Source: Pxhere CC0

Imagine hopping on the bus, to be told by the driver that they’re expecting low passenger numbers today – so you’ll have to pay a higher fare to cover the costs. You begrudgingly agree, pay, and board the bus, only to find it’s completely full.

Now imagine this happens not just once, but every day that week. You and the other passengers paid more than necessary, while the bus company ends up making higher-than-normal profits.

It turns out, something similar is happening behind your gas bill.

Gas bills are made up of a combination of different charges, with one of the largest being network costs. These make up 40% of a typical gas bill, and over 60% in South Australia, Tasmania and Queensland.

Gas networks, like electricity networks, are considered natural monopolies. Regardless of which retailer customers choose, they don’t have a choice in the physical gas infrastructure they can connect to.

There is a risk that monopolies abuse their market power and force consumers to pay higher prices. To manage this, many gas networks in Australia are regulated by the Australian Energy Regulator (AER). Every five years, the AER determines the charges that gas networks can pass through to their consumers. These charges are set in a way that allows networks to recover their costs and make a reasonable profit allowance, set by the AER.

There are also a range of incentives that allow networks to exceed that profit allowance. These are intended to encourage activities that result in long-term efficiency improvements, benefiting consumers.

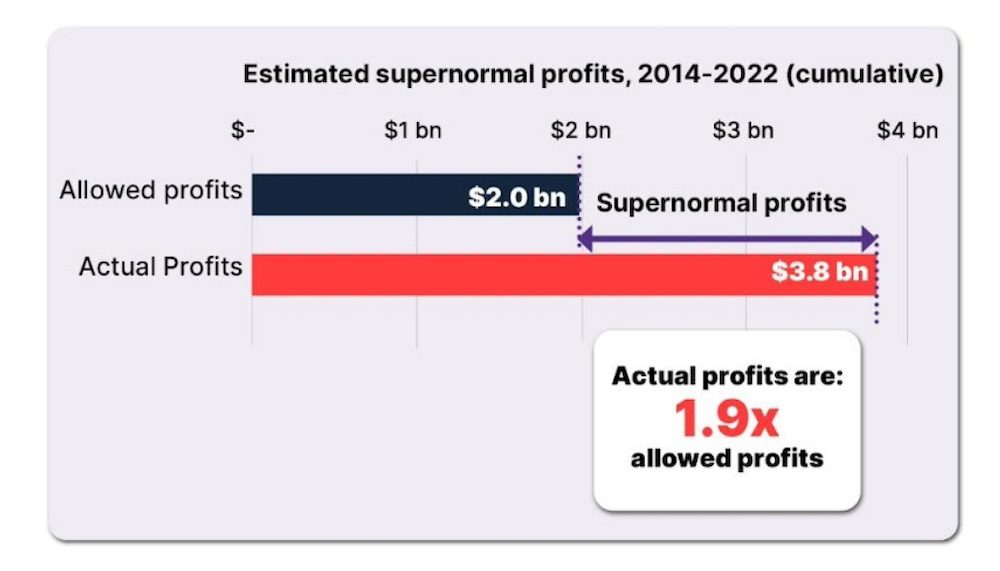

IEEFA recently undertook a simple piece of analysis, comparing the actual profits that regulated gas networks in Australia have made against their profit allowance. If the regulations were working as expected, we’d expect actual profits to roughly align with the allowance, or to exceed it by no more than 30%.

However, we found they were 90% higher than their allowance. In other words, actual profits were almost double allowed profits.

Source: IEEFA. Data includes all fully regulated gas networks.

The economic term to describe this difference is ‘supernormal profit’. Over the period we analysed, 2014-2022, regulated gas networks made $1.8 billion in supernormal profits, on top of their $2 billion profit allowance.

What does this mean for consumers?

Like all regulated gas network revenue, supernormal profits are extracted directly from consumers’ bills. We estimate that they add 5% to a typical gas bill. However, as we don’t know how these profits are divided across individual gas networks, this could well be higher for some consumers.

By anyone’s measure, making profits that are 90% higher than the regulator-approved allowance is an extraordinary outcome. However, given the incentive structures baked into gas network regulations, this raises the question: have these extraordinary profits corresponded to extraordinary long-term benefits for gas consumers?

Our report used data from the AER to understand what was driving supernormal profits.

The largest driver by far, was an effect termed ‘revenue over-recovery’. In other words, gas networks are making more revenue than expected. A 2023 review of gas distribution networks by the AER revealed that this has occurred in every year since at least 2011.

Source: AER.

To understand how this happened, we have to go back to the fact that gas networks are very large, asset-intensive businesses. The cost to maintain them is relatively fixed; it doesn’t decrease significantly if customer demand is low.

Setting fair charges for consumers to access the gas network is therefore a balancing act. To decide what a fair price is every five years, the networks must submit a forecast of how many customers they expect to serve, and how much gas they expect to deliver. The AER then scrutinises this forecast and factors into it into its final pricing decision.

If the forecast proves accurate, the cost of the network is fairly spread among consumers, and networks will make their expected revenue. If it’s wrong, networks will make less or more revenue than required.

Nobody can predict the future, so there is inherent risk in this process – in some years revenue might be higher than expected, in others, lower.

