There is no question that major countries around the world are now struggling to manage their almost exclusive focus on promoting economic growth and jobs. Leading American economists Larry Summers and Paul Krugman have asked for much more spending on infrastructure from the U.S. Government. Many governments are relying on short sighted attempts to promote growth through monetary policies including historically low interest rates and printing money to buy bonds. This time things really are different and the prospect of low global growth for the foreseeable future is a frightening possibility. There is too much focus on short term growth and not enough cooperation on building the new growth platforms needed over the next several decades.

This may be the time to think about growth from outside the box and, in the words of one best-selling book, whatever you are thinking, do the opposite. What if the biggest new growth platforms were completely counterintuitive? President Roosevelt launched the New Deal during the Great Depression and the government invested in putting people back to work by launching, among other activities, several major infrastructure building programs (not unlike the current pleas of Summers and Krugman). There are numerous global infrastructure projects that one can imagine as new platforms for growth and jobs but none is bigger than a globally coordinated effort to de-carbonize the global energy system. The question that remains is how to make this happen?

In 2015 France will host the next major UN summit on climate change. This is probably our last chance to get a global deal on reducing carbon emissions across the world’s largest emitters. At the moment, most political leaders, including many Republicans in Congress, continue to believe that reducing carbon emissions is unaffordable during this continued period of global financial uncertainty. On the contrary, rapid de-carbonization of the global energy system is both a gigantic infrastructure challenge and the ultimate pathway to lasting economic prosperity for everyone—and it may be inevitable for a variety of compelling economic reasons.

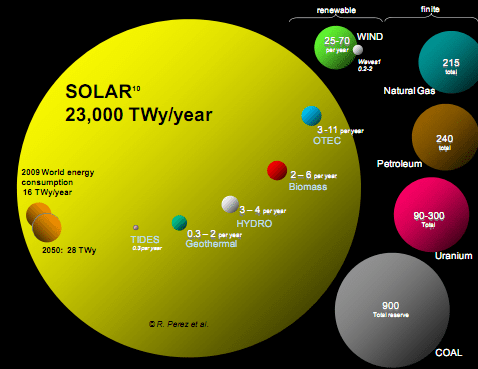

As a recent report from McKinsey on resource productivity has highlighted, future growth will require substantial increases in the efficiency with which capital, energy and resources are deployed. Many of the industrial and agricultural processes we now employ around the world are so inefficient that they will need to be completely replaced. As we scale up to a global economy that will attempt to serve the needs of more than 9 billion people in 2050, with finite resources and enormous environmental challenges, improving resource efficiency becomes the defining factor for success. The two biggest resource productivity objectives will be improving the efficiency with which water and energy resources are utilized—with staggering implications for the future supply of food, electricity and transport.

Failure in Copenhagen

The 2009 Copenhagen Climate Summit failed largely because the majority of nations participating in these UN negotiations believed, and continue to believe, that addressing climate change means deciding to be a little bit poorer in the future. Reducing carbon emissions, they fervently believed, will require lowering economic output by, among other things, increasing the cost of electricity and transport. This will create, in their view, a large negative impact on both economic growth and jobs.

There were three other issues that contributed to the failure in Copenhagen and all of them are related to the principal belief that reducing carbon emissions is too expensive. First, leading developing countries, including China and India, continue to push for a special deal that grants them less stringent carbon emissions reduction targets than what developed countries must achieve. This is based largely on the argument that, historically, their emissions were much lower than in the developed world—a fact which no longer holds true. This is the key deal breaker that keeps the US out of the Kyoto Protocol, maintains a large divide between the Americans and the Chinese, and makes getting a global deal extremely difficult.

Second, the EU, Australia, California, British Columbia and New Zealand, which all have climate change legislation in place, have a disincentive to let their carbon prices rise to levels that would drive meaningful changes in their energy systems for fear that their energy-intensive industries would leave for countries without such additional financial burdens. This is known as “leakage” and it has been used as a powerful argument to stop carbon price rules from being legislated in many countries—not the least of which in the US.

Third, there is a strong and shared belief that fossil fuels are cheap, widely produced and distributed, and in plentiful supply. With a global fossil energy infrastructure in the trillions of US dollars, and US$690 billion per year in global production and consumption subsidies, it is very hard for politicians to consider what they incorrectly believe are the higher-priced alternatives. Why promote more expensive renewable energy when coal, oil and gas are so cheap and plentiful? Even the perfectly sensible arguments advanced by Thomas Friedman in The New York Times concerning improving energy security and avoiding large cash transfers to hostile nations become non-persuasive when it comes to the primacy of fossil fuels.

