There is a new article from Cornell University that suggests that the emissions associated with the export and use of liquefied natural gas (LNG) from shale gas in the United States are higher than burning coal. Although this will be no great surprise to those who take an interest in this issue, there are two aspects of the research that are important contributions to the debate in Australia.

The first of these is the application of a 20-year Global Warming Potential (GWP) for methane, rather than the normally used 100 year value. The concept of the GWP to compare the emissions impact of different greenhouse gases (GHGs) goes back to decisions by the Intergovernmental Panel on Climate Change (IPCC) in the nineties.

There are two aspects to calculating the GWP of GHGs – their ability to absorb energy and the duration they remain effective in the atmosphere. Because these differ between gases GWP was invented as a way of comparing methane and other GHGs to CO2, giving rise to the “CO2 equivalent” (CO2e) values conventionally used.

The time period usually used for non-CO2 gases is 100 years, which probably seemed appropriate back in the 1990s. Methane (CH4) however, is a much more potent GHG than CO2, albeit with a shorter lifetime in the atmosphere.

When measured on (say) a 20‐year period it has more than 80 times the effect of CO2. In the midst of a climate crisis and a race for net zero emissions by 2050, clearly a GWP20 is more appropriate than GWP100. The use of GWP20 leads to increased CO2e values for methane of 82.5 instead of 29.8.

The second aspect of the research which is relevant is the more accurate capture of fugitive emissions from shale gas operations in the US from airborne methane surveys which identify major gaps in official estimates.

Australia’s National Greenhouse Gas Accounts report that fugitive emissions (from all sources) are around 11% of the total. A recent report from the Future Energy Exports Cooperative Research Centre states that reported fugitive emissions from the oil and gas sector were 21 MtCO2e in 2021 or around 20% of the national total.

However, a new report using the Open Methane mapping approach by the Superpower Institute identifies that methane emissions are likely to be around twice that reported for 20 coal and gas sites (which don’t include offshore gas projects).

There is global concern about under-reporting of methane emissions, leading to Australia joining the Global Methane Pledge working to reduce “methane emissions across all sectors by at least 30% below 2020 levels by 2030”.

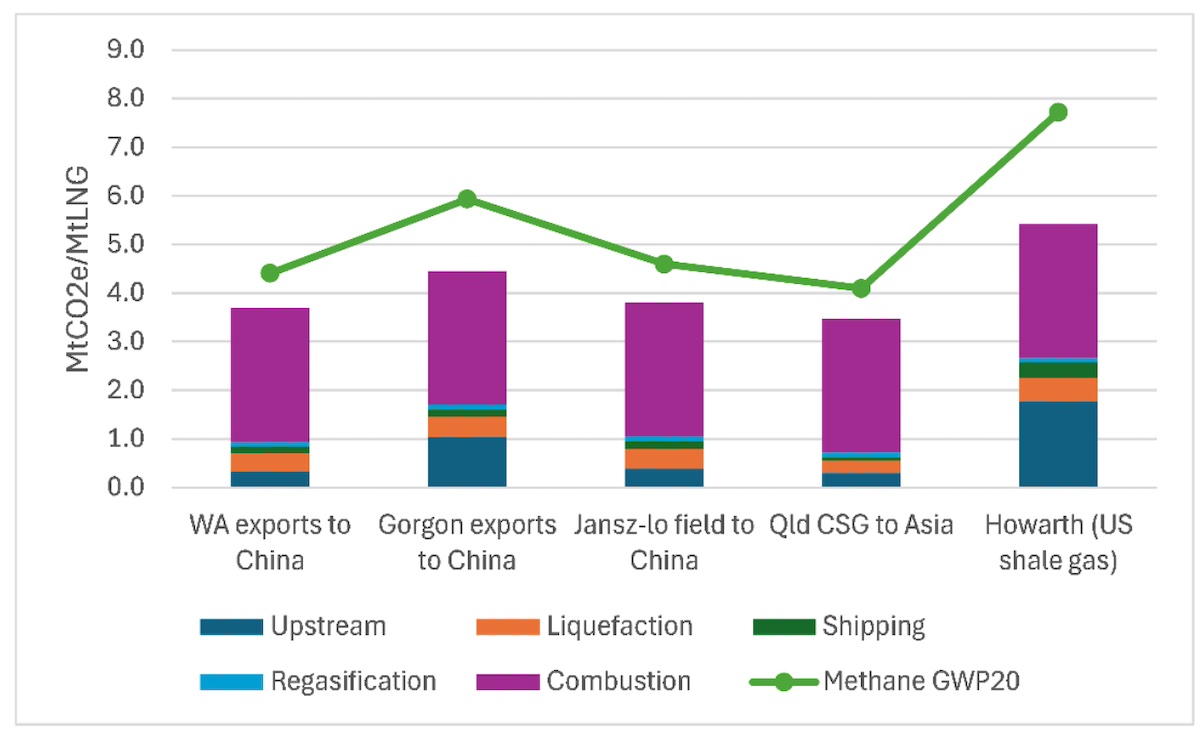

In 2022 CSIRO produced a report (funded by the Australian Gas Industry Trust) on GHG emissions from the LNG industry in Australia, also comparing these with internationally available data. I have compared the data from this report with the Cornell article by Robert Howarth.

