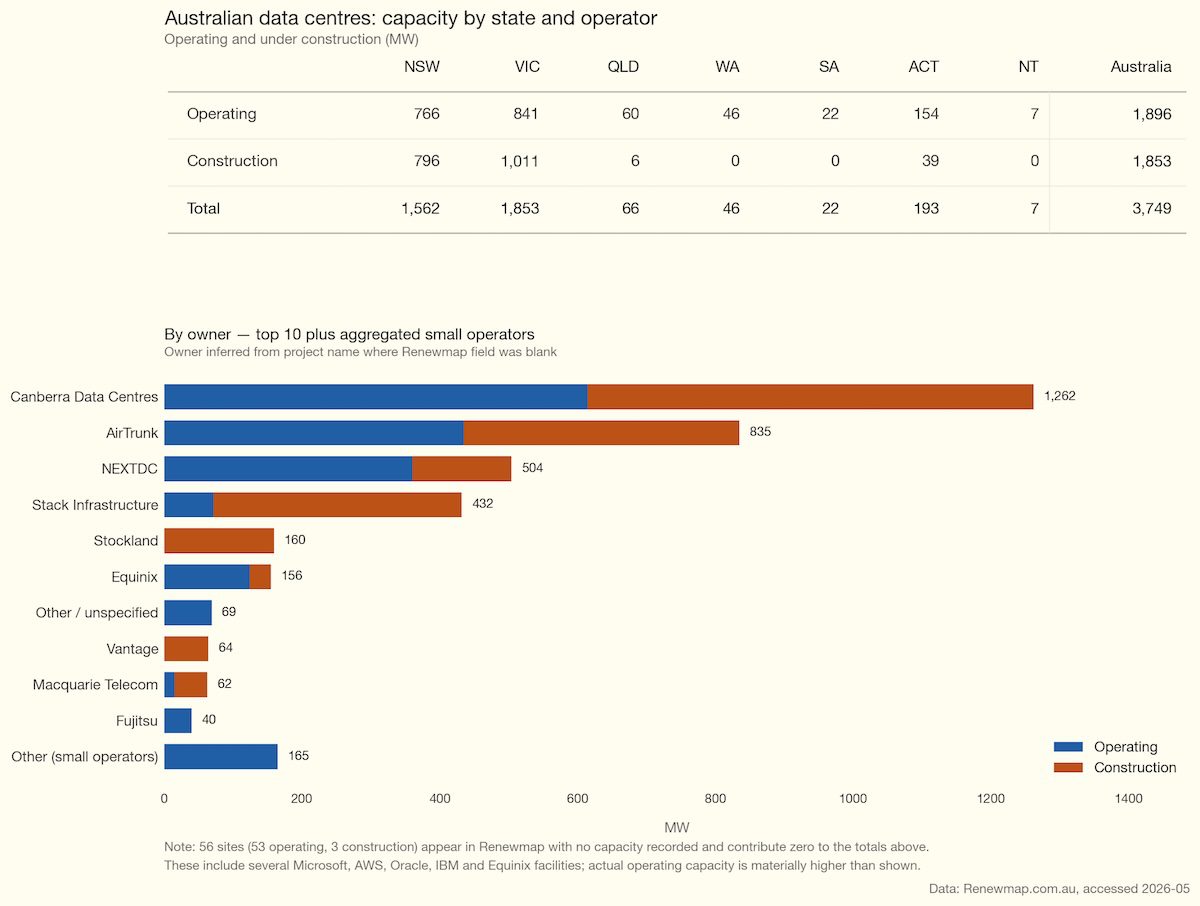

Demand for data centres in Australia is growing strongly. RenewMap identifies close to 1800 MW under construction. Despite limited disclosure, what is being built in Australia is nothing like what Amazon, OpenAI and Meta are building in the USA.

Although data centre size is typically expressed in megawatts (MW), in reality the power cost and power supply is the second most important item. USA AI data centre costs are dominated by depreciation on the graphics processing units (GPUs) and the associated “racks” and clusters.

As far as power goes, in the USA new data centres are dominated by gas; renewables rarely get a mention. Whether in the USA or Australia, backup is done with diesel gensets.

The USA industry argues, to the extent they have any interest, that gas is the only technology available near-term. I’d argue that renewables can be built far more quickly than gas generation – and that using gas actually undermines the industry’s ability to earn society’s trust.

However the more general concern is the idea that data centres have to bring their own generation. Since when? Does every house have to bring its own generation, does every shop, where do we draw the line?

Higher prices provide the signal to build new supply. If data centres increase demand, but also provide firming, then new supply gets built anyway. That’s how the market is supposed to work.

Requiring data centres to bring their own supply also ignores the benefits of a portfolio. Properly designed, the grid provides the lowest-cost supply on average.

Self-supply works when things are going well, but the insurance value of large diversified supply and demand shows up when there is scarcity. We see this insurance value at the regional level, let alone with aluminium smelters or data centres trying to do it all on their own. I return to this point at the end of the note.

Is Australia a good place to build data centres? It doesn’t matter for a few years: chips are so hard to get you couldn’t fit one out with the latest Vera Rubin or Trainium chips for three or four years.

We are a long way from the consumers, but other than that we have the land, we have cheap labour, cheap renewable electricity that will provide sustainable power for decades and lots of software skills. We also have property developers that can compete with the best. So possibly we could be a data centre destination of choice. You can’t rule it out.

For some time now data centres have been the talk of the town, even more so than batteries. Even at the Smart Energy conference, I’m told, solar panels were barely worth a mention and wind energy might as well not exist for all the interest the conference showed in it.

But at Enhar the role of data centres and where batteries fit in was well discussed with two strong presentations from Keith Middleton from Fyfe and Damien Sanford from Celero Infrastructure in a session chaired by Muneeb Anwar from Enhar. The Enhar conference had that nice vibe of the “in crowd” talking to each other.

Why would Amazon, Anthropic or OpenAI choose Australia – 26 million people, thousands of km from the real market?

Surely data centres were just the next hydrogen thought bubble, egged on by policy makers desperate to prove Australia was an attractive investment destination.

