Kerry Schott presents well but that doesn’t make the NEG good policy

It was interesting to hear Kerry Schott’s NEG webinar presentation on Friday, not so much for what was disclosed, which in the end wasn’t that much, but more because its an opportunity to go and start thinking about what actually has happened and will happen, instead of what each of us thinks “should happen”.

As has been pointed out to me, COAG Energy Council agreement isn’t really necessary for the NEG in theory, other than politically. Anyone can request a rule change from the AEMC. Certainly the Federal Government could request such a change.

The more we think about the NEG the more problems we see.

Reliability still hasn’t been defined but what about flexibility

We still know next to nothing about the reliability guarantee. Yet it’s the signature part of the policy. The more I think about this the more bizarre it gets. So far what we know is:

“A reliability guarantee will be placed on retailers and large electricity users requiring them to hold forward contracts with or invest directly in dispatchable energy resources1 that cover a predetermined percentage of their forecast peak load.

The guarantee will be calculated based on the system wide Reliability Standard2 translated into a minimum level and type (fast or slow starting) of dispatchable capacity for each region.

If the retailer did not have sufficient dispatchable capacity available to meet the predetermined percentage of their peak load, they will face compliance action. “

Some issues we think may emerge

In this note we identify:

It’s really 3 guarantees, not 2 for each retailer.

A renewables guarantee

A fast start dispatchable guarantee. We predict that this will become the dominant part of dispatchability over time. A flexibility guarantee; i.e. the ability to quickly and cheaply ramp up and down is the quality that grids are looking for all over the world. The very fact that the ESB has called it a reliability guarantee and not a flexibility guarantee shows old fashioned thinking to us.

A slow start dispatchable guarantee (We could possibly rename this the “old coal guarantee”) although some of the gas is pretty slow starting as well.

Following on from point 1 we think that not all retailers need the same sorts or even levels of “dispatchable” power. Some retailers with peaky loads need fast start dispatchables. A small household retailer for instance has very volatile maximum demand and maximum demand is high relative to average demand. Other retailers with totally flat loads, eg a retailer with say just an aluminium smelter as a customer will have no need for fast start dispatchables at all, other than for insurance. The load is constant 24/7 365 days a year. Yet as we read whats been published to date, which admittedly is virtually nothing each retailer will need the same recipe.

Dispatchability is going to be measured relative to “forecast” maximum demand. Your analyst has the utmost suspicion of forecasts. Nearly every forecast has an agenda attached to it tending to make it biased to start with. Even leaving aside bias what period are we forecasting? The next 30 minutes, a day, a week, the next year?

Even with the dispatchability guarantee it’s still unclear how it will incentivize new investment. For what it’s worth, Kerry Schott stated that she doesn’t expect any new coal generation. But even gas generation could be a worry under the more stringent carbon regulations most everyone in the industry expects long before 2030. In our view the gas price is likely to go up before it goes down. In the past month oil has gone from US$50/b to US$60/b and the A$ has weakened. The export parity price of gas is driven primarily by the oil price. Even if wasn’t’ demand for LNG is actually increasing quite quickly. As carbon standards tighten gas generation considered in isolation will have more trouble getting under the standard.

The paradox is that right now there isn’t much profit in new dispatchables right now. Consider pumped hydro. Our estimates suggest that on a “merchant” basis it needs probably as much as $80-$90 MWh differential between the off peak and peak price, for say 4 hours every day, to justify investment. Genex won’t build Kidston as a merchant plant, and nor will Energy Australia build Cultana. It’s far too risky. They will only be built as “capacity providers”. But in our view its hard to see the need for these plants right at this instant in this market. Maybe in South Australia but not in Queensland yet. You need to assume a lot more PV and wind to be confident of a market.