This risk is borne by gas networks themselves, who are regulated under a ‘price cap’ approach. This means that once their prices are set at the start of each five-year period by the AER, there are no adjustments to compensate for years where networks make more or less revenue than expected.

However, since at least 2011 gas networks have never experienced the downside to this risk. Incredibly, demand (and therefore revenue) has always been higher than expected.

Our report observed that gas networks have an incentive to submit demand forecasts that are below what is expected. It’s the AER’s job to correct for this under-forecasting bias, but the evidence suggests it has failed to do so.

Under-forecasting does not benefit consumers. Rather, it results in consumers paying more than necessary for access to the gas network.

Aside from under-forecasting, other drivers contributed to supernormal profits, including the fact that gas networks reduced their expenditure below the level accounted for by the AER.

In previous reports, IEEFA observed similar drivers resulting in electricity networks making significant supernormal profits. In response, the AER claimed these high profits were an expected outcome of the regulatory system. Networks can achieve higher profits by keeping their actual expenditure below the regulator-approved allowance, and in theory this should encourage productivity improvements that would lead to lower prices in subsequent regulatory periods.

However, IEEFA found no strong correlation between supernormal profits and productivity improvements among electricity networks.

For gas networks, the best available proxy for network productivity is the capital asset base (CAB) per customer, a metric of how ‘asset-intensive’ the business is. In all except two gas networks, this has increased since 2014. This indicates that gas network supernormal profits have not been accompanied by productivity improvements.

Source: AER.

Meanwhile, gas networks have experienced extraordinarily high returns on equity; well above both the AER’s allowed rate and an assumed risk-free rate. In the most extreme example, South Australia’s gas distribution network provided its shareholders with returns of 30% in a single year.

In other words, gas network shareholders, not consumers, are the beneficiaries of supernormal profits.

Consumers are paying more than necessary to access the gas network, but this is avoidable. There’s an urgent need for the AER to review its approach to assessing demand forecasts, to correct for under-forecasting biases.

Going forward, gas networks face unprecedented uncertainty. As electrification increases, the Australian Energy Market Operator forecasts that residential and commercial gas demand is likely to decline by 74% between now and 2043.

If demand for gas falls faster than the networks expect, their nine-year streak of high supernormal profits is under threat.

However, gas networks have warned of a more severe but equally likely threat – that if large numbers of consumers eventually leave the network, networks may be unable to recover the cost of their pipelines. This is called asset stranding risk.

Gas networks’ natural position is to shield themselves from this, for example by transferring it to their consumers.

This can be achieved via a strategy called accelerated depreciation – where networks ask consumers to pay higher charges now to recover the sunken cost of their pipelines more quickly.

It can also mean asking for broader changes to the form of regulation under which networks operate – for instance, moving them to a ‘revenue cap’ or hybrid approach that would see more demand risks borne by consumers, similar to electricity networks.

These are not abstract concepts. New South Wales’ Jemena gas distribution network intends to propose a change to a hybrid form of regulation, and the AER has already approved $333 million worth of accelerated depreciation charges to be passed on to Victorian gas consumers.

Our report questions the logic behind these changes. If consumers have already compensated networks up to $1.8 billion above their regulated profit allowance, there is no strong reason why they should provide even more compensation, or step in to shield networks from their stranded asset risks.

Our analysis only covered the 2014-2022 period, but the existential threat that electrification presents to gas networks has been well understood for much longer than this. We have recommended that the AER produce its own independent, robust analysis of the full extent of gas network supernormal profits, and whether these profits are reasonable.

Non-regulated businesses are expected to bear both upside and downside risks. They don’t have the luxury of reassigning them to another party (consumers) when bearing them is no longer convenient.

The ongoing extraction of high supernormal profits, combined with decisions that continue to reallocate costs and risks to consumers, highlights the urgent need for better planning around the phase-down of gas networks.

In its recent consultation on the development of an energy and electricity sector plan, the Department of Climate Change, Energy, the Environment and Water stated: “Regulatory settings will need to be considered as electrification accelerates and use of gas networks declines.”

This represents an opportunity to produce guidelines on how the AER should allocate stranded asset risks equitably between consumers and networks. It’s critical that it is developed in close collaboration with state governments – whose policy decisions have material impacts for how the transition to all-electric homes is managed.

This guidance must address the fact that under the current risk-sharing arrangement, Australians overpaid $1.8 billion to gas networks. In a future where residential gas is in decline, gas networks are now asking consumers to wear their potential losses. The failure of governments and regulators to address this issue could mean a costlier and risker transition for consumers.

Jay Gordon is energy finance analyst, Australian electricity at IEEFA – Institute for Energy Economics and Financial Analysis

State government has already ploughed more than $300 million into embattled coal generator, and has…

Less than three years after launching its home battery product, Sigenergy has dominated the Australian…

The next-generation of solar technology could be cheaper, more efficient and a step closer to…

Kaluza CEO Melissa Gander on the change in technologies, and energy thinking, that will deliver…

As Australia's biggest utility stalls on the closure of the biggest coal plant, Andrew Forrest…

Energy retailers should be required to act in their customers’ best interests, rather than forcing…

{kind=link}

{kind=link}