The rise and rise of home battery storage, spurred on by the success of federal and state rebates, is shaping up to shave hundreds of megawatts off future peak electricity demand on Australia’s biggest isolated grid, even as overall consumption continues to rise.

The Australian Energy Market Operator says peak demand on the Western Australia electricity market, or WEM, is being reduced by consumer-owned energy resources, including a combined rooftop solar capacity that is forecast to almost double from around 3.1 gigawatts in 2026-27 to 6 GW by 2035-36.

AEMO’s annual 10-year outlook for the WEM, the 2026 Electricity Statement of Opportunities (ESOO), is also forecasting that distributed battery capacity will grow from around 550 megawatts (MW) in 2026-27 to something more like 2,300 MW (2.3 GW) by 2035-36.

But it is the impact that this behind-the-meter solar and storage is expected have on the broader grid – and more specifically on future electricity demand profiles – that is the big turn-up from this year’s ESOO, published on Tuesday.

According to AEMO, the coordination of distributed energy resources (DER) through virtual power plants (VPP) is expected to reduce the need for grid-scale investment by approximately 200 MW in 2028-29, when it expects about 640 MW of batteries will be able to be orchestrated through the state retailer’s VPPs.

This is good news for a number of reasons, but as state government energy policy lead Jai Thomas puts it, the “absolute banger of a highlight” is that government-backed investment in consumer energy resources is working to meaningfully reduce the need for costly peaking gas.

“This is 200 MW of utility batteries or gas-fired generation not required – even at the 50% capacity price floor a saving for consumers of $49 million every single year,” Thomas writes on LinkedIn.

“The strong growth in household batteries is reducing evening peak demand as well as increasing daytime demand via battery charging, as these batteries are increasingly being coordinated to charge or inject into the grid by aggregators acting as a VPP,” the ESOO says.

“This often soaks up excess solar energy, even as rooftop solar continues to reduce daytime demand. These trends are forecast to continue.”

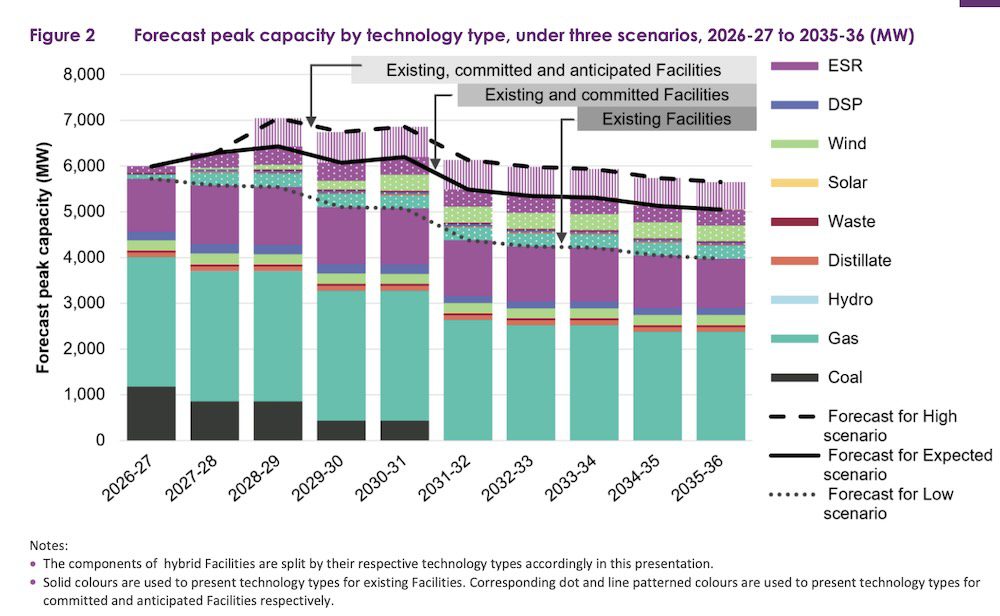

The report says WA’s peak reserve capacity target – RCT, or forecast of peak supply capacity required in the main WA grid (the SWIS) after taking into account the impact of DER – is forecast to rise from a 5,720 MW in 2026-27 to 6,323 MW in 2028-29, then to 7,454 MW in 2035-36.

Of course, as AEMO itself notes, the ESOO’s forecasts on peak demand will depend on “reliable communications and control systems, and effective integration of DER into market and operational processes” and on VPP buy-in.

To this end, and “to account for uncertainties around remote control and operational behaviour due to the early stage of development,” AEMO has assumed a 50 per cent availability factor for VPP-coordinated battery capacity.

WA has taken a slightly different approach to home battery rebates than other states, giving households the option to access a slightly more generous discount as well as a zero interest loan by “stacking” the federal Cheaper Home Batteries rebate with the WA Residential Battery Scheme.

But opting in to the state rebate also makes it mandatory to sign up to a virtual power plant – for a minimum of two-years – which is currently limited to two state-owned retailer offerings, with one alternative from Plico Energy (via Synergy).