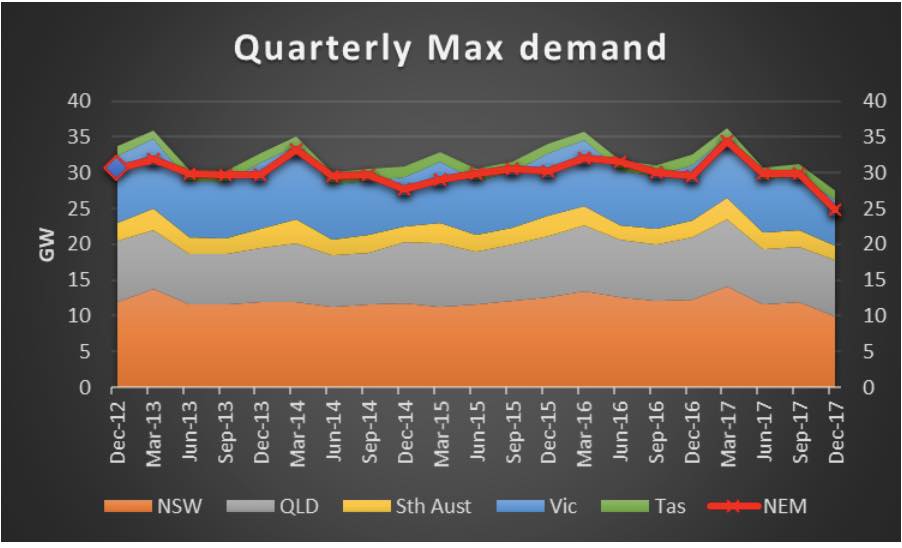

Ignoring retailers incentives to distort forecast maximum demand we think it likely that putting the guarantees on retailers is likely to result in over investment. That’s because the aggregated, forecast peak demands of all the retailers in each State is likely to be significantly higher than the forecast peak demand of the NEM. This is standard portfolio effects. Over the past five years summing the State quarterly maxium demands is about 10% higher than the NEM maximum demand. This impact will be higher for each retailer, and the more retailers there are the bigger the variation.

Figure 1 NEM max demand less than State total. Source: NEM review

The NEG is at least partly abandoning the NEM . The reliability guarantee is going to be State based. So for this purpose you can consider every retailers as having to run separate generation portfolios in each State. The renewables guarantee will accommodate State renewable targets so each retailer will have to meet those State by State. Forget the idea that you can use a windfarm in WA to make yourself feel green. You are going to need some in every State. Lets assume for a moment that Labor is returned in Qld (they are favorites with the betting agencies) and Labor in power in Victoria and South Australia. Each retailer will have to comply with the State obligations and the national obligation. This will mean that nothing will need to built in the NSW, the largest consumer of energy and power in the NEM. Yet NSW is the State where at the very least one coal power Station is going to be retired. What will replace that?

Similar to 7 what is the point of the gross pool under the NEG? Its original purpose was, as we understand it, twofold. Firstly to determine which generators were dispatched and secondly the pool price would act as a forward investment signal. However the dispatch function is increasingly being distorted by wind & PV which are essentially dispatched whenever they can run because of their close to zero marginal cost, and the new investment signal is fairly meaningless as that is now going to be driven by the various guarantees

Poor Process – where is the background paper?

Whether we contrast the NEG with development of the carbon price in Australia, or the Finkel report, it’s crystal clear its an idea produced in a hurry with little or no consultation with many of the stakeholders. A completely unnecessary hurry. Australia’s wind & PV penetration remains quite low.

We have years to get this right. In our view haste and secrecy are a poor way to develop a policy and risks a lack of buyin from stakeholders. In particular it’s a shame the electricity industry wasn’t consulted or a process similar to the Finkel Report couldn’t have been adopted. After all this a relatively big change sprung upon Australia with a “like it or lump it attitude”.

Because it’s in such a nascent state it’s difficult to be too specific in the comments. That is a bad thing. We are being asked to buy a concept rather than a fully developed plan and then live with the consequences.

Nor is this a policy likely to substantially change electricity prices, particularly in the near term. If anything its likely to result in a delay in new investment while the details are sorted.

In the corporate world it would be normal to have a Plan A, a Plan B and a Plan C.

The merits and demerits of each would be examined by a careful study, there would be lots of consultation on the plusses and minuses of each policy and then a considered choice would be made. By contrast ,this policy development process stinks.