Getting a deal in France in 2015 will require addressing these issues head-on as they continue to impede progress within the interim UN negotiations and in the legislative bodies of many countries and sub-national jurisdictions. What if reducing carbon emissions represented a tremendously large and economically efficient means of driving economic growth and jobs? Is it possible that, instead of thinking about a global agreement on reducing carbon emissions as an economic race to the bottom, a new global framework based on economic opportunity becomes a race to the top? Success in France depends on a new narrative where the major global powers seeking continued exponential economic growth become the driving forces for change and opportunity.

A Poor Track Record to Date

Let’s explore this counterintuitive value proposition for growth through reducing carbon emissions by reviewing where we are today in our collective attempts at responding to global climate change. We have two related international agreements on climate change with almost every country on Earth a party to one or both of them. We have been discussing climate change in UN fora for the past 25 years. We have a global carbon market that is currently trading approximately US$80 billion per year (from a high of US$150 billion) and we have more than 30 countries with carbon price laws in place. Despite what appears on its face to be a robust global climate change response, we are completely failing to make any progress.

More than 15 years ago thousands of scientists organized from around world by the Intergovernmental Panel on Climate Change (IPCC) generated several global carbon emissions scenarios which highlighted several possible future levels of greenhouse gases in the atmosphere. These scenarios reflected several variables including, for example, human population growth, demand for energy and the emergence and penetration of new energy technologies.

Here is the very disappointing, and well more than inconvenient, truth—actual carbon emissions today are tracking above the highest modelled IPCC scenario. Along with the fact that the carbon dioxide concentration in the atmosphere is now at its highest level in the last 3 million years nothing could be more confirming of a complete failure to address the staggering risks posed by a climate system completely modified by human activity.

Changing the Finance Equation

Responding to climate change is, ultimately, a global financial activation challenge. Worldwide, more than 40 times more money is invested in industrial, transport and agricultural processes and consumer goods and services that have the effect of increasing carbon emissions than on those technologies, activities, products and services that reduce carbon emissions. Although there is growing media attention on the diminishing costs of solar energy, new all-electric vehicles, and the advent of aviation biofuels, in stark contrast capital markets and major institutional investors are directing significantly more money towards increasing carbon emissions through, for example, fracking shale gas, large offshore gas processing platforms, extracting energy from tar sands, and expanding the global market for coal and coal-fired electricity.

Many recent studies point to increasing investments in the green economy but, at current levels of investment and growth, they will make little difference to our global climate change challenge. The real focus should not be limited to just promoting “green growth” but must also include a gigantic coordinated effort to reduce “black growth”. This will require large investments in the early shut down of many high carbon-emitting assets around the world. These black growth assets include, for example, a large number of coal-fired power plants—some of which are located in the US and Australia.

Meaningful investments into de-carbonizing the global energy system, on a timescale sufficient to respond to climate change and on a financial scale relevant to jump-starting significant growth, will require US$2 trillion per year immediately. This amount is twice the figure recently released by the IEA yet represents a little less than 4 percent of global GDP today—a figure roughly equivalent to the percentage of total household expenditures on all forms of insurance in OECD countries. This investment is, however, substantially more compelling than just the idea of an insurance policy against climate change. As Joseph Stiglitz has pointed out, in the current period of massive deleveraging, de-carbonization of the global energy system is a great way of restoring aggregate demand and growth.

The proposed US$2 trillion per year will need to be spread across four categories of investment that will deliver the required results over the short, medium and long term. Each category is essential but on its own insufficient to address the unprecedented structural changes required in the global energy system. For the short term results, approximately half of the annual total must be directed towards expanding low carbon energy solutions that are currently in place. This means much more investment into nuclear, solar and wind power and creating sufficient new financial incentives to substantially improve efficiency across energy production, transmission and end-use.

Roughly one eighth of the total new investment dollars will take the form of one-off payments to the equity and debt holders of high carbon emitting assets in order to secure their early closure. It may seem ridiculous to pay these big polluters but, after improving energy efficiency, this is the cheapest means of lowering carbon emissions and, in the absence of closing these assets soon, the other measures will never deliver sufficient reductions in carbon emissions. It is expected that these one-off payments would take place over 5 to 10 years. Effectively managing the timing of these investments will be critical as new capacity will need to come online fast enough to account for the loss of the high-carbon emitting assets.