The CSIRO report doesn’t include CO2 emissions from re-gasification (for all projects) and burning the gas in the importing countries so I have added that to the analysis set out below, assuming methane emissions using both GWP100 (approximate for the Australian projects) and GWP20.

The major differences between the Australian figures and those of Howarth relate to higher upstream emissions from shale gas production and the longer shipping routes for US gas. Of course, the Australian emissions likely would be higher if methane was accurately accounted for in line with the Howarth article.

Nevertheless, even with these figures, the Australian projects produce 50-115% higher emissions than if the gas was used domestically.

This illustrates a comparison between Australian LNG emissions and the U.S. shale gas reported by Howarth and the impact of using the more appropriate methane GWP20. The higher emissions associated with Gorgon are due to the high CO2 content of the gas itself. It should also be remembered that both the Australian and Northern Territory governments are set on seeing the Beetaloo project proceed, claiming it will:

– Deliver cheaper and more reliable gas across Australia for decades to come;

– Provide an additional source of gas for Liquefied Natural Gas (LNG) export.

Notably the projected emissions by CSIRO are strongly contested. The justification for continuing Australian LNG exports (we are the second largest exporter in the world after the U.S.) is:

“Australia is, and will remain, a reliable trading partner for energy, including Liquefied Natural Gas (LNG) and low emission gases. Australia’s ambition to become a renewable energy superpower will involve developing new, low emissions energy exports to support the energy security and decarbonisation efforts of our trade partners.”

This statement doesn’t, however, stand much scrutiny. Firstly, the importing countries (mainly Japan, China and South Korea) are all judged as having insufficient emissions reduction policies by the highly respected Climate Action Tracker, and so our exports of fossil fuels to them only assists in delaying the global transition.

The Institute for Energy Economics and Financial Analysis (IEEFA) reports on Japan:

“The resultant fall in LNG demand means that Japanese buyers have found themselves over-contracted, and are increasingly reselling the gas overseas. IEEFA has found that Japanese companies sold more than 30 million tonnes (mt) to third countries in FY2020, FY2021 and FY2022, peaking at 38mt in FY2021. This is more than Australia’s total LNG exports to Japan over those three years.

“The surplus LNG is often sold in Southeast Asia where Japanese utilities are cultivating demand. IEEFA found that Japanese “utilities are investing in midstream and downstream gas infrastructure, such as regasification terminals and LNG-fired power plants and offering engineering and consulting services to inform energy and power roadmaps across the region. Corporate strategies for Japan’s major LNG buyers aim to tilt revenue share towards overseas revenues.”

So in this case, our exports are also delaying action in Southeast Asia.

The reality is, of course, that the LNG industry is a huge contributor to government revenue and employer of Australians throughout their supply chain. According to McKinsey:

“Throughout the 2020s and beyond, the LNG industry is forecast to add around A$30 billion per annum to Australia’s GDP, equivalent to about 2 percent of the total. Depending on realised prices, LNG could contribute up to A$55 billion exports in 2020 – rivalling iron ore, Australia’s biggest commodity export today.”

Accordingly, no government will take on the LNG industry, irrespective of their contribution to global emissions and worsening climate change.

The sad reality is that we will decarbonise where there is little or no pain in doing so (e.g. domestic electricity using wind and solar that is cheaper than coal and gas) but have no appetite for aggressive action across the economy.

That would require policies that responsibly constrain both demand and supply, domestically and internationally, irrespective of the economics.

Transmission remains the fundamental building block to decarbonising the grid. But the LNP is making…

Snowy blames bad weather for yet more delays to controversial Hunter gas project, now expected…

In 2024, Renew Economy's traffic jumped 50 per cent to more than 24 million page…

In our final episode for the year, SunWiz's Warwick Johnston on the highs and the…

CEFC winds up 2024 with record investment in two huge transmission projects, as Marinus reveals…

Regulator says big energy players are manipulating prices to their benefit. It's not illegal, but…

{kind=link}