If there aren’t going to be any data centres, then the angst about whether they are good or bad is less of an issue.

What I noticed from the presentations is that the presenters focussed – quite correctly, because that was their brief – on the technical side of things, and the contribution that batteries can make.

However this struck a note of discord with me because I’d just been in a prior session where the entire discussion from the battle-hardened renewable energy developers was all about “social licence.” Social licence is a convenient term to reach for, but it is itself value-laden.

As I show in this note, in the USA the data centre industry is already deep into a social licence minefield it hardly knows it’s in. AI labs – this generation’s “masters of the universe” – and the creators of social media don’t seem to understand that they are just as subject to its laws and mores as anyone else.

Even the best of them – Anthropic, in my book – has just done a deal to rent the most polluting data centre recently built in the USA and the one with the least “social licence.”

In this note, therefore, I’ve tried to piece together the state of play in the USA. This may offer some clues – first, on why Australia might be an alternative to Virginia, and second, on how Australia can avoid the same naivety.

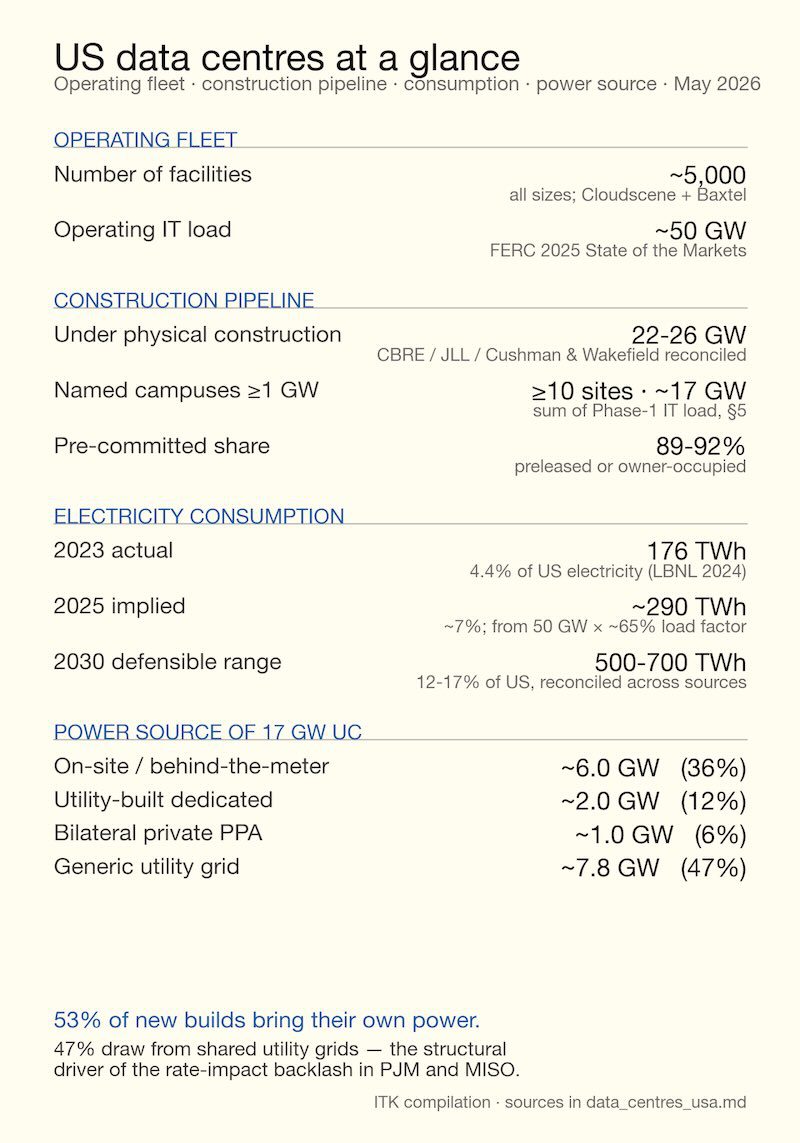

Gonna let these tables speak for themselves.

