In the second in my series on the crisis besetting the National Electricity Market (NEM) in eastern Australia, I look at the tightening balance of supply and demand.

Australia’s NEM is witnessing an unprecedented rise in spot, or wholesale, prices as market conditions tighten in response to a range of factors.

As shown above, spot prices are typically highest in summer, due in large part to the way extreme heat waves stretch demand. The historical summer average across the NEM is around $50/MWhour. As recently as 2012, summer prices were as low as $30/MWhour. With only a few days to go in the 2017 summer, prices are averaging a staggering $120/MWhour on a volume-weighted basis. Many factors have played a role, including hot weather, and the drivers vary from state to state.

In South Australia, the high prices have been accompanied by a series of rolling black-outs culminating on 8th February. Spot prices are more than twice last summer, on a volume-weighted basis, and three times the summer before that. Volatility has increased markedly, as evidenced by the way the volume-weighted price has diverged from the averaged spot price.

But the price rises and security issues have not been restricted to South Australia, with Queensland and New South Wales experiencing steeper rises in percentage terms. Current Queensland volume-weighted prices are averaging $200/MWhour, some 300% above the long-term summer average.

On the 12th February new demand records were set in Queensland, with prices averaging $700/MWhour across the day. New South Wales narrowly averted load shedding on 10th February as temperatures and spot prices soared. So far, the exception has been Victoria, where summer prices have remain relatively subdued, at levels not far above the recent average.

Demand for electrical power varies over a range of time-scales, from daily, weekly to seasonal, as well as with longer-term economic trends.

A key determinant in how much power is needed on any given day is the maximum daily temperature. As shown below, the maximum daily demand marks out a characteristic boomerang shape when plotted against maximum daily temperature. The boomerang bottoms out at temperatures of around 25°C when air conditioning loads are at a minimum.

As illustrated above, demand increases significantly in response to heating loads as the weather cools below 20°C and cooling loads as the weather warms above 30°C.

The difference in demand across the weather cycles can be substantial. For example, in South Australia the maximum daily demand varies from around 1500 megawatts on a day with a maximum temperature of 25°C to around 3000 megawatts during heatwaves when the temperatures exceed 40°C. With minimum daily loads under 1000 megawatts, this implies well over half the generation capacity in South Australia is for peaking demand, with much of it sitting idle most of the time waiting for extreme hot weather events. In an energy-only market like the NEM, such peaking capacity demands extreme pricing accompany its dispatch in order to recoup costs. In reality, to manage risks such capacity is normally hedged at a cap-contract of around $300/MWhour.

Similar patterns apply in other states, although in percentage terms the range is less severe. In Queensland the increase between 25 and extreme degree days, which top out at about 37°C in Brisbane, is about 2000 megawatts or approx 30%.

A comparison of the figures above show some subtle but important differences in the South Australia and Queensland markets. Notably, the diagrams show that annual demand in Queensland has been rising progressively over the last four years, while it has been static in South Australia. The extreme weather of Sunday 12th February set a new demand record in Queensland, and well above any previous weekend day. In contrast, the 8th February peak in South Australia was lower than previous peaks. To understand why spot prices spiked to similar levels in the different regions requires a deeper dive into the local market conditions.

One reason for seasonal variability in prices is the natural variability in weather conditions, and particularly the frequency and intensity of heat waves. As illustrated below, the 2017 summer in Adelaide has been rather normal in terms of weather extremes, so far with only six days above 40°C compared to seven last summer and thirteen in the 2014 summer. To date, the mean maximum is around 29.7°C , more-or-less spot on the average over the last five years. As such weather variability would not seem to be the key factor driving the recent dramatic rise in spot prices.

The most significant change in the South Australian market last year was the closure in May of its last coal fired-power plant – Alinta’s 520 megawatt capacity Northern Power Station. Along with questions about long-term coal supply, Alinta’s decision to close had a lot to do with the low spot prices back in 2015.

Back then, spot prices were suppressed on the back of a fall in both domestic and industrial demand as well as the addition of new wind farms into the supply mix. As shown below, the rapid uptake of solar PV in South Australia had impacted the demand for grid based services, especially during summer, limiting price volatility, and affecting generator revenue streams via a lowering of forward contract prices. In combination, the conditions made for a significant excess in generating capacity, or capacity overhang.

