Australian Energy Minister Chris Bowen looks at Home Battery systems during a visit to SolarHub in Canberra, Wednesday, May 14, 2025. (AAP Image/Lukas Coch) NO ARCHIVING

A system sometimes learns from what others had already begun to see.

AEMO has now publicly acknowledged something many consumer-energy observers had already been seeing: household batteries can reduce pressure on the grid before they are enrolled in sophisticated virtual power plants, which aggregate batteries and other devices so they can be coordinated as a single flexible resource.

The signal becomes clearer when two recent speeches are read together. In late May, Daniel Westerman told large energy users at the Energy Users Association of Australia National Conference that flexible energy use is becoming a genuine system asset, with value for reliability, markets and whole-system costs.

He also noted that a similar opportunity exists for virtual power plants, but that more work is needed to develop the right value proposition for homes and smaller businesses with batteries, electric vehicles and other responsive devices.

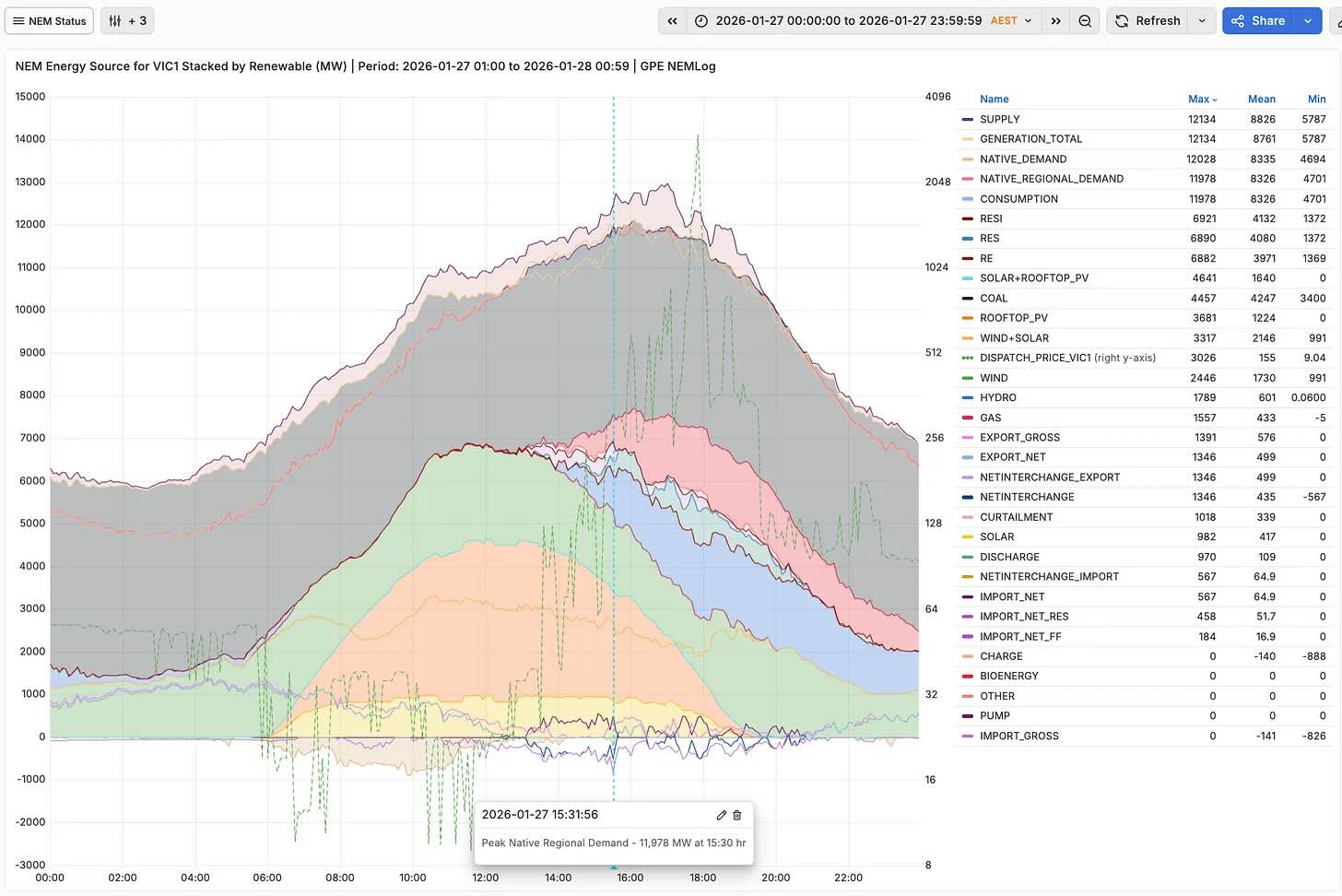

Two weeks later, at Australian Energy Week 2026, he gave the household version of the same story. During Victoria’s record peak demand event on 27 January, many home batteries were not operating as sophisticated, centrally controlled virtual power plants.

They were doing something simpler: storing solar energy during the day, sometimes charging during lower price periods from retailers, then supporting homes through the evening peak.

Westerman described many of these batteries as operating in “passive mode”: not centrally orchestrated, but still changing the household’s draw from the grid.

The impact was material. At the time of record peak demand, homes with batteries were drawing 1.4 kilowatts less than homes with solar alone. AEMO described this as an 80% reduction during record demand. In context, this appears to mean the battery homes in the comparison were drawing about 80% less from the grid than solar-only homes at that moment, with stored energy serving the home instead.

The important point is not that household battery value suddenly appeared. The important point is that value already visible at the consumer edge is now moving into the formal system conversation.

A system changes first in practice, then in language, then in design.

The May speech gives the prequel to the passive battery story. AEMO was already saying that demand is no longer only something to be forecast and supplied. It is becoming something that can participate.

For large energy users, this is already familiar. Their operations can shape reliability, system security and market outcomes, particularly at critical moments. Many are investing in electrification, on-site generation, storage, controllable load and digital energy management.

This shows three things:

This is the first step in the wider framing. AEMO had already recognised flexible demand as system-relevant among large users. The later household battery example extends that logic to the consumer edge.