Figure 1: dc_fleet_at_a_glance

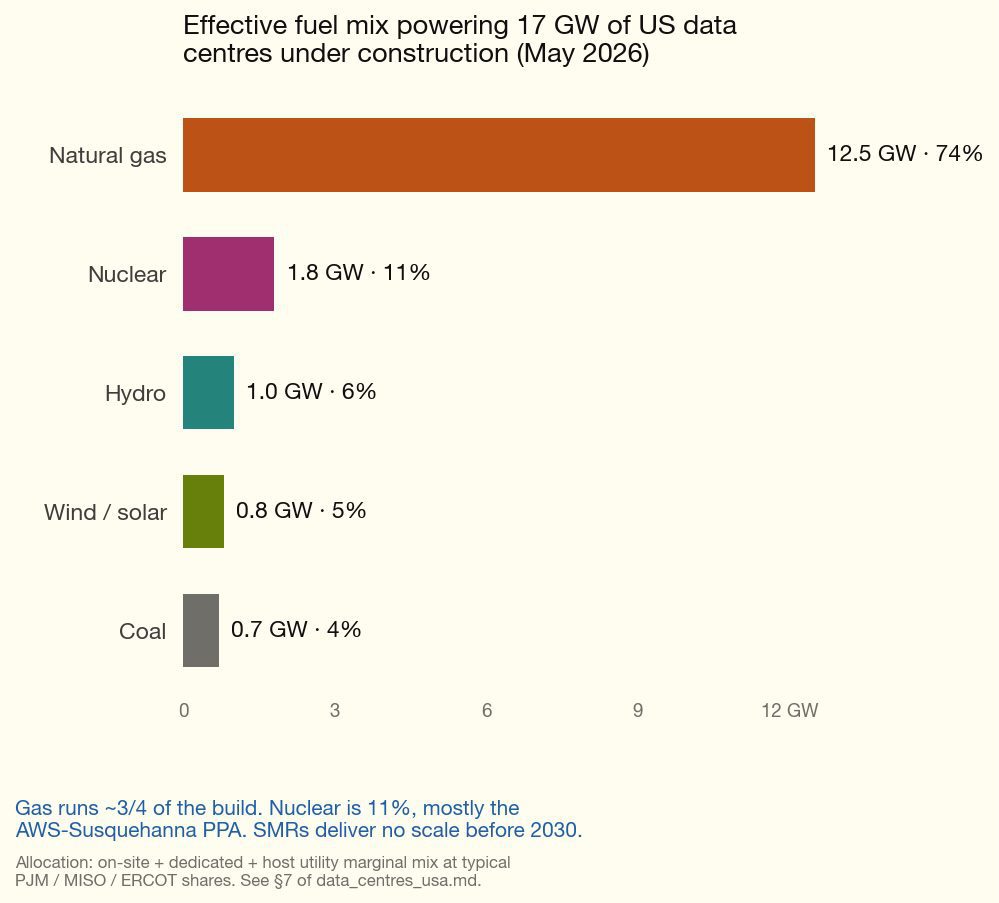

In the USA gas is the primary fuel.

Figure 2: dc_power_fuel

So I think that’s pretty dumb of the USA operators. The 13 gigawatts (GW) of gas means more carbon emissions and more long-term reserve issues. Gas is relatively slow to ramp up and down. It’s short-termism. After all, when your main focus is “where are the chips coming from?” and “who pays for them before my IPO this year?”, long-term power supply issues can look after themselves.

As we will see, community concerns are not really about fuel source – at least not right now. As I say, this is an industry with an ultra-short-term focus.

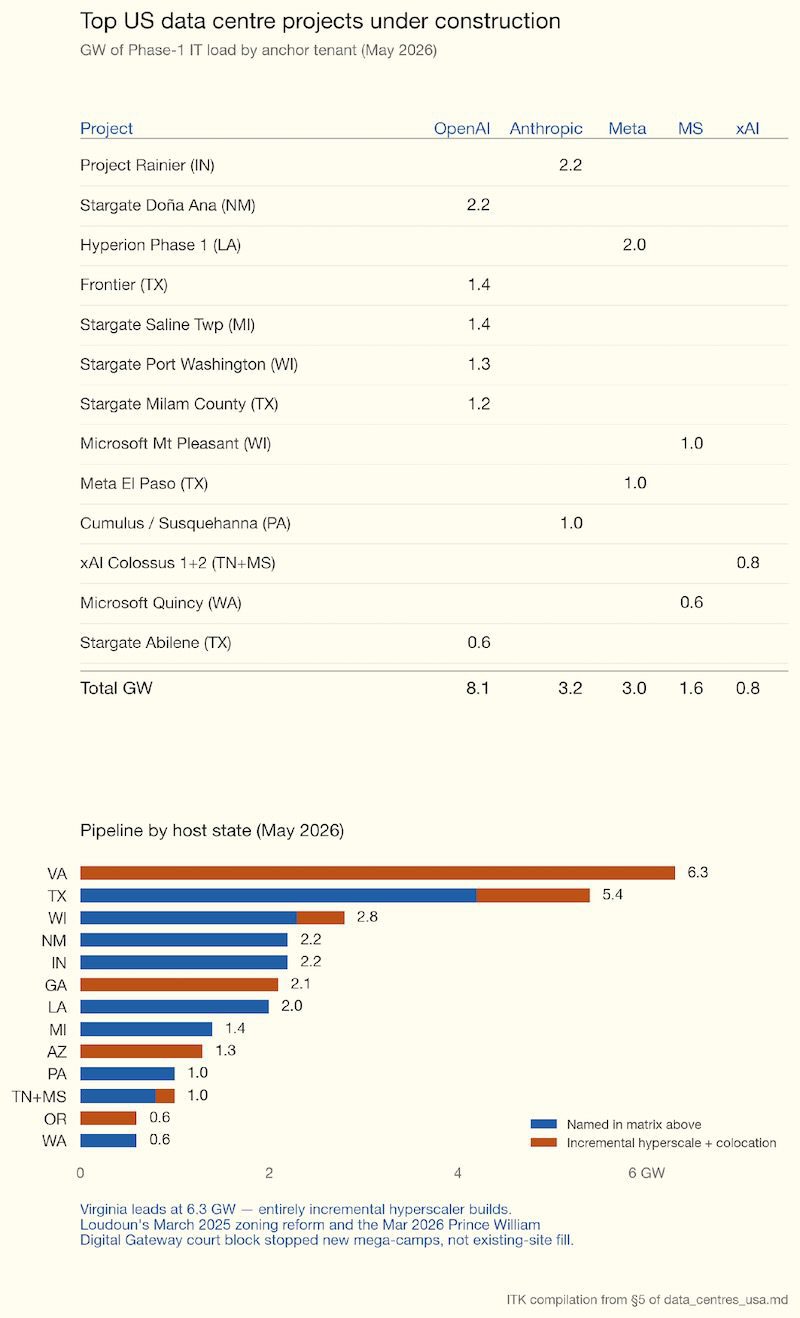

We can also look at the pipeline by tenant and geography.