Despite the falling average demand, and a changing load distribution, the peak demand during the recent heat wave reached above 3045 megawatts in the early evening of 8th February (at 6 pm Eastern Australian Standard Time). That was 340 megawatts lower than the all time South Australian peak of 3385 megawatts for South Australia on the 31st January 2011. The peak on February 8th was accompanied by a spot price of $13160/MWhour.

With the closure of Northern, any comparison with previous peak demand events should factor in any demand previously served by Northern Power Station. Before its closure Northern contributed around 420 megawatts power on average over the summer months. Without that supply available this year, the February 8th peak effectively exceeded the previous peak by around 80 megawatts in adjusted terms.

Queensland has experienced a hot summer with the maximum daily temperature in Brisbane reaching 37°C for the first time since 2014, and an average daily maximum of 31.2°C (at the time of writing). That is about one degree above the average of recent years. However, with only four days with a maximum temperature above 35°C, compared to five in the summer of 2015, weather effects seem unlikely to fully account for the extraordinary rise in spot prices this summer.

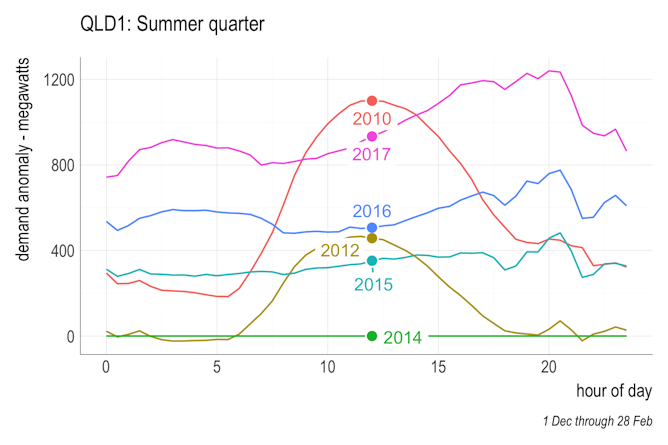

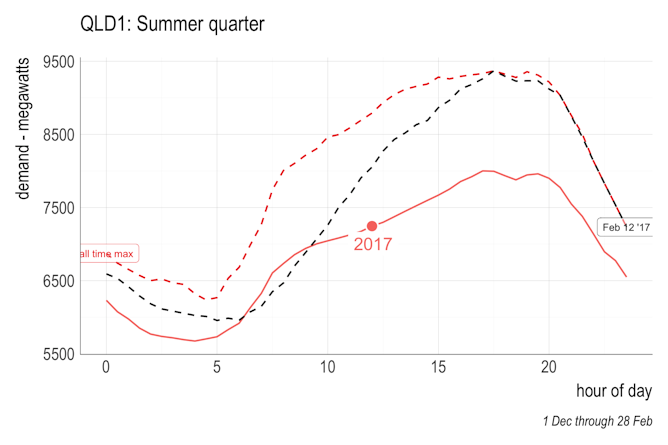

In detail the Queensland market differs from other regions in the NEM in as much as it is the only region to have experienced significant demand growth in recent years. Mapping the change of demand growth over the years, by time of day, helps reveal the drivers for market tightening, as shown below firstly in absolute terms, and then in relative terms normalised against 2014.

Between 2009 and 2014, summer demand fell by about 400 megawatts (or 6%), with the greatest change occurring in the middle of day. This pattern is akin to the signal in South Australia shown above, and reflects how the growing deployment of domestic rooftop PV was revealed to the market as a demand reduction.

Since, 2014 summer demand has grown appreciably across all times of day, skewed somewhat towards the evening. Relative to 2014, demand is up by almost 800 megawatts across the board, and by as much as 1200 megawatts at 8 pm. The ~800 megawatt base increase in demand can be attributed in large part to new industrial loads associated with the commissioning of the LNG export gas processing facilities at Curtis Island.

In terms of extreme events, it is notable that February 12th this year set a new Queensland demand record at 5.30 pm of 9368 megawatts (at the half hour settlement period) with a spot price of $9005. This is extraordinary given it was a Sunday, a day which normally sees demand down several percentage points on corresponding weekdays with similar temperature conditions.

