Gas industry calls for solar hot water rebates to remove to try to slow down mass defections from gas networks it fears will be caused by soaring gas prices.

The Australian gas industry has renewed its attack on policies that support Australia’s solar industry – solar hot water in particular – as it fears mass defections caused by soaring gas prices.

The Energy Network Association has released a report that suggests the industry could lose one quarter of its customers as a result of soaring prices. It says 1.15 million households could drop gas and defect to solar hot water in coming years.

The Energy Network Association has released a report that suggests the industry could lose one quarter of its customers as a result of soaring prices. It says 1.15 million households could drop gas and defect to solar hot water in coming years.

As a result, it is repeating its call for federal subsidies, under the small-scale component of the renewable energy target that covers rooftop solar PV and solar hot water, in an attempt to stem the flow.

The ENA issued a media statement that claimed that non-solar hot water households would face bill increases of $50 a year if the subsidies were not removed.

The media release was given to the Murdoch press, which, of course, reported it dutifully, with the emphasis on solar subsidies. But it only takes a few minutes looking at the report itself to find out what the real issue is here.

The ENA first raised the prospect of the “death spiral” facing the gas network earlier this year in a submission to the energy white paper.

As we reported at the time, ENA warned that the cost of wholesale gas supply will likely “significantly affect” residential customers through higher retail gas prices. It warned then, as it does now, that if customers reduce gas consumption by adopting other technologies, then this could force even greater rises in gas prices because “infrastructure costs would have to be recouped over a smaller customer base.”

In effect, the gas industry is facing the same problem as the electricity industry, where rising prices are causing consumers to look at other options, forcing networks to try to recoup the cost of investment from falling volumes.

Like the electricity industry, the gas industry has built in large, static delivery costs that are being challenged by distributed generation technologies. Like electricity, around half the cost to consumers is in the form of network charges. Like electricity, the revenues that the networks are allowed to recoup from their total customer base is fixed, so if they have fewer customers, or if some customers start using less gas, then they have the right to lift fixed costs on all customers.

“There is potential for a downward demand spiral – price increases reduce demand – demand reductions give rise to an increase in regulated network tariffs – network tariff increases flow through to retail prices, with this cycle perpetuating into the future,” the latest report says.

“There is potential for a downward demand spiral – price increases reduce demand – demand reductions give rise to an increase in regulated network tariffs – network tariff increases flow through to retail prices, with this cycle perpetuating into the future,” the latest report says.

In other words, the death spiral is happening anyway, thanks to soaring gas prices. The attempt to recoup network costs as people adopt solar will result in even further bill increases.

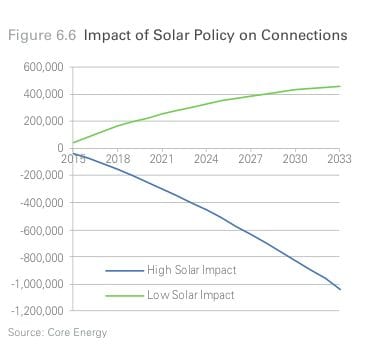

The gas industry is just trying to gain some breathing room by calling for the SRES to be abolished. It estimates that half the fall in demand could be blamed on solar subsidies, and half on soaring gas prices. This graph to he right illustrates how ending solar policies could affect demand.

The electricity industry has been using this “death spiral” argument to fight against feed in tariffs, and more recently to the federal subsidies available under the renewable energy target.

What neither industry likes to talk about is the pricing of the network – did they invest too much money in network infrastructure, and shouldn’t they take a write down on those assets, rather than just charging customers more?

The ENA release is timed as the federal government prepares to reveal its position on the renewable energy target, and try to forge agreement with the Labor Party, if not the minor parties in the Senate.

The controversial Warburton RET Review panel recommended that the small scale solar scheme be ended, or wound back quickly. The latest speculation from Canberra is that the Abbott government is inclined to keep the solar hot water incentives, but not rooftop solar PV.

The gas industry estimates there are around 4.5 million customers with gas connected and 3.4 million of these use gas for heating water. The document suggests there are 294,000 additional gas hot water units installed each year.

Solar hot water, on the other hand, totals just 865,000, with new units of around 60,000 a year.

Despite – or maybe because of – its dominant market position, the gas industry has had a history of fighting against solar hot water, raging against government regulations that require certain homes to have solar hot water. The solar hot water industry actually grew out of Western Australia, but when the gas industry signed “take it or pay” contracts with the WA state government after the initial gas boom in the 1980s, the solar hot water industry virtually collapsed.

It should be noted that the gas network industry is not exactly doing it tough at the moment. The regulated pricing means that despite falling volumes, its revenues and profits are rising. As Michael West, in Fairfax, wore recently, investors in the number one player, APA Group, have enjoyed a 19 per cent annual compound return over 14 years.

The industry has claimed, and received, a 10 per cent risk-free return from the regulator in the last regulatory period. It is so attractive that Hong Kong multinational Cheung Kong Infrastructure recently paid $3.7 billion, or an eye-popping multiple of 1.5 times regulatory asset backing, to mop up pipeline owner Envestra.

According to West, that is the sort of valuation investors that might be ascribed to an internet stock and it only points to one thing; the Hong Kong people reckon that win a handsome return from the regulator.

Hence the importance of the ENA lobbying campaign against solar, which is the biggest threat to the industry (apart, of course, to the soaring price of its fuel)

The study finds that there is potential for Network costs to increase by up to 20 per cent in real terms over the next 20 years, with the majority of this increase to occur by 2019. But it points out that price will account for half of this (as bills are increased as people drop gas).

“Assuming that Network costs remain approximately 50% of a total retail bill, there is potential for price and policy factors to give rise to a 10% real increase in retail prices, with the majority of the rise over the next five years.”

This, it says, equates to a hidden cost that would mean that gas network costs would be $50 per year more – in 2034 – than thy would if the solar subsidies were removed.

The analysis was prepared by Core Energy Group, a consultancy with predominantly gas industry clients and whose CEO, Paul Taliangis, is a former head of corporate planning at Santos, the country’s largest independent gas producer.