Figure 3: dc_top_projects

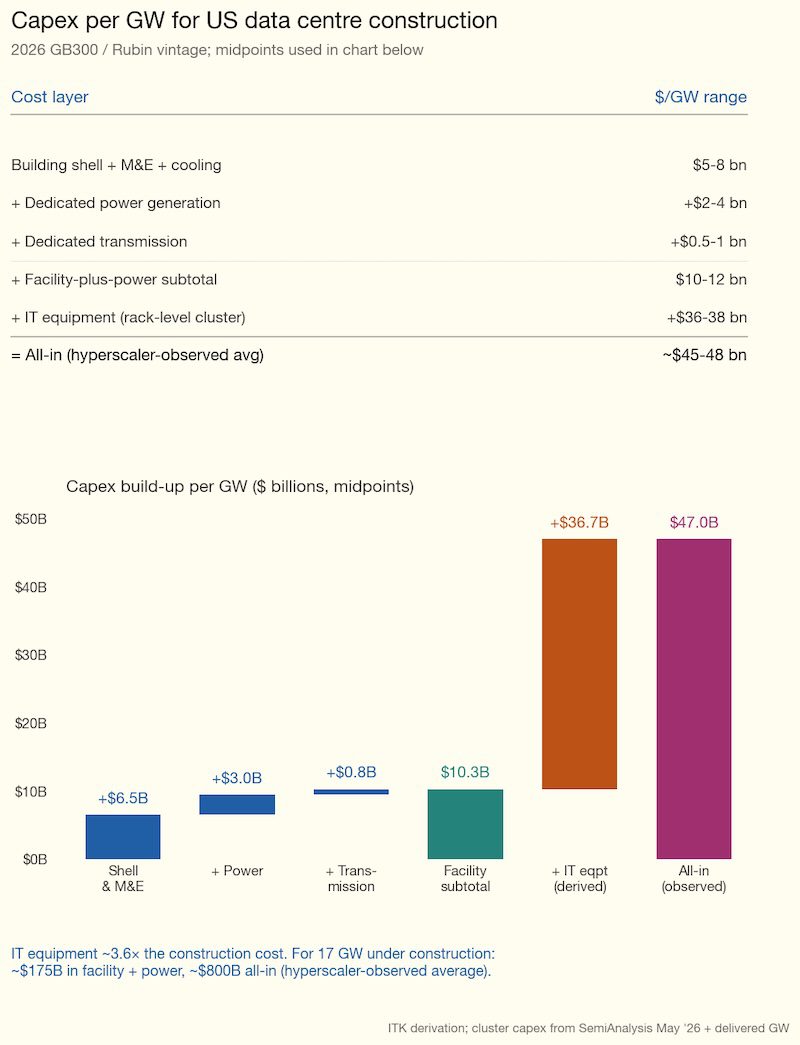

If I work off $US47 billion/GW for the 17 GW actually under construction, that’s about $US0.8 trillion.

Figure 4: dc_capex_per_gw

The global rate at which new AI data centres can actually be energised is not ultimately set by transmission queues or local zoning fights – it is set by TSMC (Taiwan Semiconductor Manufacturing Company).

AI accelerators consumed roughly 9% of TSMC’s leading-edge N3 wafer output in 2025; SemiAnalysis estimates that share reached 60% in 2026 and projects 90% by 2027 (SemiAnalysis, 2026b). Nvidia alone accounts for around 80% of the accelerator-wafer share, with Broadcom – which fabricates Google’s TPUs and Amazon’s Trainium chips – the only meaningful second customer.

The N3 wafer price has lifted from about $US20,000 to $US23,000 over two years, and HBM is in structural deficit through at least 2027. The practical consequence is that headline hyperscaler capex announcements run well ahead of what TSMC and its memory partners can actually deliver, so the binding global constraint on AI data-centre capacity through 2027 is silicon, not megawatts.

