Source: Free Pik

Since 1990, Australia’s iron ore exports have surged dramatically, rising from approximately 96 million tonnes per year to nearly 900 million tonnes annually by 2024.

This extraordinary growth was largely propelled by China’s unprecedented infrastructure expansion, which absorbed vast quantities of Australian iron ore to feed its booming steel industry. However, this sustained export growth now faces a clear inflection point.

With China’s infrastructure boom nearing completion and the country pivoting decisively toward electric arc furnaces (EAFs) that primarily use recycled scrap steel rather than freshly mined iron ore, Australia’s long-established iron ore export model confronts a structural decline. 80% to 87% of Australia’s iron ore goes to that single country.

As China reduces its dependency on iron ore, Australian producers face the urgent imperative of transitioning toward higher-value, lower-carbon steel products. Australia’s strategic pivot toward green steel is not just an environmental or technological choice—it is becoming a fundamental economic necessity as traditional export markets begin to contract.

Pivoting from raw iron ore to processed green steel dramatically enhances Australia’s export revenue potential; currently, iron ore exports fetch roughly $A110 per tonne, while green steel can command upwards of $A800–$A1,000 per tonne.

Shifting just 20% of Australia’s iron ore exports, approximately 180 million tonnes annually, to green steel products could potentially increase annual export revenues by tens of billions of dollars, representing a transformative economic opportunity.

In recent years, Australian policymakers have signaled a robust shift toward aligning with global best practices in green steel, drawing inspiration from leaders in Europe, North America, and East Asia.

The focus has crystallized around several foundational technologies and approaches—most notably electric arc furnaces (EAF), direct reduced iron (DRI) using low-carbon fuels, and the strategic integration of renewable energy. Despite these promising developments, significant gaps remain, particularly around scale, speed of implementation, and domestic market incentives for green steel uptake.

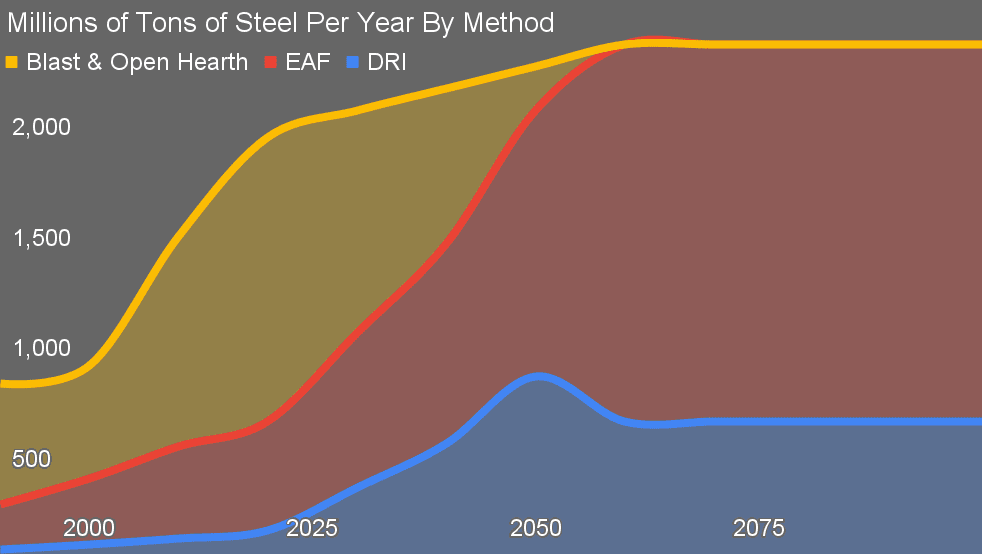

Projection of global steel production and decarbonization by method through 2100 by author

In my current projection of global steel through 2100, the world sees a significant shift, with 75% of demand met by scrap steel fed through electric arc furnaces, and various direct reduction of iron technologies delivering the 25% of new steel required.

China is currently manufacturing half of total global tonnage of steel annually, but is pivoting to use its 260-280 million tons of domestic scrap. The country didn’t approve a single new blast or open hearth furnace in 2024 after decades of rapid growth in the sector.

Other markets don’t have the conditions for success for nearly as rapid a growth in steel demand as China did in 1980, including the fundamentals of their economic growth models, so as China’s demand declines the developing world will only just replace it.

As a note, when I revisit this projection, the insights gained from my projection of the plummeting demand for cement over the century will be firmly in mind. A great deal of steel is used for reinforced concrete and we won’t be building with reinforced concrete to nearly the extent we have been for the past 100 years. That will likely bring this projection down at least a bit, possibly into decline in total tonnage.

Electric arc furnace technology, leveraging recycled steel scrap, represents the lowest-hanging fruit for significant emissions reductions globally. Australia, historically lagging behind in this regard, has now moved strategically to boost domestic EAF capacity. Federal funding directed towards Liberty Steel’s EAF installation at Whyalla, alongside Western Australia’s initiative to establish a dedicated EAF recycling facility in Collie, represents concrete progress.

These moves align Australia with international benchmarks such as those in the United States, where approximately 70% of steel production already uses EAF technology, albeit usually with preheating with natural gas rather than 100% electrification at present.

To fully exploit this opportunity, however, Australia should invest more aggressively in scrap collection infrastructure and develop stringent standards for scrap segregation, enabling a broader range of steel grades to be produced domestically. The potential to become a scrap importer for steel powered by Australia’s massive green electricity opportunities is present as well, requiring a shift of ports from pure export to import-export.

Another promising strategy involves mandating green steel content in public procurement, following the successful model employed in the European Union. By explicitly requiring that government-funded infrastructure projects such as bridges, railways, public buildings, and renewable energy installations use a minimum percentage of domestically produced low-emission steel, Australia would create strong and reliable market demand.