To generate sufficient additional carbon emissions reductions in the medium term some of the remaining new investment dollars must be used to accelerate the development and implementation of technologies that are largely proven but not yet at full commercial scale. Despite the success of Tesla Motors and their all electric vehicles, we still have a long way to go before this technology makes a meaningful impact on growing transport sector carbon emissions. We will need to speed up both the roll-out of commercial scale electric vehicles and energy storage as well as other connected smart grid applications.

Finally, although the areas of investment outlined above take us most of the way to reducing carbon emissions on a scale and timescale meaningful to addressing climate change, we still need to get additional reductions from areas not yet proven or commercial. To use a baseball analogy, we will need to hit a few home runs with largely disruptive new technologies. These innovations are expected to be enormous and capable of launching new companies the size of Google. They include many new technologies that will have a direct impact on carbon emissions, for example, synthetic biology including artificial photosynthesis—using molecular genetics to create new microbes capable of directly producing, for example, liquid fuels. There are other technologies with indirect benefits including the revolution in quantum computing that may also prove to be fundamental to this effort.

Obstacles to US$305 Trillion

There are numerous compelling reasons why we can expect to see an enormous increase in capital investments into low-carbon energy technologies. The OECD now estimates that global GDP would need to reach US$305 trillion by 2050 in order to meet the growing economic aspirations of a human population that is expected to exceed 9 billion people. The largest component required to lift global GDP from approximately US$67 trillion today to US$305 trillion in the next 37 years is the enormous expected increase in middle class consumers—mostly in Asia. To put this into perspective, the required exponential economic growth rate between 2010 and 2050 is almost double what the global economy produced between 1970 and 2010.

Reaching US$305 trillion by 2050 is a very ambitious target and there are a few key factors and trends that makes this challenge even more daunting. First, total global debt is approaching US$250 trillion and this includes private debt (corporate debt and personal debt—including everything from student loans to home mortgages) and public debt (cities, counties, states, provinces and countries). This is equal to almost four years of global economic output at the current GDP level. Assuming we avoid widespread defaults, a significant amount of future economic growth will be required to pay down this debt.

Second, global productivity growth is declining and there is little prospect of new demographic trends or technologies that will reverse this in the near to medium term. Most of the economic growth between 1970 and 2010 was driven by technological improvements and demographic trends that led to large productivity gains. In the absence of the investments into low carbon home runs proposed above, these productivity improvements will be very hard to reproduce in the next 37 years, especially in light of the growing impacts of increased health care costs and the large numbers of people entering retirement.

Third, the largest group of people ever to enter into retirement will occur at the same time we need to see a large increase in economic growth and productivity. A large share of economic growth will need to generate sufficient financial returns to fund the retirements of this enormous group of people—even when there are large shortfalls in the funding for many public pension schemes. For example, recent studies suggest that public pension plans in the US are unfunded by as much as US$850billion.

Fourth, health care costs are soaring around the world and the treatment of growing chronic and mental disease represents the largest share of this problem. The increasing costs of treating more and more people with diabetes, for example, will have a large negative impact on future economic growth. This is despite the fact that perverse performance metrics including “GDP” will reflect the inevitable doubling of the cost of treating diabetes in the US as a positive economic result. Correcting or replacing such ridiculous performance metrics is an important part of dealing with many major challenges—including, of course, climate change.

Fifth, the IEA estimates that the required level of new investments into stationary energy systems around the world exceeds US$50 trillion by 2030. This is largely because we have not invested sufficient capital into replacing declining and inefficient power production and distribution assets nor are we currently investing at an appropriate level to meet future increases in electricity demand. This large capital requirement works both for and against the required large increases in economic growth—depending on which types of energy infrastructure investments we make.

Sixth, current global economic growth, according to the IMF, is approximately 3 percent with the US and Europe almost flat between them. Asia and a few other countries are accounting for all of the growth with little expectation that the major OECD countries will be contributing anytime soon. It is important to note that the current 3 percent also includes the “negative growth” represented by the fact that GDP counts everything—including all negative welfare activities from increased spending on chronic and mental illness, car accidents, violent crime and divorce. If we subtract the negative activities from GDP then the corrected growth figure is much less and our challenge all the larger.