Victoria is the exception to the trend of rising spot prices, with the summer prices of 2017 not much above long term average. In part, the relatively subdued prices can be attributed to the absence of

extreme heat in southern Victoria so far this summer. The mean maximum daily summer temperature in Melbourne stands at about 27°C, slightly below average of the previous five years. So far there have been no days with temperatures above 40°C, compared to eight in 2014 and four in 2016.

The dominant factor in subduing the Victorian markets prices is likely to be the ongoing fall in demand. In the year to 18th February, demand in Victoria fell by 200 MW. This follows a persistent reduction in demand that has seen a fall of almost 500 megawatts over the last three years, equivalent to 9% of average demand. As shown below, the contrast with Queensland is stark, and reflects significant reductions in industrial demand stemming from the closure of the Point Henry aluminium smelter in August 2014 (Point Henry consumed up to 360 megawatts) and more recently the reduced demand from the Portland smelter on the back of damage caused by an unscheduled power outage on December 1st, 2016. While power capacity in Victoria was reduced by the closure of the 150 megawatt Anglesea coal-fired power plant in August 2015, the cumulative demand reduction over the last decade has led to substantial capacity overhang. All that is set to change with the closure of the 1600 megawatt Hazelwood power station, slated for the end of March.

The figures shown in the previous sections reveal that peak demand events are stretching the power capacity of the NEM in unprecedented ways, for a variety of reasons. The tightening in the demand-supply balance is driving steep price rises that, if sustained, will have widespread repercussions. For example, a $20/MWhour rise in the Queensland spot price translates to a notional annual market value of $1 billion, that must eventually flow through the contract markets. With summer prices already more than $100/MWhour above last year, the additional costs to be passed onto energy consumers may well tally in the many billions of dollars.

In South Australia, the market tightening follows substantially the reduced supply stemming from the closure of the Northern Power Station.

In Queensland, the market tightening is being driven substantially by industrial loads such as the new LNG gas processing facilities. To the extent that the LNG industry is a significant driver, it is a heavy excise to pay for the privilege of exporting our gas resource. The makings for a policy nightmare, should the royalties from our LNG export be outweighed by the cumulative cost impacts passed on via our electricity markets.

It is important to note that the electricity market is designed so that prices fluctuate significantly in response to the normal capacity cycle, as capacity is added to or removed from the market following rises and falls in demand. In small markets, such as South Australia, the spot price fluctuations over the capacity cycle can be extreme, because the capacity of an individual large power plants can represent a large proportion of the native demand.

Although not large in terms of total capacity by Australian standards, Northern’s 520 megawatt power rating represented around 40% of the South Australia’s median demand. That made Northern one of the Australia’s most significant power stations in terms of its regional basis size. Its withdrawal has dramatically and abruptly reduced the capacity overhang in South Australia. Spot prices were always going to rise as a consequence, because that is the way the market was designed. In addition, Northern’s closure has also increased South Australia’s reliance on gas generation, and it has concentrated market power in the hands of remaining generators, both of which have had additional price impacts beyond the normal market tightening.

In both Queensland and South Australia, the rises in spot prices is signalling the growing tightness in the market. Under normal circumstances that should serve to drive investment in new capacity. The lessons of Northern show that any new capacity in South Australia will need to be responsive to the changing pattern of demand, unless the market rules are changed.

Further, both regions have questions about the adequacy of competition. Both are sensitive to the impacts of parallel developments in the gas markets, which have made gas-fired power production much more expensive in recent times. In the case of Queensland this is greatly exacerbated by the extra demand from the LNG gas production facilities.

Finally, these insights have importance for predicting how the markets the will react to the impending close of the 1600 megawatt Hazelwood Power Station in Victoria, all topics I hope to consider in following posts in this series.

Source: The Conversation. Reproduced with permission.

A community benefits find will share $50 million across a series of “legacy projects” for…

In a record six months of investment, the Clean Energy Finance Corporation helped break Austalia's…

Brisbane-based battery innovator gets its first chunk of Arena funding towards building a gigawatt-scale factory…

A last-minute submission gives an unexpected take on debate over a proposal to raise fixed…

A day after announcing full commercial operation of its Supernode battery in Brisbane, Quinbrook has…

Spanish police have made arrests after man died from electrocution last year after breaking into…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}