This procurement-driven approach could significantly reduce market uncertainty, stimulate private-sector investment in green steel manufacturing, and accelerate Australia’s transition away from raw iron ore exports toward higher-value, sustainable steel production.

Direct reduced iron technology, including hydrogen-based reduction, holds considerable promise as a long-term decarbonization solution. Internationally, pioneering projects like Sweden’s HYBRIT have set a high bar, and Australia appears cautiously optimistic in adopting similar technologies.

However, recognizing the practical constraints surrounding immediate large-scale hydrogen deployment, Australian industry and government have embraced natural gas as a transitional fuel. BlueScope, for instance, has identified natural gas-driven DRI at its Port Kembla facility as an interim measure capable of significantly cutting emissions compared to traditional blast furnaces.

Australia has the opportunity to become a global pioneer by exploring biomethane as a direct replacement for natural gas in the DRI process, and using electricity for process heat. Given Australia’s extensive agricultural resources and burgeoning biogas sector, this renewable methane approach could significantly accelerate emissions reduction while waiting to see if hydrogen costs ever come down into the range of profitability.

The exploration of biomethane and other alternatives to hydrogen is strongly recommended, as the same fundamental problem hydrogen for energy faces — green hydrogen is far too expensive and not getting cheaper — is killing green hydrogen steel proposals globally.

In parallel with incremental transitions such as EAF and biomethane-driven DRI, Australia has the opportunity to position itself as an innovation leader in breakthrough technologies like molten oxide electrolysis (MOE). MOE, championed internationally by companies like Boston Metal, directly electrolyzes molten iron ore, eliminating carbon emissions entirely if powered by renewable electricity.

Despite significant global enthusiasm for this technology, Australia’s current engagement is largely indirect, occurring through research initiatives by organizations like CSIRO and strategic investments by Australian mining giants such as Fortescue. Unlike the European Union and the United States, which have explicitly funded and supported dedicated MOE pilot projects, Australia has not yet provided specific policy backing for large-scale demonstrations.

A similarly disruptive opportunity arises from China’s emerging high-temperature “flash” ironmaking process, announced in late 2024, which builds directly upon Professor Zhang Wenhai’s earlier breakthrough in ultra-efficient copper smelting technology. This process reduces iron ore to molten iron within seconds by exposing iron ore powder to extremely high temperatures generated electrically or through plasma, entirely bypassing traditional coke-based methods.

While Australia’s domestic policies have not yet directly engaged with flash ironmaking, the country’s recently announced NeoSmelt electric smelter pilot in Kwinana, WA, exhibits conceptual alignment, suggesting Australia could rapidly adapt to or even collaborate with Chinese developers. Actively pursuing such partnerships or independently funding research into similar flash-smelting approaches would position Australia to capitalize on this revolutionary technology.

From a broader policy perspective, Australia’s current efforts reflect an emerging alignment with international changes such as the EU’s Carbon Border Adjustment Mechanism. Becoming a low-tariff provider of green steel to iron poor Europe is a strong potential growth area.

Australia faces an urgent need for clearer national strategies and explicit timelines to phase out coal-based steel production, akin to the roadmap established by Germany. While the federal government has made significant investments, such as supporting BlueScope’s interim blast furnace relining and the transformative green steel transition in Whyalla, these measures need clearer long-term targets to ensure emissions align with mid-century net-zero objectives.

Australia’s policy landscape already reflects several key strengths: the integration of climate policy with industrial strategy, proactive collaboration between different government levels and industry stakeholders, and the embrace of technological diversity to manage risk and uncertainty. The strong regional focus — tailoring policies to the specific needs of industrial hubs such as the Pilbara, Illawarra, Whyalla, and Collie — demonstrates commendable sensitivity to local economic and social conditions.

Nevertheless, critical gaps remain evident, notably around the speed and scale of commercial deployment, the comprehensive development of supporting infrastructure and skills, and, most urgently, the creation of strong demand signals for domestically produced green steel.

These challenges are surmountable and represent significant opportunities. Australia’s potential to evolve from merely exporting raw iron ore to becoming a global powerhouse in green iron exports is enormous, offering substantial economic upside as international markets increasingly demand low-emission steel.

Integrating steel plants with dedicated renewable energy sources, such as offshore wind farms or large-scale solar installations, could substantially enhance the competitiveness of Australia’s industrial base. By strategically positioning itself at the forefront of innovations such as biomethane DRI, MOE, and high-temperature flash-smelting, Australia could develop unique technological expertise, creating high-value export opportunities beyond traditional commodity markets.

Australia is well-positioned to leverage strategic international alliances, particularly with established Asian steel producers and European technology leaders. Such alliances could accelerate technology development, share risks and costs, and secure early markets for Australia’s emerging green steel products.

Transitioning to green steel offers Australia significant domestic economic benefits—revitalizing manufacturing, generating skilled employment opportunities in regions undergoing industrial transition, and creating a robust, exportable skills base that can service the global green industrial revolution.

Australia’s current moment represents a genuine opportunity to redefine its role in the global steel supply chain. By aggressively addressing existing policy gaps, ramping up strategic investments, fostering robust domestic demand, and embracing innovation, Australia can transform its rich natural resources into lasting competitive advantage in a low-carbon world.

Williamsdale battery in Canberra to fund two rooftop solar and battery storage systems for local…

Another outage at a major coal unit triggers price spike and supply concerns, highlighting vulnerability…

The Essential Services Commission has banned a second company in as many weeks for allegedly…

AGL is making more money from customer margins and its new big batteries, but is…

AGL to create a new funding vehicle, using other people's money, to develop its major…

US companies sign deal to build giant sodium batteries for US data centres, and also…

{kind=link}