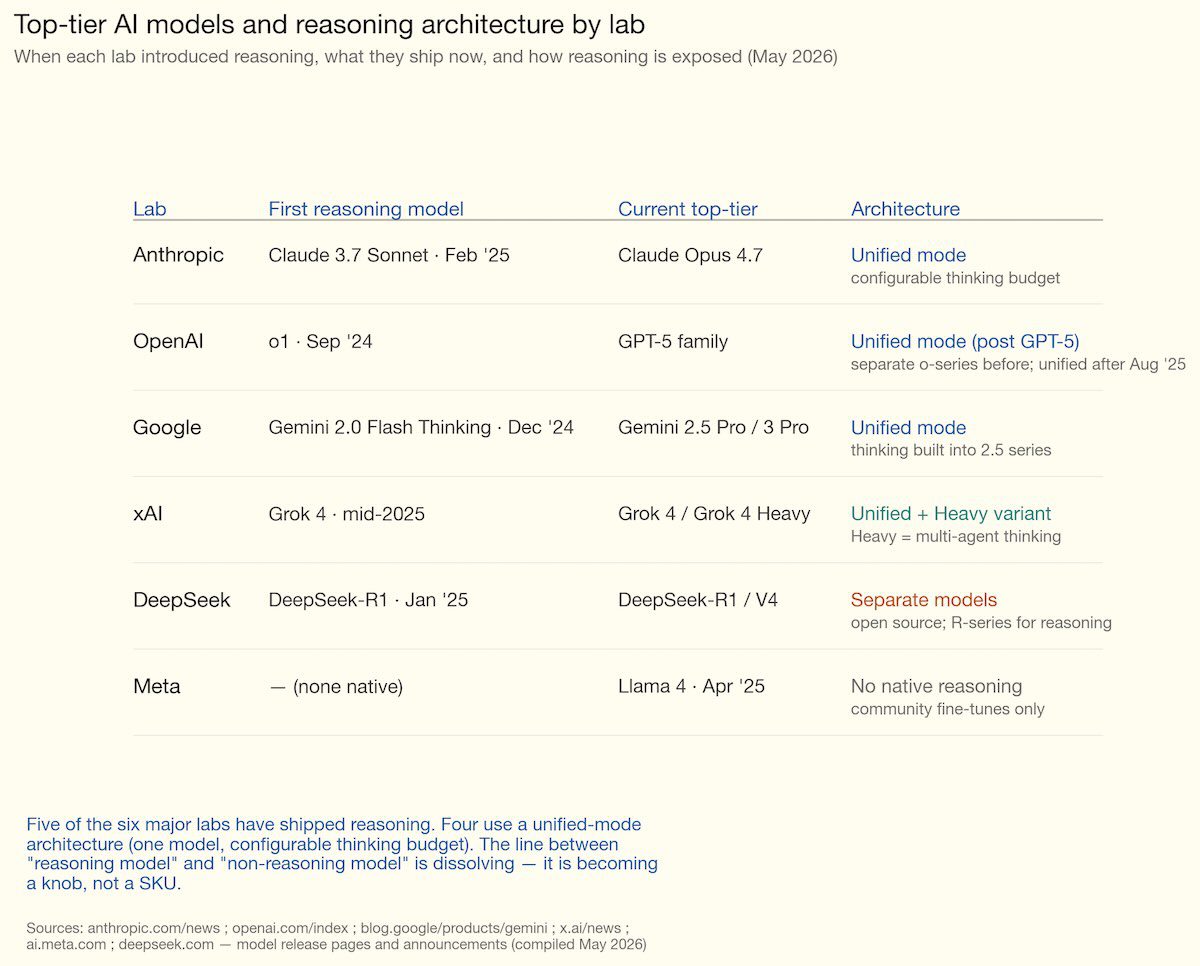

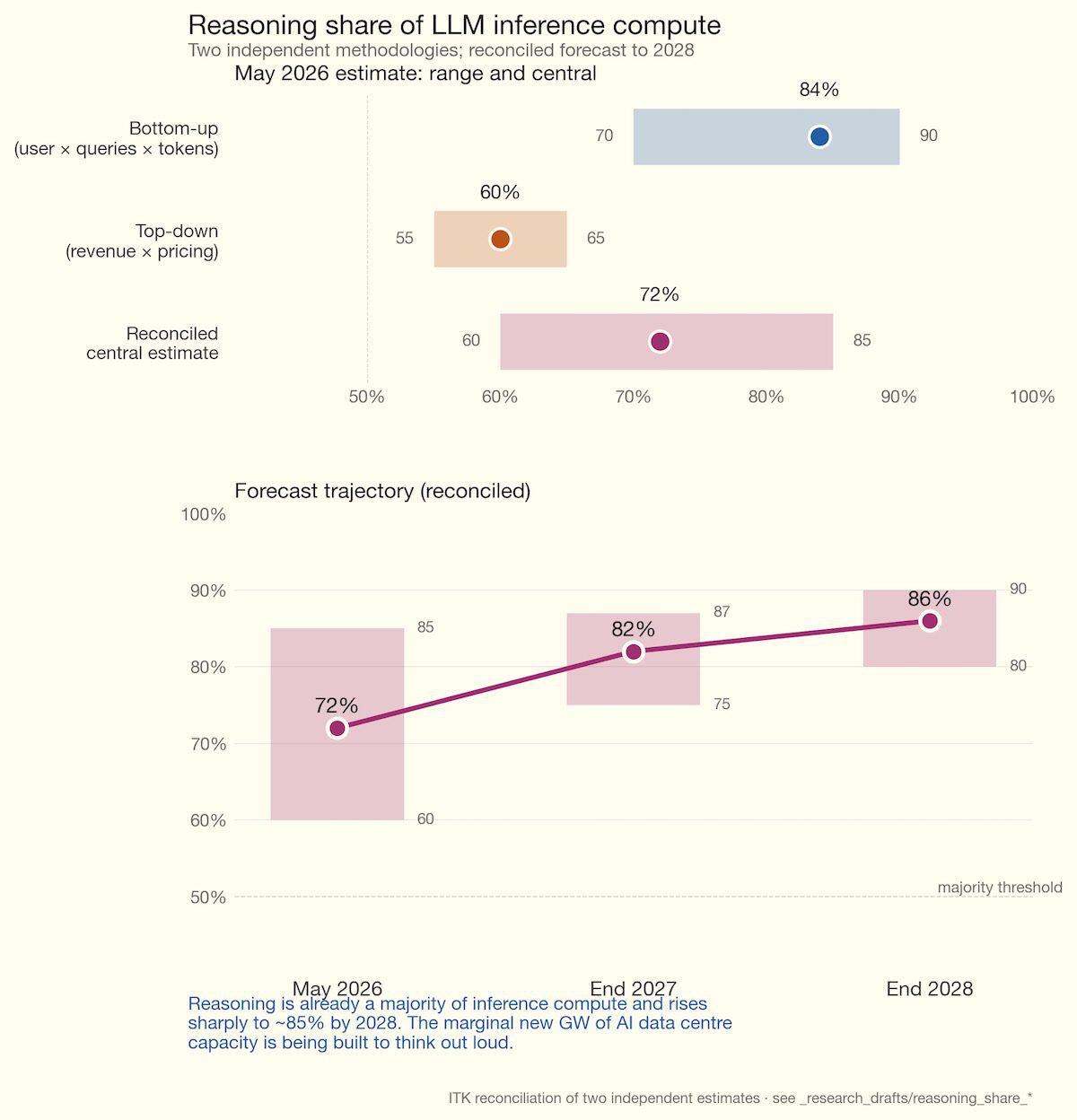

A year ago the view was that inference would have lower capacity utilisation than training. So a 100 MW training load would use more energy than 100 MW devoted to inference (answering user queries). However reasoning models make that assumption questionable.

Figure 5: reasoning_models_lineage

To my way of thinking, as far as model adoption goes, the table shows just how far off the pace Meta is. However Meta’s data centres might still be quite profitable, just not running Meta’s models.

Figure 6: reasoning_compute_share

Reasoning probably already represents the largest share of LLM (large language model) compute, and that share is likely to keep increasing. The implication is that capacity utilisation in a data centre used for AI is likely to be high under any circumstances.