Seventh, and finally, continued investment into fossil energy will never deliver the economic growth necessary to reach US$305 trillion by 2050. With demand for energy growing exponentially the total energy supply must also grow exponentially. The recently discovered deep water oil and gas reserves, the new onshore and offshore gas resources of Australia, shale gas and oil, and the prospect of new discoveries in the Arctic provide only a little help in meeting the demand-supply imbalance.

The bigger problem is these new fossil fuel discoveries require more and more capital and energy to be deployed in risk-intensive locations with potentially devastating consequences—BP and the Horizon disaster, for example. This trend leads to increased operating costs, increased fossil energy prices, lower energy return on energy invested and increased wealth transfers to OPEC producers with substantially lower extraction costs and risks. All of these factors render continued reliance on exponential fossil fuel production and consumption a major obstacle to driving the substantially higher economic returns required on the road to US$305 trillion.

A Need for Large New Growth Engines

With 37 years left to double the economic growth rate of the period 1970-2010 we have a monumental challenge that includes a range of significant obstacles—not the least of which is a constantly growing US$250 trillion debt mountain. If we re-calculate the required growth rate relative to the debt and the other challenges mentioned above, then we approach a new requirement that must triple the 1970-2010 figure. To have any hope of meeting this staggering growth rate we will need to create many new growth engines that do not exist today at any meaningful level of investment or deployment.

Launching new major growth engines means investing in every large project that has the potential to lift the efficiency with which capital, energy and resources are deployed. Nothing on this planet comes close to scale of the demand aggregation and job-creating opportunity represented by de-carbonizing the global energy system. In fact, without investing in this effort, reaching US$305 trillion by 2050 becomes impossible. Forget about focussing on climate change as the principal driving force for a low or zero carbon global energy system—this effort now becomes the only means of meeting the world’s principal preoccupation with exponential increases in economic growth and jobs.

Carbon Taxes as a Solution

The most efficient policy approach to direct substantially more capital to reducing carbon emissions is to agree on a new global framework to impose carbon taxes on approximately 75 percent of the world’s carbon emissions. The tax will drive changes in the energy system by increasing the cost of fossil resources and thereby increasing the financial attractiveness of low carbon energy technologies. Ideally, some of the tax revenue would be directed to helping low income households adapt to the changes with the majority of the funds to go directly to the companies pursuing and implementing the new technologies—which could include many of the existing global fossil fuel companies.

The level of the tax needs to be high enough to stimulate meaningful structural change in the global energy system—this suggests an initial price around US$40 per tonne of carbon dioxide emitted and slowly rising up to US$100. Prices lower than US$40 lead to nothing more than some minor and temporary changes at the margin that fail to generate any long-term reductions in carbon emissions. Governments would implement the new international agreement by legislating their own national carbon tax regulations with the tax revenue being left to be disbursed within each country. There would be no direct international wealth transfers of the tax revenues.

The remaining 25 percent of carbon emissions not covered by the tax would be available for a carbon credit system where those entities subject to the national carbon tax schemes could offset some part of their compliance obligations. This would allow forestry, REDD and the Clean Development Mechanism of the Kyoto Protocol, among others, to continue delivering low cost carbon emissions abatement. The 75 percent of emissions covered by the tax could be distributed across countries to help manage the equity challenges. The US might have, for example, 80 percent of its emissions under its national carbon tax but China could be limited to 60 percent—at least for the first ten-year commitment period.

A carbon tax is preferable to a standalone emissions trading system for at least two important reasons. First, it is easier to implement and administer and it avoids the wild carbon price fluctuations we have witnessed in the global emissions trading markets. Second, if implemented on a revenue neutral basis where taxes on investment, savings, profit and income can be reduced, a carbon tax will help drive economic growth by shifting the tax burden from activities that are beneficial to activities that reduce welfare and the efficiency with which capital, energy and resources are utilized. Once we recognize that most of fossil energy is already taxed, then a carbon tax should become much more politically acceptable and manageable.

The new narrative is very simple: if you wish to be poorer in the future then avoid putting a price on carbon emissions today and continue down the road of low economic growth and prosperity that allows capital, energy and resources to be fretted away without any regard for the economic, political, and social consequences. If you want to be richer in every sense in the future then use a robust carbon tax to immediately start the process of de-carbonizing the global energy system—reducing the risks of human-induced climate change then becomes the biggest co-benefit in history.

Michael Molitor is a Visiting Professor in the International Energy Program at the Paris School of International Affairs, SciencesPo. He was formerly the global leader of Climate Change Services at PricewaterhouseCoopers (now pwc).