Residential VPP buy-in has been considered to be particularly important for WA, which already has a huge amount of distributed solar testing the bounds of its isolated grid.

But evidence suggests customers are not yet sold on the benefits – and there has been some speculation that the approach WA has taken to its state rebate has set it behind the pace on what has been booming home battery uptake in other major NEM states.

In an update earlier this month, state-owned utility Western Power said Under more than 45,000 Western Australian households and small businesses had installed batteries under the Cheaper Home Batteries Program, but industry figures suggest only a fraction of this number – around 8,000 – have also signed up to a VPP.

But the jury is also out on just how important VPPs are to delivering the broader benefits of DER. AEMO chief Daniel Westerman recently made a point of highlighting the positive, system-wide impact that hundreds of thousands of “passive” home batteries are having on the grid.

“Even acting in passive mode, so a consumer with complete control over their battery, just soaking their own solar or using a free power period during the day, actually has enormous benefit to our grid, reducing their own costs and reducing the costs for everyone involved,” Westerman told the Australia Energy Week conference in Melbourne two weeks ago.

“If you had have asked us 12 months ago, would we have seen such an impact on on the grid from passive home batteries? I think we wouldn’t have pointed to such an impact.

“There is an opportunity for retailers to provide a value proposition to consumers to participate in a VPP, we do see that, and actually that benefits the grid even more, but ultimately this is a decision for consumers based on … the sort of propositions that they have.”

On the WA grid, AEMO says home batteries are also having the effect of increasing daytime minimum demand, which is the dippy part of the solar duck curve in the middle of each day when all of the solar feeding into the grid from rooftops can present a different set of problems to the market operator.

Beyond home batteries, AEMO expects a significant increase in grid-scale battery storage to further flatten peak electricity demand, and has upped its preferred storage duration from six hours in 2027-28 to seven hours in 2028-29, to help “meet a longer and flatter peak.”

According to the ESOO, a total of 1,666 MW of existing and committed battery storage is forecast to be operational on the SWIS by 2028-29 and a further 1,119 MW of committed generation and battery storage is forecast to be operational by 2030-31.

“If the 661 MW of anticipated projects are delivered in a timely manner, then capacity is forecast to be sufficient through to 2030-31,” the forecast says. “More investment will be required to mitigate potential shortfalls from 2031-32 onwards.”

More broadly, AEMO is forecasting an improved outlook for the WEM compared to its 2025 report, when it issued a call for six-hour batteries, as well as more wind and solar and transmission to transport it to help wean the state off coal in coming years.

All of the above still needed – a total of 1,661 MW of thermal generation is expected to exit the SWIS by 2035-36, the ESOO says, with more than half of this capacity “assumed to become unavailable or retire from 2031-32.”

But some of the urgency has been dialled back, thanks to the progressive delivery of more than 1,000 MW of new generation and storage by 2030-31, with even more projects in the development pipeline, and backed by the barrage of investment and installation behind the meter.

Rooftop solar is no small part of this: By 2035-36, AEMO expects distributed PV generation from household installations to offset the equivalent of 68 per cent of total forecast underlying residential consumption.

“The near-term outlook for the SWIS has improved, and reliability targets are expected to be met over the next three years,” AEMO executive general manager Kirsten Rose said on Tuesday.

“This improved outlook has been largely driven by strong investment alongside government-led initiatives,” she said.

Looking forward, the ESOO forecasts a steady upwards trajectory in overall electricity demand over the coming decade, rising 56 per cent to 31.9 terawatt-hours (TWh) in 2035-36.

AEMO says this growth is underpinned by the electrification of homes, cars and businesses and the projected influx of data centres, which appear as a separate category for the first time in the 2026 WEM ESOO.

“While strong investment has been observed to-date, more investment will be needed over the second half of the outlook period to meet demand growth and replace ageing thermal generation, which is expected to progressively exit the SWIS over the remainder of the outlook,” Rose says.

“We continued to see high investment interest with more than 2,000 MW of potential projects submitting expressions of interest in the 2026 Reserve Capacity Cycle, which procures capacity for 2028-29.

“The project pipeline is clearly strong, but it remains critical new generation and storage capacity is delivered on time, alongside planned transmission network augmentations.”

If you would like to join more than 29,000 others and get the latest clean energy news delivered straight to your inbox, for free, please click here to subscribe to our free daily newsletter.

AEMC commissioner Rainer Korte on what the new rules on reporting and data sharing will…

Developer says it is good to go on early works and construction of the largest…

AEMO says proof that grid forming battery inverters can deliver heartbeat of the grid will…

Days after lodging new plans for a more than 500 MW wind farm, Squadron dumps…

AEMO’S head of systems Nicola Falcon on the 2026 ISP and the importance of grid…

Flagship pilot program to set up 100 sites around the country to collect used solar…

{kind=link}