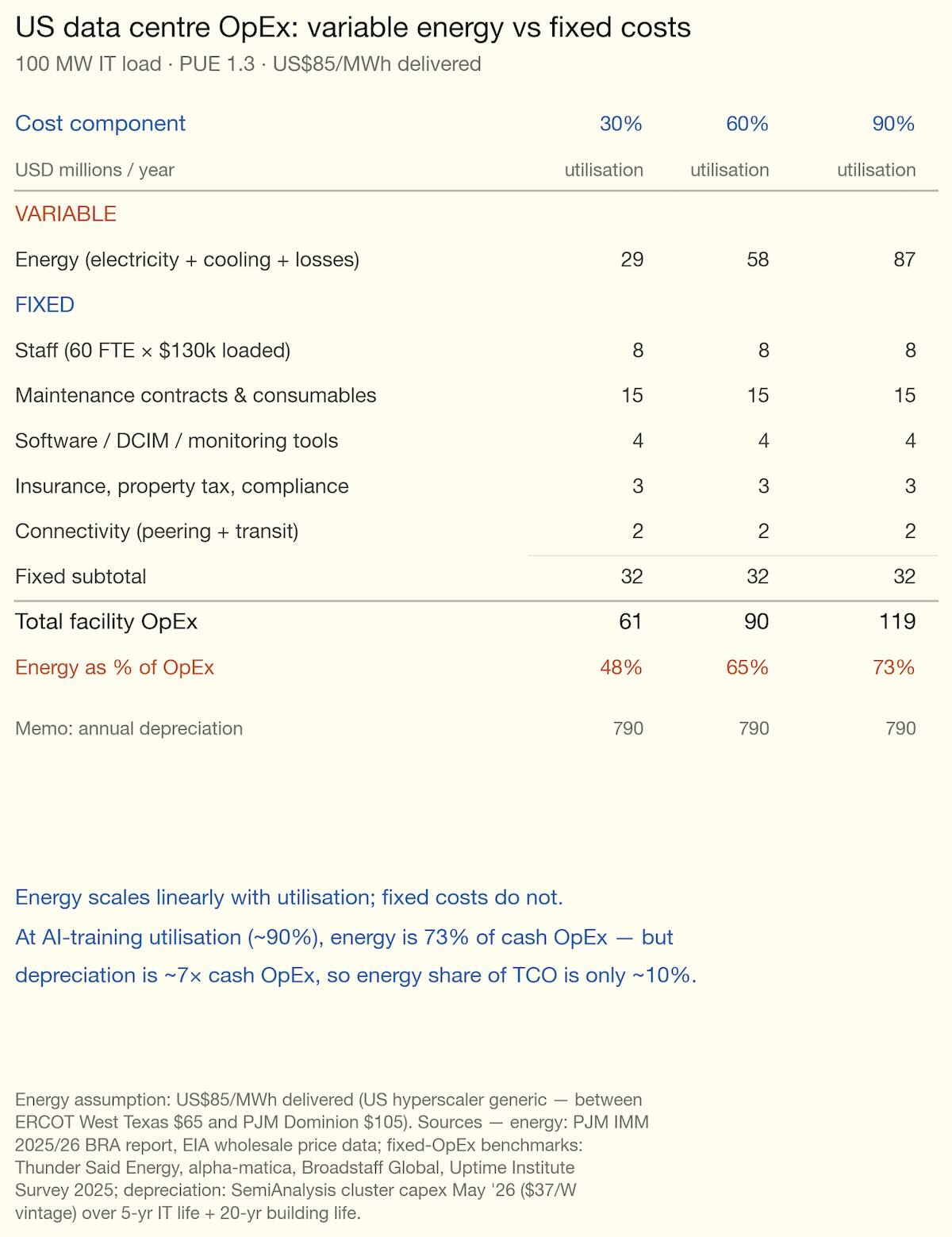

Energy becomes a bigger share of opex the larger the data centre and the higher the capacity utilisation. Fixed annual costs like labour don’t scale with size. Water costs are regarded as minor but you have to have the water.

As the table shows, depreciation is by far the largest cost. I worked off 5 years on the equipment, but currently, due to chip shortages, perhaps 6 years is economic.

On the depreciation point, new chip generations can’t simply be dropped in to replace old ones. Racks and cooling need to be replaced. Building shells may be reusable, and no doubt in Australia new data centres are designed from that point of view. Eventually the value of the revenue produced falls below the energy cost.

Figure 7: us_opex_by_utilisation

You don’t need to be an expert to know that the population, at large, generally has concerns about anything different or new. Anything that increases productivity is immediately suspect because some jobs will disappear. The jobs that disappear will be much more obvious than the new jobs that are created.

Throughout history, from at least the invention of the wheel, productivity has resulted in some jobs being lost but a greater number of new jobs being created. Unions will never, ever understand this and these days it’s pretty hard to get the message through to the broader population.

Still, it must be true because the number of employed people tends to grow, and – except in Australia – productivity tends to increase. The invention of the car saw horse jobs decline but auto jobs increase far more. Etc.

Until late 2024, opposition to US data centres was overwhelmingly local – county-level zoning fights about noise, water, traffic, viewshed and lost farmland.

By mid-2026 it is also a generalised national political story, driven by three converging shocks: PJM capacity-auction prices clearing 833% above the prior auction in July 2024 and re-clearing at the new administrative cap a year later; a sequence of FERC orders culminating in the December 2025 PJM co-location order; and a wave of state legislation in 2025-26 (more than 300 bills tracked by MultiState) seeking to make hyperscalers pay their own grid costs.

The clearest single piece of evidence that opposition has broadened is the Washington Post-Schar School Virginia poll: voter “comfort with a new data centre in your community” fell from 69% in 2023 to 35% in March 2026.

The Trump administration is the most pro-data-centre actor in the system – Stargate was unveiled at the White House on the second day of the second Trump term, followed by Executive Order 14148 accelerating federal permitting and four nuclear executive orders in May 2025. State public service commissions across the partisan spectrum are pushing back through new rate classes, minimum-bill provisions and stranded-cost protections.

The local issues have not gone away – if anything they have intensified, with the xAI Colossus Memphis air-quality case becoming a national environmental-justice flashpoint, and the Prince William Digital Gateway court loss demonstrating that procedural land-use challenges can defeat 17 GW of approved development. But the generalised cost-shifting and AI-environmental-impact frames have now overtaken purely local quality-of-life concerns as the political driver.

Noise. The constant low-frequency hum from chillers and cooling fans is the most-cited grievance in densely-developed clusters. Loudoun County’s industrial noise cap is 55 dB at residential property lines; one CloudHQ measurement reached 90 dB at the boundary, with at least a dozen 2024 complaints against Vantage (WUSA9, 2024).

Water. The single most-cited concern in arid-state and drought-stressed locations. Of 25 projects cancelled in 2025, water use was raised in over 40% of cases (Common Observer, 2026).