A name can reveal the viewpoint from which something is being judged.

There is a subtle asymmetry in the language across the two speeches. Large energy users are described as active participants. Household batteries are described as mostly operating in passive mode.

That word, passive, is worth pausing over.

A battery charging from solar and discharging into the home during the evening is not passive in any physical sense. It is doing work. It is changing the household’s grid draw. At scale, it changes demand shape. It is passive only from the perspective of central orchestration.

The distinction matters:

So the useful correction is simple:

Passive to central dispatch does not mean passive to the system.

Once that is clear, the question changes. It is no longer whether passive batteries count. It is how much value sits outside the formal market view.

Recognition often arrives after the pattern has already formed.

The public discussion after the Energy Week comments sharpened this point. Some consumer-energy observers argued that AEMO should not have been surprised, because the effect of passive home batteries had already been visible through analysis, public data and consumer-grid advocacy. The phrase Consumers’ Grid captures the underlying claim: households are already shaping the system before the formal market has fully caught up.

That phrase is useful if treated as more than a slogan. The consumers’ grid is what happens when household devices, retail offers, default settings and ordinary energy decisions begin to reshape demand at scale.

The wider discussion also shows why this is contested. It quickly moves from passive batteries to V2H/V2G, distribution-connected batteries, plug-in batteries, storage-as-a-service, renters, capital access, consumer resilience and the cost of orchestration.

Three points follow:

The passive battery is not a new phenomenon. What is new is that its system value is becoming harder for the formal market conversation to ignore.

A useful correction can become misleading if it turns into a new binary.

One of the strongest responses to AEMO’s comments was the simple observation that household batteries did not need VPP orchestration to deliver value.

As a correction, that matters. It cuts through the assumption that household batteries only become valuable once aggregated, orchestrated and dispatched through a virtual power plant. The Victorian peak example supports that correction: those batteries were not mostly acting as sophisticated VPP assets, yet they still reduced demand at a critical moment.

Victoria’s record peak demand event on 27 Jan 2026 | GPE NEMLog

But the better conclusion is not that VPPs do not matter. It is this:

VPPs are not required for household batteries to create system value. They may still help measure, reward and deepen that value where consumers trust the offer.

Orchestration therefore has to earn its place.

It should be judged by three tests:

The issue is not whether passive batteries work. They do. The issue is whether the system can recognise their contribution without immediately trying to over-control it.

