Source: Peabody Energy. This file is licensed under the Creative Commons Attribution-Share Alike 4.0 International license.

The US-based coal miner has just paid over $A5 billion dollars to acquire some of the biggest greenhouse gas emitting coal mines in Australia, and may now be in the driver’s seat to determine whether or not Queensland’s metallurgical coal sector will reach its decarbonisation goals.

The acquisition includes super-emitting metallurgical mines such as Moranbah North, Grosvenor, Aquila and Capcoal, as well as Dawson open-cut mine.

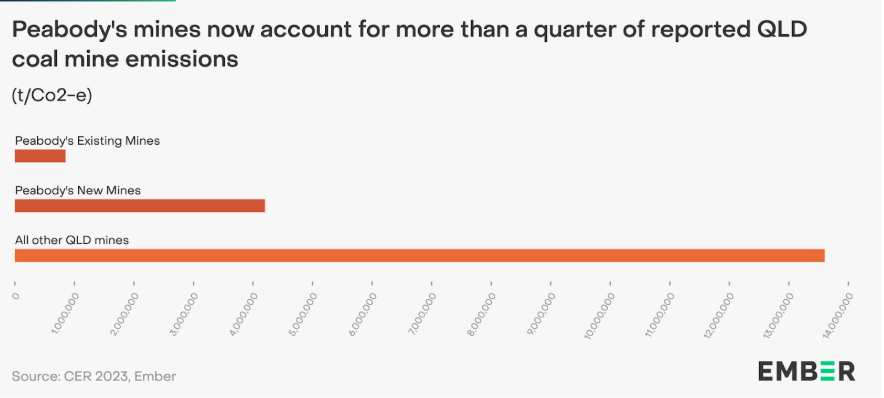

Collectively, these new mines reported emitting the equivalent of over 4.2 million tonnes of carbon dioxide in 2023, and according to Peabody, these mines have an average mine life greater than 20 years.

In 2023, four of the five mines reported their emissions under the Safeguard Mechanism, reflecting close to a quarter of all reported scope 1 emissions from QLD coal mines. When combined with the existing mines under Peabody’s ownership, the company now represents upwards of 28 per cent of QLD’s coal sector emissions.

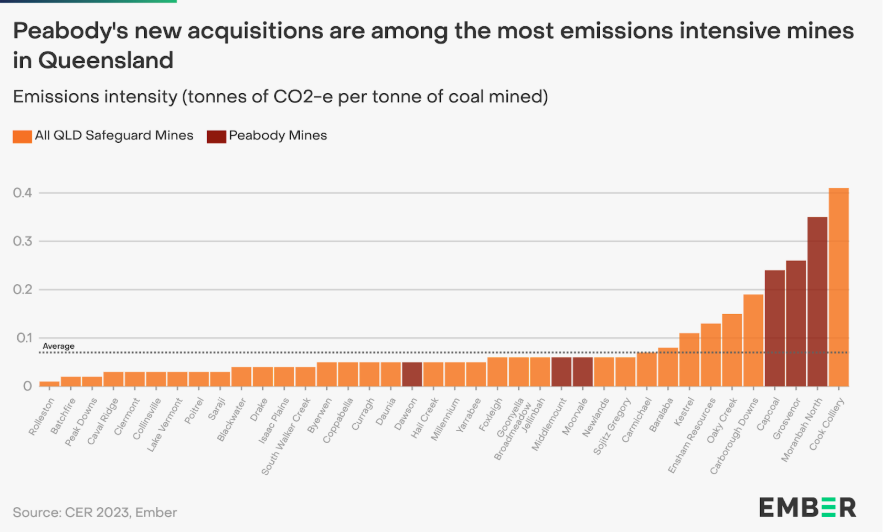

These are also some of the most emissions intensive mines in the country. Capcoal, Grosvenor and Moranbah North mines, which all reported their greenhouse gas emissions under the Safeguard Mechanism last year, release more than four times as much greenhouse gasses as the average of all other Safeguard mines in QLD.

Even after significant investments in pre-mine drainage, these three mines on average release the equivalent of 200 kg of carbon dioxide for every tonne of coal they dig up. That’s before any of that coal is shipped around the world and burned.

The biggest emitter, Moranbah North, releases the equivalent of 350kg of carbon dioxide per tonne of coal. This is five times the average for large coal mines in QLD, reporting under the Safeguard Mechanism.

Part of this is due to the nature of underground mining. As you dig deeper, especially into higher grade metallurgical coals, you release significant amounts of methane that is embedded into the coal seam.