It’s natural to think that rushed through policies developed in secret are anti democratic and normally served the vested interests of the people proposing the policy.

Your author has been watching “Borgen” where exactly these points were made. So in our view the policy is handicapped from the start, but lets put that to one side.

Why reinvent the wheel? No one else does it this way

Somewhat contrary to Ms Schott’s webinar comment, we don’t believe there is anything like the NEG in the ERCOT [Texas] market. ERCOT does have a gross pool, like the NEM, but that’s as far as it goes. It manages its reliability issues via emergency response capacity auctions.

You don’t have to look far to see how it is done in other jurisdictions. AEMO’s advice to the Federal Govt as recent as September 26 contained a report by the Brattle Group entitled:

This covered, Texas, Belgium, Alberta, Ireland, New York and one or two other regions.

Every electricity grid in the world is dealing with higher renewable penetration. As we keep saying Australia is lagging, not leading, and there is much that could have been learned from overseas markets.

To us it seems fairly disrespectful of the ESB, or maybe arrogant, that it can be so confident that an overnight thought bubble is going to be superior to carefully developed process in overseas markets developed after considerable thought. Its typical of recent policy development in Australia that all the Finkel work is done and then its just tossed out.

Meanwhile, where is the 2017 NTNDP?

Developing better transmission is an obvious way to improve reliability. Too bloody obvious apparently. Doing a better job on transmission planning was a Finkel recommendation. What’s happened?

A consultation period for the 2017 plan started in January, submissions were held by March and …. actually nothing else has surfaced.

So this is the real work, that’s been delayed by all this NEG reinventing of the wheel. Last year’s useless plan was produced in October 2016. Everyone recognizes that a more progressive plan is needed. Transmission takes longer to build than new renewables. Much longer.

Forecasts, incentives and generation contracts

The requirement is relative to “forecast peak” load. However, actual loads can differ significantly from forecasts. Who does the forecasting?

Every retailer immediately has an incentive to underestimate their “foreast peak load”. We have already seen from the network businesses that gaming of forecast demand is an absolute fact of life.

Secondly, retailers can gain or lose load during an accounting period. Industrial loads in the TWh level can move around quite quickly depending on management strategy and market conditions how will the “compliance police” think about this.

Thirdly, it seems as if every retailer is going to have to have a level of both “fast” and “slow” start dispatchable capacity. Even leaving aside the definition questions it seems extraordinary that this should be a requirement on every retailer.

In fact it goes further than the retailer. If you are an independent customer operating in the NEM, say an Adelaide Brighton Cement or similar, you will also have to comply.

So poor old Adelaide Brighton will have to buy some fast start dispatchables, some renewables and some slow start dispatchables according to some formula dreamed up by the AEMO and measured and enforced by the AER according to rules drawn up by the AEMC with the whole thing overseen by the ESB.

Yes, this is Australia …. the land of opportunity and innovation. .

In the end, reliability and dispatchability are not retailer level issues, they are system level issues, more properly managed by the AEMO.

Emissions intensive export oriented industries may be excepted from the emissions guarantee but not the reliability guarantee. This seems just plain weird, and of course puts even more load on other sectors of the economy to do emissions reduction.

We think that a focus on reliability is arguably at odds with the direction of today’s generation market and although it seems subtle the industry is trying to move in the direction of flexibility.

We already know that demand in the NEM is quite volatile. Over the last five years the daily average difference between maximum and minimum demand is about 8 GW or about 37% of daily average demand over the same time period and our present system copes with that reasonably adequately.

All that said ramping requirements from renewables are still less than traditional daily demand driven ramping

Lots of talk about intermittency and duck curves tends to ignore the fact that demand in Australia has always been peak and on average across the NEM the difference between minmum daily demand and maximum daily demand is about 37% of the average daily demand.

That number has not changed in the past five years despite rooftop PV. A few charts can easily illustrate this.

Coal generation on average isn’t ramping anymore than it used to

The following two figures compare for NSW the average daily demand of dispatchable (coal + gas + hydro) in 2013 and 2017 and then coal alone.

