A leading energy consultant is predicting a 15-fold increase in the deployment of battery storage over the next decade and a half, as the world’s car fleets turn electric and as huge, multi-gigawatt hour battery storage projects replace coal and gas.

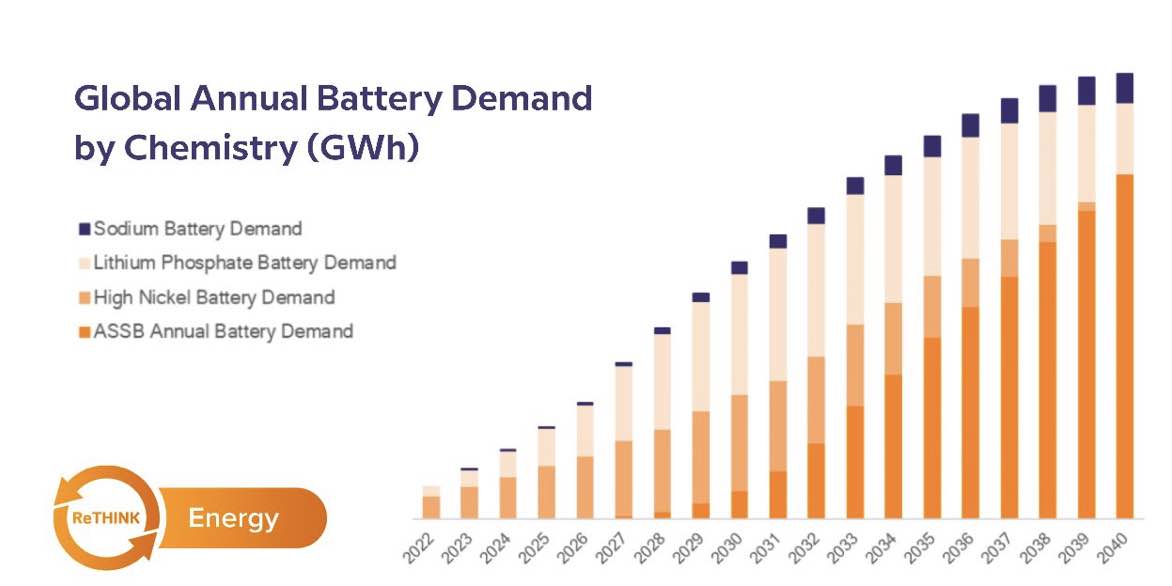

The forecast by Rethink Energy also suggest lithium iron phosphate batteries will come into their own during the late 2020s as stationary storage exclusively switches to this chemistry, and as key regions swap it in due to longer product lifespans and that anticipated drop in demand for very long-range batteries.

Nickel-based batteries will remain popular in North America but even those EV drivers will conform to the new technology “due to the need for safe, long-lasting batteries rather than facing replacement costs for batteries with a high variable cost due to global commodity prices”.

For stationary storage, Rethink says the focus will be on the deployment of increasing duration energy storage systems, which is currently dominated by <4-hour systems using lithium-ion batteries.

“We believe that with more renewable energy deployment, longer duration systems will be required,” it says.

“This will require different technologies due to the insufficiency of li-ion as a commercially and technically viable option in the long duration sector.

“Alternative chemistries will fill this gap in the >6-hour segment as they drive down costs prior to 2030; this will be a mix of flow batteries and other chemistries like nickel-hydrogen which have superior technical characteristics for supporting the long-duration energy storage sector.

“The falling cost of these batteries will drive large deployments of multi-GWh projects which directly replace incumbent assets like coal and gas peaker plants globally, though this will initially be focused in China, the US, and then Europe in order of expected capacity by 2030.

Come the 2030s, predictions become more difficult, the consultancy says. It thinks solid-state batteries will not only be viable, but there will be “significant quantities” vying for market share.

The consultancy’s predictions come as demand for electric vehicles, combined with an increasingly urgent realisation that renewable-heavy grids need some level of firming, are creating a perfect storm for battery makers.