Not every useful contribution needs to enter through the same door.

The two speeches and the industry response point towards a better model: a ladder of participation.

Large users already sit near the more mature end of this ladder. They can invest in controls, respond to market signals and shape demand deliberately. Households may begin in an another place, with batteries serving the home first and the system second.

But there is one important precondition. Each step beyond household-first use depends on the consumer allowing it. Technical capability is not permission. A battery may be able to respond to a signal, share data or join a VPP, but that does not mean the household has agreed to those uses.

A practical ladder might look like this:

This ladder matters because each step asks for something different.

Household-first flexibility asks little beyond installation and sensible settings. Signal-shaped flexibility asks for clear incentives, transparent rules and the ability to opt out. Orchestrated flexibility asks for trust, data sharing, commercial arrangements and confidence that the household will not be disadvantaged.

That is why the industry should not treat VPP participation as the only sign of maturity. A household battery can be useful before it becomes a market instrument, and it should only become one on terms the consumer understands and accepts, where deeper participation creates fair household value and helps reduce wider system costs or pressure.

Sometimes coordination begins before anyone calls it coordination.

The Victorian example also shows that passive behaviour may not be entirely passive. Some batteries were supplementing solar charging during retailer lower-price periods.

That detail matters. Retail tariffs may already be doing a first layer of coordination that market design often assumes must come through dispatch. A simple retail offer can influence when batteries charge. A default battery setting can affect evening demand. A consumer trying to reduce bills may also reduce pressure on the grid.

This creates both opportunity and risk:

The point is not to romanticise uncoordinated behaviour. Simple signals still need visibility and design. Consumer energy has household, retail, distribution and system layers.

A shared system is weakened when participation depends too heavily on private advantage.

The phrase Consumers’ Grid is powerful because it names a real shift. Consumers are no longer only using electricity. They are storing it, shifting it, responding to prices, investing in devices and altering demand shape.

But the phrase also creates a test.

If the consumers’ grid mainly means homeowners with capital, suitable roofs and conventional batteries, then it is only a partial public idea. Renters, apartment dwellers, low-income households and people without access to rooftop solar need pathways too.

The wider industry discussion surfaces this tension through debate about V2H/V2G, distribution-connected batteries, plug-in batteries and storage-as-a-service.

The equity question can be put simply:

The consumers’ grid will only be a useful public idea if it includes consumers who cannot install a conventional home battery.

The best systems do not begin by demanding participation. They begin by understanding it.

The policy and market-design lesson is not complicated, but it does require discipline.

The system should not ignore household-first battery value because it is not fully dispatchable. It should also not assume every useful battery must be pulled immediately into a formal market product.

A better path is threefold:

This avoids two mistakes.

It avoids treating non-orchestrated batteries as irrelevant just because they are not dispatchable. It also avoids treating every household battery as if its natural destination is full market control.

Orchestration should not be assumed. It should earn its role by creating more value than it extracts in cost, complexity and loss of consumer control.

When read alongside AEMO’s earlier EUAA speech and the industry response that followed, the discussion of passive batteries reveals something important about the next phase of consumer energy.

Large users are already recognised as active participants in the energy system. VPPs remain an important pathway for smaller users, but the right consumer value proposition is still being worked through. Household-first batteries now show that useful flexibility can exist before full orchestration arrives.

The passive battery is not a new phenomenon. What is new is that its value is becoming harder for the formal market conversation to ignore.

The task is not to make every household look like a large energy user, or every battery look like a virtual power plant. It is to recognise the layers of value already emerging on the demand side, shape them carefully, and invite deeper coordination only where trust, reward, consumer permission and system need justify the step.

A system becomes more intelligent when it learns to value what people are already doing well.

Australia's biggest operating wind farm has set a stunning new record, becoming the first in…

State-owned utility says it is in discussions to invest in non-lithium technologies with up to…

Batteries have been protecting consumers from price spikes in most states over summer. But they…

State Electricity Commission CEO Chris Miller on how the government-owned energy company is filling gaps…

Australia’s electricity prices ignore location, even though the grid doesn’t. This mismatch drives congestion, curtailment,…

What began as a plan to fix a cold, draughty terrace evolved into a 25-year…

{kind=link}