What the figures show is that coal demand has always had to ramp up and down in NSW, and so far if anything, less ramping is required due to the unshown average impact of PV and wind. Of course the averages can hide extreme cases.

The figures do show a duck curve, but so far its much smaller than the ramp that has always been there and that the system copes with quite easily. In 2013 the average morning trough to peak was about 400 MW more than in 2017.

Figure 2: NSW coal & other dispatchables by time of day. Source: NEM Review

Let’s look at QLD: Next we see (i) an increase in the average level of coal generation and (ii) a flatter overall profile but no real evidence yet of the middle of the day duck curve being as important as the “normal” daily morning increase in demand.

The increase in average levels of coal generation is equally due to a reduction in gas generation and an increase in demand due to the CSG wells and compressors all being electrically powered.

In QLD, as in NSW, in short, so far the impact of renewables on dispatchability requirements still seems small relative to the historic requirement to ramp up and down. Indeed, if anything – and as in NSW – the total trough to peak morning ramp in percentage terms has declined.

Figure 3 QLD coal average coal generation by time of day. Source: NEM review

But what about South Australia…

As we’ve explained many times we think South Australia is a poor grid to do high wind & PV market share in. The reason is the only dispatchable generation sources are some mostly fairly old, and old thinking, gas generators, and the limited interstate transmission link.

If South Australia had more transmission, its rich, renewable resources could be far better integrated into the NEM. Be that is it may, the data shows…..

Figure 4 South Australia, coal & gas average generation by time of day. Source: NEM Review

Figure 4 South Australia, coal & gas average generation by time of day. Source: NEM Review

On average less coal and gas are being used today in South Australia than before (partly replaced by renewables and partly by extra imports) and

More ramping is required in South Australia, but, in our view, considering that renewables are now up to about half the market, not on average, as ramp heavy as you might have thought. Averages can conceal extreme problems but this review is already over long. For one final chart we compare the 2017 dispatchable generation in NSW with that in South Australia, with both expressed as an index.

Figure 5 Sth Australia dispatch generation compared to NSW as index 2017. Source: NEM ReviewFigure 5 Sth Australia dispatch generation compared to NSW as index 2017. Source: NEM Review

Despite the way higher renewable penetration in South Australia the dsispatchable generation profiles in the morning a very similar (we do ignore imports but NSW has those as well). South Australia does have a bigger evening ramp compared to NSW, but it’s no bigger than the morning ramp. This might lead you to think that NSW could easily cope with more renewables without seeing ramping requirements of its dispatchable generation any different to what already happens.

8 responses to “National Energy Guarantee’s bizarre approach to reliability”

trackdaze

Demand management for the coalition has so far been to chase vehicle manufacturing out of the country.

Rod

Yes, looking at the minimum thermal generation difference for SA makes me think it is a loss of demand. Maybe partly due to Holden dropping from 3 shifts to 2.

bruce mountain

Thanks David for putting the time into this. As you say, not just an empty cupboard but

a rather large can of worms. The NEG was an embarrassment from the outset, and is a real setback from the reputation of our institutions, at least some of whom deserve respect. While various hanger-oners can be expected to have been slow on the uptake, that it has taken others so long to figure it out is something they should have to account for.

MrMauricio

Fantastic analysis David-thank you!!!

howardpatr

Schott is probably being run over by the fossil fuel incumbents man, John Pierce.

As Abbott would say, give me a lawyer before a scientist, like Finkel, to advise on anthropogenic climate change and the renewable energy future.

Andy Saunders

“In the end, reliability and dispatchability are … system level issues”

That’s the most important sentence in the whole article, and one which has very important ramifications, if you think it through.

solarguy

An interesting article David, thank you. I all seems very complicated though, but could you tell us, if you had a hand in transforming the grid to 100% RE, what would you recommend needs to be done to set it up going forward.

Les Johnston

A good article which highlights the vagueness and weakness in three word slogans. Complexity must be an integral part of reforming the market not simplistic vague utterances.