The International Energy Agency says the automotive battery industry alone was using 550 GWh of units in 2022, while S&P Global says lithium-ion battery production capacity generally was 2.8 TWh at the end of the March quarter and should grow to 6.5 TWh by 2030.

Europe will not be able to avoid dependence on China even for lithium iron phosphate battery supply, as smaller makers on the continent are already dependent on the Asian giant for technology, wrote Rethink Energy lead analyst Connor Watts.

“Europe will be increasingly dependent on Chinese batteries, not too dissimilarly to how Russia made it dependent on oil and natural gas,” he wrote.

“While not selling its soul to the devil, it makes for a very fitting analogy for companies risking Chinese involvement in operations despite an evolving geopolitical environment. Ford and Tesla to an extent are also among this group due to the pair’s deals with CATL.”

Solid state batteries are also likely to see Japanese car makers being phased out in preference of those from China – everywhere bar the US where tariffs on Chinese cars are still at 27 per cent. Rethink believes these tariffs are likely to remain in place for some time.

Furthermore, even when it does begin to wind down the punitive tariffs, the US will need to continue with subsidies for battery makers to maintain any competitiveness Chinese manufacturing capacity.

Solid state batteries are, according to a number of companies including Quantumscape, CATL, Solid Power, BYD, Qingtao, and ProLogium, on the cusp of commercialisation.

These companies are promising solid state batteries for vehicles on the market by 2025-26, with the likes of Toyota and Nissan staking their electric credentials on the technology.

Rethink’s Watts says all-solid-state batteries (ASSB) promise energy densities of 450 -500 watt hours (Wh)/kg, significantly increasing potential electric vehicle range while reducing the bill of materials associated with battery production.

This is better than nickel-based batteries with a 300 Wh/ kg at the pack level.

The first residential solid state battery might be already on its way: Amptricity in the US says it will start delivering in the third quarter this year what it says is the world’s first solid state home battery.

And it is also being proposed as a stationary storage alternative.

In June 2022, Spanish energy company Iberdrola bought a stake in Basque solid state storage company Basquevolt, saying “liquid electrolyte lithium batteries are reaching maturity and that the next technological breakthrough to truly unlock the true potential of energy storage must come from the solid state”

Basquevolt plans to have prototype cells and a pilot line in play by 2025 and commercial production in 2027.

Solid state batteries are exciting because they are more energy dense than the current electrolyte-based lithium-ion batteries, meaning they can be smaller, weigh less, and — in theory — aren’t prone to catching fire and exploding.

However, scaling the technology up from the micro-sizes used in watches and phones has proved difficult and expensive.

One problem is the instability at the edges of the electrodes and the solid electrolyte radically shortens a solid state battery lifetime. Some researchers, such as those at Honda, are trying different coatings between the layers, but this adds yet more cost and time.

The Rethink report casts doubt on whether solid state batteries can be the saviour of car companies that have, to date, failed to embrace an electric future.

“ASSB development has been plagued by technological setbacks for years now but with the transparency of some companies within the space and the success of WeLion’s semi-solid-state batteries (SSSB) currently on roads in China we can expect commercialization in 2025/2026 for most companies with mass production ramping up from 2028 into the 2030s,” the report said.

“The relative success of this will decide the fate of companies, Toyota is completely banking on its battery’s success since it is still completely lacking significant internal battery manufacturing and a comprehensive EV lineup it only plans to make available by 2026, far later than its main Western competitors.

“It’s difficult to see a world in which the transition works out for the company or the smaller Japanese companies that closely follow its decisions like Honda.”

There is something for everyone in China’s coal data, but the direction that the energy…

Santos beat greenwashing claims in court, and while the ruling exposes the limits of climate…

A flurry of new solar and battery projects has appeared in AEMO's grid management system,…

One of Australia's fiercest defenders of nature and biodiversity has thrown his hat into the…

Lauri Myllyvirta, lead analyst at the Centre for Research on Energy and Clean Air, on…

As early works – and a legal challenge – get underway for Marinus Link, the…

{kind=link}