Tesla recently launched its Powerwall 2.0 battery at a price per kWh stored that is less than half the price of its first battery. My previous article looked at the annual charge that a household that installed 5 kW PV+ Powerwall 2.0 battery would pay. Such customers would use the grid for back-up supply and to export surplus PV production that it does not use. That article compared this “PV+battery+grid” option to the annual charge that a customer would pay for “grid-only” supply (i.e. a customer without PV and battery).

For the comparison it used the average of grid-only market offers in South Australia, firstly with conditional discounts and secondly without conditional discounts. This article extends the analysis by looking at how the “PV+battery+grid” option compares when such a customer selects the best (i.e. cheapest) grid offer for residual supply and exports, and compares this to every retail offer for “grid-only” supply.

This article will be followed by a third article looking at the implications of the developments in battery costs for network service providers.

The methodology used here, as before, is to calculate an annual charge for the PV+battery+grid combination by annuitising the capital outlay (after sales taxes) for PV and battery and adding to this the charges for grid purchases and subtracting the revenue from the export of surplus PV production.

For grid purchases and exports we have used the same volume assumptions as before but here, instead of assuming the average fixed and variable grid prices and feed-in rates, we have scanned all retail electricity offers to find the best deal (the one that offers the combination of the highest export revenue plus lowest grid charges). This best deal offers a credit of $101 per year to the customer (the worst deal is a charge of $320 per year).

Interestingly, since annual exports to the grid from a 5 kW PV + battery are so much greater than the small grid purchases, the best offer is not a time-of-use tariff, but a time-invariant block tariff that happens to offer a materially higher feed-in rate than the other retailers offer.

The resulting total annual charge for the PV+battery+grid combination represents the lowest annual cost for such customer. This is then compared to the annual cost (after sales taxes) of grid-only supply on all retail offers to households in South Australia. The dataset is established by assuming firstly that customers meet the terms of all conditional discounts in those offers and secondly assuming that they don’t receive any of those conditional discounts. This results in a dataset of 225 offers.

These offers are then ranked from highest to lowest and compared to the PV+battery+grid combination. As before, all retail market data is taken from MarkIntell (www.markintell.com.au) which includes all market and standing retail offers in all electricity price fact sheets from all retailers in South Australia in a dataset updated on 25 October 2016. All assumptions on battery and PV costs and so on from the first article continue.

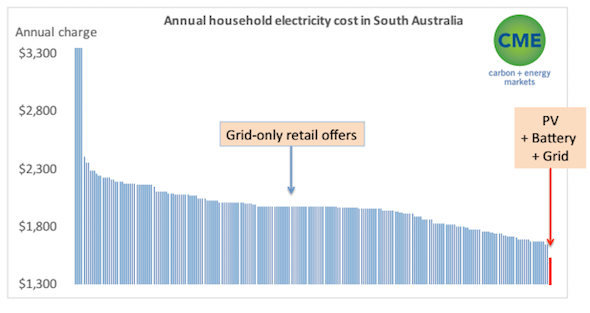

The results of this analysis are shown in the chart below.

The chart shows that the combination of PV+battery+grid, taking advantage of the best grid offer, is $123 per year cheaper than the cheapest grid-only offer ($1,645 per year) and $449 lower than the median grid-only offer ($1,971). In other words, our typical 4,800 kWh household in Adelaide can beat all contemporary grid-only offers by installing a PV + battery system and selecting the best retail offer to provide their residual grid consumption and to export their PV production surplus.

This comparative advantage is reflected in payback periods for PV+battery that I estimate to be between 5 years (assuming the alternative was that the customer selected the most expensive grid-only retail offer) and 10 years (assuming the alternative was that the customer selected the cheapest grid-only retail offer) and 8.5 years for the median offer.

The outcome shown in the chart is the best that a PV+battery +grid customer can get in the current market. If they do not have the skill or good fortune to select the best offer for their exports and residual grid consumption, their annual electricity cost could rise from $1,522 (with the best offer) up to a maximum of $1,943 (if they selected the worst offer). Evidently, even if they selected the worst retail offer, a household with PV+battery would still be better off than if they were supplied on the median grid-only offer.

Many retailers in Australia already offer to install PV and batteries, for a fee, but they have not been major players in this business. Some retailers offer to finance or own PV installed on a customer’s roof and to sell the electricity back to customers at a fixed price, but again we understand this is not popular. Households own the vast majority of rooftop PV systems. Its hard to imagine that they will think differently about batteries, particularly if PV + battery is sold as a package.

Of course not all customers will be able to accommodate a suitable PV + battery system. The economics may not be as attractive for customers that are much smaller or much larger than the 4,800 kWh per year assumed. Renters and those in apartments might find it difficult or impossible to take advantage of the opportunity. But PV+battery will be viable for a large part of the residential and probably also the commercial and agricultural market.

Finally, I will caveat this analysis by stressing that markets change all the time. Massive interconnector development in SA seems increasingly likely and with a concentrated wholesale market and high gas prices, there seems to be substantial pressure for continued high grid prices. On the PV+battery side, who knows what the future holds. It seems that even the most bullish forecaster has consistently under-estimated the rate of cost decline and technology improvement.

Analyses like these should be repeated frequently and time series established and published. But it seems pretty clear that with PV+battery economics now so compelling, and with a large market potential, it is likely that the retail electricity market is going to change profoundly. Quite what those changes are, and how retailers will respond to them remains to be seen.

Bruce Mountain is the Director of Carbon and Energy Markets and co-founder of MarkIntell

Related Reading: Tesla’s price shock: solar + battery as cheap as grid power

This article was originally published on RE sister site One Step Off The Grid. To sign up for the weekly newsletter, click here.

There are 30 big batteries operating across the main grid, and they have cemented their…

There are hopes techniques borrowed from the oil and gas industry can boost the viability…

Labor and the LNP might be approaching the federal election from diametrically opposite ends of…

Australia's first privately owned wind farm, which began operations in 2001, will cease in 2027,…

South Australia loses patience with Gupta's GFG Alliance and seizes control of the Whyalla steelworks,…

The six turbine wind project was first proposed to avoid a new high voltage power…

{kind=link}