Air emissions. xAI’s Colossus campus in Memphis is the headline case. University of Tennessee aerial-imagery analysis documented at least 35 gas turbines on site (xAI’s previously-disclosed count was lower); Earthjustice and SELC have argued the site became the largest single industrial NOx source in the 11-county Memphis area, with documented capacity to emit more than 1,700 tonnes of NOx, 180 tonnes of particulate matter, 500 tonnes of carbon monoxide and 19 tonnes of formaldehyde per year.

In Loudoun County alone, approximately 4,700 diesel backup generators are now permitted with about 12 GW of nameplate capacity.

Farmland and rural character. Saline Township, Michigan, is the case-study reference point. The township board voted 4-1 in March 2025 to deny rezoning for the 1.4 GW Stargate (Related Digital / Oracle / OpenAI) project. Two days later the developer sued under Michigan’s exclusionary-zoning doctrine, arguing that because Saline Township had no industrially-zoned land at all, a “necessary” use could not be excluded altogether. The township settled within weeks; construction began; the Michigan PSC approved the DTE supply contract in December 2025 with conditions; Fortune’s May 2026 reporting confirms the facility is operational on a path to 1.4 GW. Residents secured roughly $14 million in community benefits including fire-department funding and farmland preservation (Fortune, 2026; Michigan Public, 2025).

The shift from local to generalised opposition runs through residential electricity bills, environmental-justice litigation, federal regulatory action and state legislation. The political coalition is cross-cutting; the regulatory consequence is a structural rate-design pivot that will outlast the news cycle.

The PJM Interconnection 2025/26 Base Residual Auction, held in July 2024, cleared at $269.92/MW-day across most of the RTO — an 833% jump from $28.92/MW-day in the prior auction. The Dominion zone cleared at $444.26/MW-day; Baltimore Gas and Electric at $466.35/MW-day. The 2026/27 auction, held July 2025, cleared at the new $329.17/MW-day administrative price cap across the entire RTO, with cleared volumes only 139 MW above the reliability requirement (PJM Interconnection, 2024, 2025; Utility Dive, 2025b).

The PJM Independent Market Monitor (Monitoring Analytics) attributed the 2025/26 increase principally to data centre demand: in a November 2025 filing, it estimated that data centres accounted for 63% of the 2025/26 auction price increase, equivalent to $9.3 billion of the $14.7 billion total capacity bill. Across the most recent three auctions, data centre forecasts contributed 45% of $47.2 billion in cumulative capacity costs (Monitoring Analytics, 2025; Utility Dive, 2025a).

The industry counter-view, advanced by SemiAnalysis in March 2026, attributes the price step-change primarily to a 34.4 GW (20%) supply contraction — Capacity Performance accreditation reform after Winter Storm Elliott (-14 GW), coal closures (-10 GW) and renewable derating and other reductions (-10 GW) against only +4.5 GW of new build — with data-centre demand setting the auction’s clearing level rather than causing the spike (SemiAnalysis, 2026a).

Public service commissions across the partisan spectrum moved through 2025-26 to put data centres into separate rate classes with minimum-bill provisions and stranded-cost protection. The structural shift is the most consequential element of the entire backlash because rate-design changes operate for decades.

Legislators across both parties introduced more than 238 data centre bills across all 50 states in 2025; over 40 were enacted in 21 states.

Microsoft committed in 2024 to “next-generation” zero-water-cooling data centre designs and matched 100% of its global electricity consumption with renewables in 2025 (Microsoft, 2025). However, Microsoft is reported to be reconsidering its 24/7 carbon-free energy matching pledge in light of AI demand growth (Data Center Dynamics, 2025; GeekWire, 2025). Google maintains its 24/7 CFE moonshot for 2030 but its operational emissions have risen sharply with AI (Google, 2025).

Yes. The evidence is consistent across three independent measures:

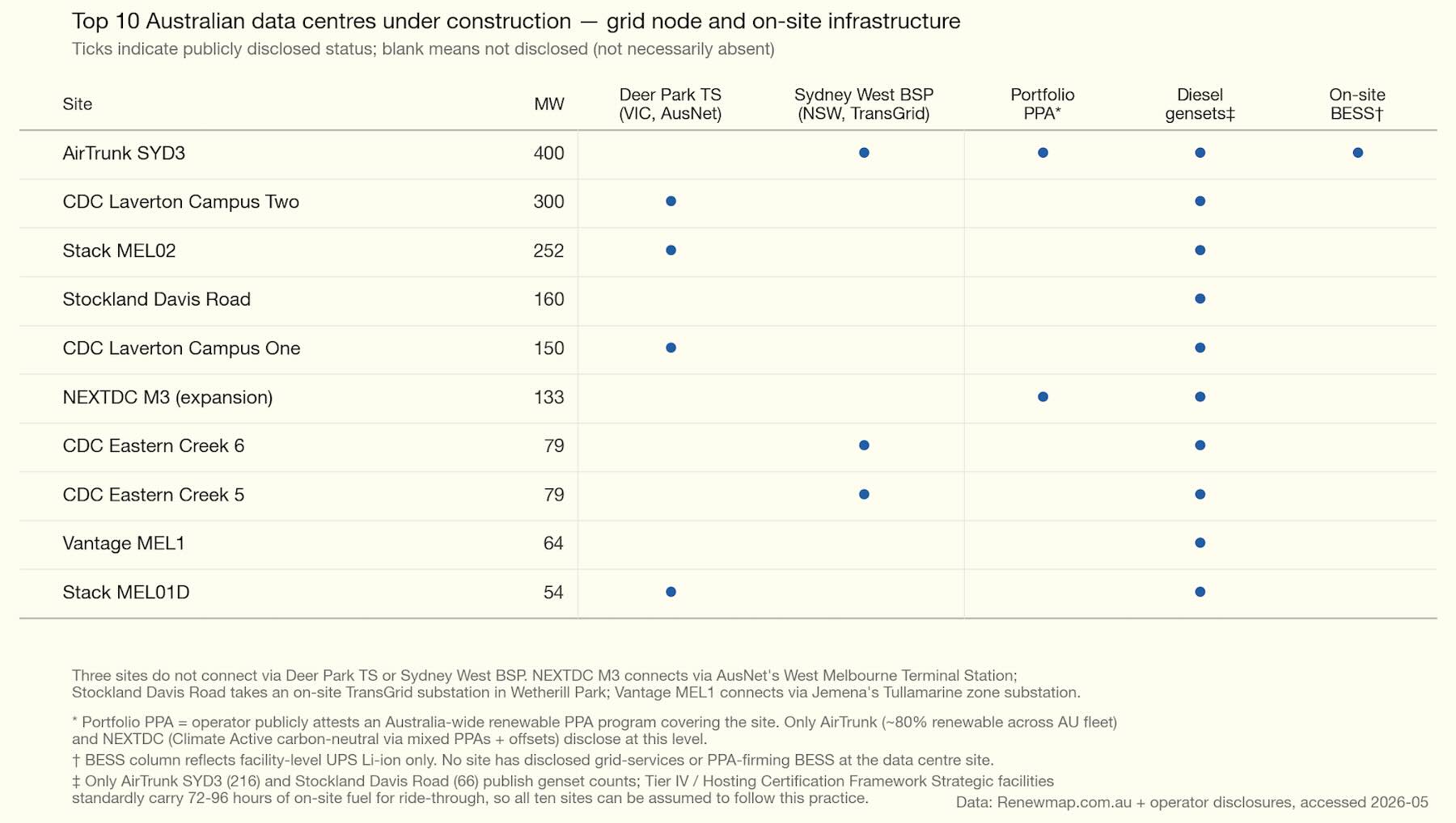

At present Australia is structurally quite different to what is happening in the USA.

Figure 8: dc_australia_overview

Figure 9: dc_australia_top10_matrix

Australia has had no equivalent of the US political moment. Local opposition is real but small in scale, council-led, and procedurally weak – the State Significant Development pathway in NSW and ministerial call-in in Victoria have routinely overridden council objections.

There is no Australian equivalent of the Data Center Watch $160bn-blocked tally, no Title VI civil-rights litigation, no Washington Post-Schar School voter-comfort poll showing a 34-point drop, no PJM capacity-auction shock translating into residential bill politics, and no Talen-style co-location decision requiring AEMC to write new rules.

There is:

The Albanese government released the National AI Plan and accompanying Australian Government’s expectations of data centres and AI infrastructure developers on 11 December 2025 (Australian Government, 2025).

The five expectations are: national interest, energy transition (with explicit “full share of new grid connectivity” and “underwrite new renewables” language), water sustainability, skills and jobs, and research/innovation.

The instrument is not legally binding — the enforcement device is the bilateral Memorandum of Understanding. Microsoft signed an A$25bn MoU in April 2026 binding itself publicly to the Expectations (Microsoft and Australian Government, 2026); Anthropic signed the first AI-developer MoU in April 2026 (Anthropic and Australian Government, 2026).

The joint statement of 23 February 2026 is signed by twelve organisations: Clean Energy Council, Smart Energy Council, Electrical Trades Union, ACF, WWF-Australia, RE-Alliance, Climate Energy Finance, Nature Conservation Council NSW, Environment Victoria, Queensland Conservation Council, Sunrise Project Australia and Carbon Zero Initiative.

The four demands are: (1) all new data centres matched 100% with additional renewable generation from day one; (2) operators pay full grid-connection costs; (3) demand-flexibility mechanisms integrated; (4) workforce training contributions.

An emerging trend in Australia and in the USA is that data centres have to bring their own power. In the USA the multi-billion-dollar data centres can do this – and are doing it – with facility-specific power, e.g. their own gas generators. Nevertheless each of them is then backed up with its own diesel sets.

In Australia there is a coalition of groups that want each data centre to provide its own power or perhaps to show it has caused sufficient renewable generation to be built.

In my opinion – and this stems from my background as a finance analyst and from a decade of work on aluminium smelters – this is basically a dumb idea, or at least should not be implemented the way it sounds.

The basic point is that it’s no more sensible for a data centre to be stand-alone, disconnected from the grid, than it is for the individual house, even if the house has a battery.

The grid is in effect a giant insurance scheme that means every consumer can access the common supply when needed, even if the consuming unit is largely self-sufficient.

Imagine a data centre running from a wind farm and batteries. You need a lot of batteries. The same goes for a data centre running off solar and batteries. Same rules apply.

Now imagine a data centre in Melbourne and one in Sydney. It’s raining in Sydney and sunny in Melbourne. If they are both powered by solar, and assuming away transmission (or assuming it’s done in markets rather than physically), then fewer batteries are needed because the batteries at the centre still receiving sun can be used to help the centre where it’s raining.

Equally, adding a wind farm would reduce portfolio volatility, meaning less firming and lower overall cost. To me this is so bloody obvious as to be embarrassing to write out. But it seems to be completely over the heads of the “must power itself” agitators.

One way forward might be an independent company – call it “Data Centre Power Supply” – to provide firmed power. Each data centre would buy shares in the company according to its share of the power required, and the company would build a portfolio of firmed power. Such portfolios already exist. Snowy Hydro for instance already has one, but the data centres can’t buy a share of Snowy Hydro.

Snowy is not the only option: Tilt or Brookfield Renewable Australia (Neoen) could offer such a portfolio. Of course “co-ops” basically end up fighting with each other, but the point is there are vast savings to be made.

The most obvious example would be batteries at the Transgrid and Deer Park terminal stations that could supply services to all the data centres at those locations – at a minimum reducing diesel usage, but also being used to firm renewable power that the data centres might contract.

Equally, if the data centres contracted a diverse portfolio – even though they are close to co-located – the shared firming might lower their overall costs.

.

Policy review will investigate settings for Australia's 2030 and 2035 emissions reduction targets.

Kane Thornton has moved from the peak renewables body to data centres, now the presumed…

Australia's government-run "carbon neutral" certification scheme is being wound up. It is good news for…

Victoria's newly appointed energy minister says the state will go ahead as planned with Australia's…

A promise of banning gas while waving through “gas firming” and “gas peaking” with unlimited offsets leaves…

Plans for a potentially massive new wind farm start federal environmental assessment, proposing up to…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}