Spark Infrastructure half year results:

Spark Infrastructure (SKI) is by far the most pure play electricity infrastructure listed investment in Australia, and has a market capitalization of $4.3 billion. It has achieved this despite not having majority ownership or control of any its assets (structurally subordinated).

Because it operates in South Australia it has first hand experience of the impact that renewables have on the wires and poles business and the opportunities and challenges that presents. For the most part we would argue that rooftop PV in South Australia has had only a minor impact on SAPN returns. Those returns are driven more by regulatory decisions. That’s because returns in regulated utilities are not impacted by volumes.

In fact both the South Australian and Victorian business of SKI now have “revenue caps” as opposed to “price caps”. This means that if the regulated revenue in a given year earned by the business is above or below what the regulator allowed, then prices are adjusted the following year to give back or recover the difference.

For investors this is extra security and a lower cost of capital and for PV users this means that the regulated business no longer has a volume incentive to make PV connections difficult.

Win win.

The downside is that management no longer feel they need to disclose volume information. This is disappointing as networks are historically the best source of volume information providing a split between, large, commercial and mass market consumption unavailable elsewhere. Here’s hoping they correct this oversight going forward.

Another issue is that volume based pricing is in theory not cost reflective pricing. We will leave that discussion to another time.

Summary of underlying maintainable results for six months

SKI reports underlying look through ebitda of the assets on two bases. One includes customer contributions, revenue cap overs and unders and is essentially an accounting view. The other is an adjusted view which removes mostly “one off” items. We have used those numbers.

Secondly we have including in our view of “free cash flow” 35% of the growth capex for the half. We also assume the VPN tax expense will show up in cash tax paid. On that basis our presentation of the free cash flows and comparison to dividends is:

3 years, DPS CAGR 5%, EV:RAB around 1.5X

Management provide the following distribution guidance:

SKI’s credit ratings are A- for VPN and SAPN. That provides confidence.

The confidence is reflected in the asset valuation, where SKI is basically valued at around 1.5X its share of asset RAB. In our experience this is at the upper end of where regulatory assets have been able to trade both in Australia and in Europe.

Much of the interest in SKI is in transgrid new transmission

When a consortium bought 100% of Transgrid from the NSW Govt. in 2015 the ebitda multiple was about 16X which was regarded as very high relative to the trading multiples of SKI, AST and DUE or even APA. However when analysing this at the time it did seem as if the major upside was in the new transmission that will be required to support increased renewable penetration.

Unless storage is a big part of the system, moving to to high levels of renewables generally means that higher levels of capacity relative to demand and a greater level of redundancy are required. And the way to utilize the extra capacity is to connect it up with more transmission.

One good example of this is in Texas where around US$7 bn has been spent by ERCOT to reinforce transmission there as the wind penetration has increased.

However getting new transmission built in Australia is presently difficult, particularly if its to be “regulated transmission”.

Sounds familiar, this was 2005?

“In the end it was the latter situation which prevailed, but we have been left with a lack of interconnection capacity into critical areas — like South Australia — and with expensive and sub-optimal transmission links. I noted, Chairman, that in the middle of the blackout in South Australia last Monday, when half of SA was without power and support was desperately needed, Murraylink contributed just 50MW — less than 25% of its rating. It was pretty useless.

A strong essentially free-flowing transmission system, regulated efficiently, delivering bulk power when it is needed, and facilitating competition between generators, is what we need. “

Source:Dr Robert Booth testimony to ACCC, March 18 2005

Regulatory test for transmission [RIT-T]

“Under the RIT-T, TNSPs are required to assess the efficiency of proposed investment options by estimating the benefits that would result for market participants and consumers, and comparing these to the associated costs. If a proposed investment passes the criteria governing the RIT-T, the TNSP will proceed with the investment, and this will be funded by market customers through Transmission Use of System (TUOS) charges…….

In addition, few investments in interconnectors between regions have occurred, largely due to the relatively small differences in fuel costs between the regions.” : AEMC review 2013

The AEMC noted that under the curenet system generators can be constrained off. Generators have little incentive to fund new transmission because other generators can act as “free riders” and take advantage of new transmission. The AEMC noted this was an unusual model by global standards and a better model might be to allow for generators to bid for a guaranteed share of transmission (as ocurrs in gas pipes). However this model in gas has its own problems. In any event its slow and hard to justify new regulated transmission particularly interstate links.

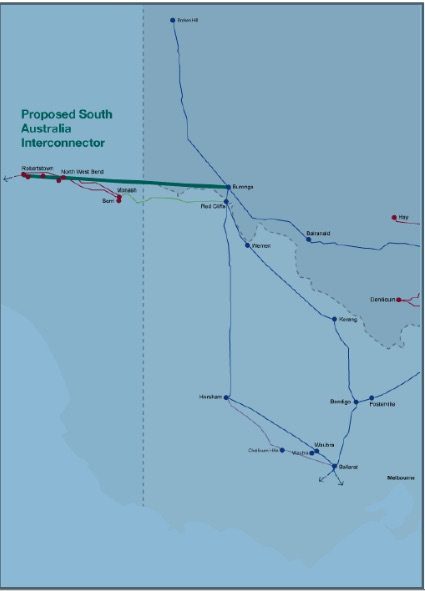

New NSW – South Australian interconnector 650 MW $500m

The SKI results outlined the benefits of a proposed new interconnector, particularly reducing pool prices in both South Australia and NSW and Victoria but increasing transmission costs by about $70-$80m per year [ITK estimate].

The new transmission would allow more renewable energy to be built and connected in both South West NSW and in South Australia.

The project is expected to cost around $500m with 650MW of capacity on a 275kV transmission line and could be built in 18 months from final investment decision [FID].

So in our view this project could and probably will be up and running early in calendar 2019. The steps are:

SCER/AEMC review regulatory test methodology by, say, Xmas 2016. Apply the regulatory test to the proposed link by June 2017. Build transmission link by Xmas 2018. Operate in 2019.

There will be more to be said about this, but in our view despite the fact that above ground transmission has about the same level of beauty as a wind farm it’s great that we are getting on with it.

David Leitch is principal of ITK. He was formerly a Utility Analyst for leading investment banks over the past 30 years. The views expressed are his own. Please note our new section, Energy Markets, which will include analysis from Leitch on the energy markets and broader energy issues. And also note our live generation widget, and the APVI solar contribution.