For many underground more than 90 per cent of their scope 1 emissions share comes from this “fugitive” methane. These “fugitive” emissions makes these mines the highest intensity emitters in the country, under current reporting requirements. But these emissions can be addressed.

Underground mines release the majority of their methane through the mine’s ventilation shaft, which is a source that can be significantly reduced through strategic investments in methane capture technology, both prior to, and during mining.

This is exactly what Anglo American has been doing for years across Grosvenor, Capcoal and Moranbah North coal mines.

The company invested in “excess of USD $100 million per annum, in methane capture infrastructure” in pre-mine drainage over the last few years. As a result, it reported capturing and mitigating up to 60% of its potential methane emissions last year.

These results require ongoing investments. Without which, the emissions from these mines would be even higher. Peabody has a critical choice to make here.

Prior to the sale, Anglo American was also conducting extensive trials to explore the opportunities of abating the remaining emissions, by installing emissions mitigation technology on the mine’s ventilation shafts.

This could potentially capture up to eighty per cent of the mine’s remaining methane emissions, with technology on the market reportedly able to do so at close to AUD$30-$35 per tonne.

This is well below the current ACCU market spot price of $41.50.

Considering that Moranbah North, Grosvenor and Capcoal mine were still among the country’s top 10 biggest super-emitters even after successful pre-mine drainage, it’s clear there is still a lot that needs to be done.

While Peabody will likely be initially focussed on restarting the Grosvenor coal mine after its explosion earlier this year, the company’s decisions around methane mitigation could shape the future of decarbonisation across QLD’s metallurgical coal sector.

This was a priority for the previous Labor government in QLD, which announced $520 million in up-front joint-investments to fast track decarbonisation across metallurgical coal mines. So far, funds have been granted to develop two power plants that will run on pre-drained coal mine methane at South Walker Creek and Kestrel coal mines. Both of these grants were driven by voluntary engagement from the mine owners, something that Peabody could now tap into, as the fund is likely still under-subscribed.

However, the biggest opportunities for decarbonisation would be to capture the majority of emissions leaking out of underground mine ventilation shafts. This is exactly what Anglo American was recently exploring, with the likely solution to utilise a regenerative thermal oxidiser technology, that was first installed on Australian coal mines back in the mid-2000’s.

The mitigation tech solution saw no major safety issues at the time, but lost commercial interest in the mid 2010s due to the incentive roll-backs of the climate wars. Since then technologies such as catalytic oxidisers have also shown significant promise.

Following the acquisition of some of the country’s biggest emitting coal mines, Peabody now has a critical decision to make. These new mines could increase its annual reported scope 1 emissions well beyond 5 million tonnes per year (CO2-e).

With plans to bring on the underground Centurion mine in 2026, the company’s emissions should be expected to increase further. The potential Safeguard reduction requirements could be substantial, considering they are tailor-made to target high intensity mines.

But they also have a unique opportunity.

As the owners of some of the most emissions intensive facilities in Australia, they could also be the best placed to lead on emissions reductions. The mine’s previous owners have already made a kick-start on the decarbonisation journey, and have the blue-prints ready to go to bring down the remaining emissions.

There should also be ample opportunity to tap into further grants under QLD’s LEiP fund, to avoid significant pre-2030 penalties under the Safeguard mechanism.

As metallurgical coal mines, they should expect the steel market to be looking for low-emission products in the next few years, and increasing regulatory pressure to decarbonise from state, federal and international sources.

If the company expects the average lifespan of these mines to extend across the next 20 years, they would have ample time to earn a serious reward on upfront investments in decarbonisation, while ensuring they don’t miss out on potential premium opportunities.

While it might sound strange to call a couple of coal mines the climate acquisition of the year, I’m convinced that Peabody just stepped into the centre of Australia’s emissions reduction challenge.

The company and its investors now have the opportunity to tackle some of the most emissions intensive activities we have, and take a front-row seat in driving the resource sector’s decarbonisation.

Failing to do so, will only make the company vulnerable to increasingly tough regulatory sticks that could swing from a variety of directions, and may miss out on the medium term low emissions opportunities that are starting to arise from buyers around the world.

A coalition of energy and consumer groups is urging federal government to seize the global…

Safeguard Mechanism gives coal and gas companies "a free ride," new modelling shows, while other…

Applying for grid connections is like a fishing expedition. You lower your hook into the…

Australians have spent decades fighting over how much multi-national investors should pay for our resources.…

Transgrid details causes of the "contract failure" that has blighted delivery of Project EnergyConnect, as…

Stand-alone solar and battery systems used to upgrade upgraded remote rail crossings from “passive” –…

{kind=link}

{kind=link}